Co-authored by Allan Mortel and Howard Badger, Partners at Pitcher Partners Sydney.

A Firstlinks reader, Robert Baker, asked the following question:

"For an increasing number of LICs, post-tax NTA is now larger than pre-tax NTA, a reversal of what many investors experience as the norm. However, chatting to other LIC holders, the potential financial implications of this shift is not understood. For example, what are the franking credit implications of having a high post than pre tax NTA?"

A listed investment company’s (LIC) net tangible asset (NTA) is an important measure of its worth or financial position at a point in time. In theory, the calculation of NTA is simple, but the reality is that there is a great disparity in the way LICs calculate and report their NTAs.

[For more on LIC performance, see Chris Cuffe’s article, published in this publication on 14 December 2017.]

Generally, a profit generated usually results in the recognition of an income tax liability. An investor in a LIC can expect the post-tax NTA to be lower than a pre-tax NTA. However, this is not always the reality as some LICs are reporting post-tax NTAs higher that the pre-tax NTAs.

What is happening with these NTAs?

In our current climate of share market volatility and the many unknowns surrounding the impact of Covid-19, some LICs may experience significant realised and unrealised losses resulting in large tax benefits being recognised. Ultimately, directors and auditors will need to scrutinise the recoverability of these losses under the accounting standards as to whether they are recognised as assets, written down or written off completely. However, this generally will not take place until the year end (or half year end) reporting cycle.

Monthly NTA announcements by LICs during this crisis may not have the same level of rigour applied to the assessment of tax benefits as during annual and half year reporting.

Investors need to know what to look for to better understand a LICs published NTA. Briefly, for a LIC to report a higher post-tax NTA than its pre-tax NTA, it must have a tax benefit that exceeds its tax liabilities (if any) and include that tax benefit as an asset. Prima facie this would indicate the LIC has experienced losses.

What is a tax benefit?

A tax benefit is also known as a deferred tax asset (DTA) or in the old terminology, future income tax benefit (FITB). Simply stated, it’s the amount on which a company can pay less income tax in the future.

A tax benefit may include one or a mix of the following:

|

|

Type of tax benefit

|

What’s the implication?

|

|

1.

|

Tax losses—including carried forward tax losses and current period tax loss either arising from trading losses or expenses exceeding income.

The nature of a tax loss (revenue or capital) for a LIC on capital account for tax purposes may limit their utilisation.

|

LIC will not need to pay tax to the extent of tax losses available. Not able to be converted to cash.

Investors need to be aware that this asset would not convert to a refund or cash on wind-up or transfer to a Trust in the event of a scheme to convert from a LIC to a managed investment scheme / trust or Listed Investment Trust (LIT). It would instead be written off the balance sheet and expensed.

Further, a company can lose tax losses, but that’s too technical to go into in this article.

|

|

2.

|

Net unrealised losses on investments

|

A temporary tax provision, which until the investments are sold, may change in amount or become a liability (i.e. in the event the value of the investments increases above their cost base).

|

|

3.

|

Excess franking credits contribute to carry forward tax losses, which can be recognised as a tax benefit.

|

As for 1 above.

|

|

4.

|

Capitalised offer costs—a tax deduction deferred (claimed) over 5 years from being incurred. Being the capitalised cost at the relevant company tax rate.

|

A temporary difference between the accounting and tax treatment. The LIC will benefit from the tax deduction (pay less tax) over a 5-year period.

|

|

5.

|

To the extent a trading stock election is made in respect of investments held as trading stock, a deduction may be available to generate tax losses in the relevant income tax year.

|

As for 1 and 2 above.

|

|

6.

|

A tax refund due from the ATO (this should be recognised as a current tax asset but may be grouped for NTA purposes together with other tax benefits).

|

Will be converted to cash.

|

What are the implications of tax benefits on franking credits?

The recognition and value of tax benefits recorded in a LIC’s balance sheet is subject to satisfying the relevant criteria stipulated in the accounting standards. The tax benefit recorded in a LIC’s accounts and used in NTA calculations should be that amount the directors reasonably expect to be utilised by the company within a reasonable period. That is, there must be an expectation that the company will derive income or gain in the future that will be taxable and the tax benefits will reduce the amount to be paid to the ATO. Sounds good, but is it that straightforward? Consider:

- For many investors, a LIC’s ability to pay franked dividends is attractive. A LIC either receives franking credits with franked dividend income earned on stocks within the portfolio or generates them by making tax payments to the ATO. Where a LIC does not need to pay tax to the extent that tax losses are available, it will not generate further franking credits.

- If the LIC’s income predominately consists of franked income, it won’t need to pay as much (if any) additional income tax, keeping cash in the company and still having franking credits available to distribute to shareholders. However, unfranked income is required to utilise the tax benefit.

- If the LIC does not receive sufficient franked income to frank a dividend, it could elect to carry forward (some or all of its) income tax losses and elect instead to pay tax which would generate franking credits to enable it to pay franked dividends to shareholders. This would entail the company utilising its cash instead of its tax benefit.

- Carried forward tax losses will only have real value where there is unfranked income to absorb that loss. This arises due to the extent in which any profits in the LIC are taxed, they can be distributed to the shareholders with the accompanying franking credit. Conversely, profits that are distributed without corresponding franking credits will have less value to most shareholders.

What should investors look for?

Here are four points for LIC investors to check:

1. Understand the LIC’s predominant investment style

Whilst some LICs may have a mix of long-term investing portfolios and more actively traded portfolios, there will be a more dominant style. The ASX Listing rule option to either disclose NTA before or after provisions for estimated tax on unrealised income and gains (deferred tax) can be confusing to investors.

For example, for a LIC that:

A. Rarely realises an investment and therefore rarely pays the deferred tax liability provided in its accounts, the NTA backing before the estimated tax on unrealised income and gains is a meaningful proxy for the net assets at work for shareholders. This LIC might be described as having a long-term, or passive investment style, or investing for income growth. OR

B. Actively realises its investments, the estimated tax liability provided in its accounts will quickly become payable and therefore, NTA backing after all tax provisions may be a more meaningful proxy for the net assets at work for shareholders.

Ideally, each LIC would report both NTA backing before and after provisions for estimated tax on unrealised income and gains (or net losses) and explain which they consider more meaningful.

2. Understand the nature of tax balances

A tax benefit that relates to net unrealised losses may be less of a concern than one that relates to growing tax losses. A LIC may have both tax assets and tax liabilities at a point in time. They may not have been netted off due to the differing nature of the tax item (e.g. capital losses cannot be used to offset income gains for some companies) or perhaps they were disclosed separately because the portfolio swings from unrealised losses to unrealised gains with regularity.

3. Look at trends in tax balances

Some LICs continue to pay tax and frank dividends to shareholders, yet tax losses remain on the balance sheet or continue to grow over time. What sort of performance would see the tax losses utilised without impacting franking credits available for distribution? Or will future dividends need to be franked at a reduced rate? Are there calls to wind up the LIC, convert to a trust or return capital to shareholders? If so, will the tax assets be written down or off rather than benefit the company and its shareholders?

4. Look for disclosures of the LIC’s franking balance

Franking credits that a LIC has available to distribute to shareholders are not recorded on the balance sheet nor in any NTA calculation and are of no value to shareholders until they are distributed (and to varying degrees of value depending on the shareholder’s circumstances). Further, a company can only distribute franking credits to the extent that the company has profits available.

A dividend cannot be franked beyond 100%. Accordingly, a LIC with franking credits greater than accounting profits may have franking credits unavailable for distribution.

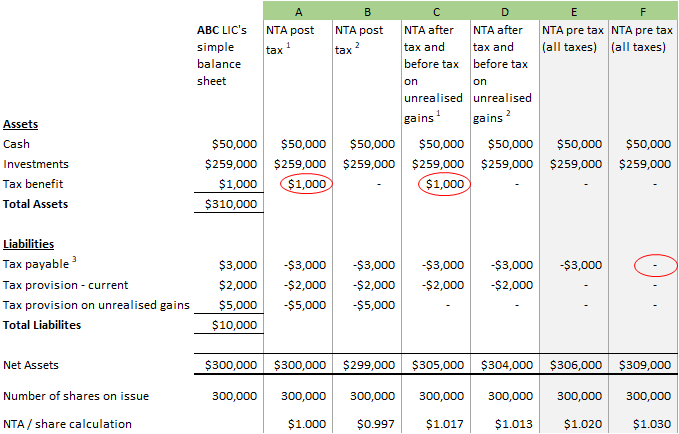

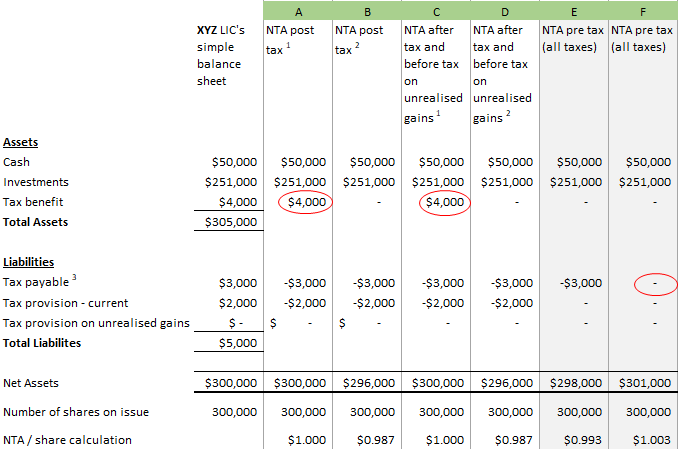

Footnote: the variation in NTA calculations

Bearing in mind all of these factors, a LIC can publish various calculations of its monthly NTA by altering assumptions on the tax benefit and tax provision on unrealised investments. For completeness, we have included some examples to show how the NTA can vary. The calculations in each column A to F are explained briefly as follows:

- In practice, some LICs include tax benefits as an asset. In the second example, this results in post-tax NTA being higher than the pre-tax NTA.

- The tax benefit is excluded from the calculation on the basis the tax benefit is intangible.

- Any provision for tax on unrealised gains is excluded, but tax benefit is included.

- Any provision for tax on unrealised gains is excluded and the tax benefit is excluded as intangible.

- All tax balances are excluded, except tax payable arising from an assessed liability to ATO.

- As for E above, except tax payable has been excluded (in error).

In the first example, Company ABC has a significant provision for tax on unrealised gains suggesting that the portfolio has recorded gains. In this case, the post-tax NTA is lower than the pre-tax NTA.

In the second example, Company XYZ has a significant tax benefit, suggesting the portfolio has suffered a loss or the LIC has had prior period losses. Note that in some calculations the post-tax NTA is higher than the pre-tax NTA.

1 Tax benefit included as an asset (in practice some LICs include tax benefits as an asset. See footnote 2 below)

2 Tax benefit excluded as an asset (we consider a tax benefit to be an intangible and should be excluded)

3 Tax payable arising from lodgement of a tax return converts from a tax provision to a creditor and does not get excluded as other tax provisions are from the pre-tax NTA calculations

Scott Whiddett, Allan Mortel and Howard Badger are Partners at Pitcher Partner Sydney, advisers to fund managers, investment entities and investors. The material contained in this publication has been made available for informational and discussion purposes only, it is not professional advice. Neither Pitcher Partners nor its affiliated entities, nor any of our employees will be liable for any loss, damage, liability or claim whatsoever suffered or incurred arising directly or indirectly out of the use or reliance on the material contained in this publication.