Underpinning the current wave of consolidation amongst Australian superannuation funds is the belief that it helps to be big. Is this really the case? Is there any advantage in being a member of a large super fund?

We address the question of whether large size benefits members in a recent paper found here. Our answer is a ‘definite maybe’. We don’t think size matters as much as how it is used. If a large fund can leverage the advantages and limit the disadvantages of size, then members can be better off. However, operating effectively at scale faces many challenges. In the end, what matters is how well management executes, whatever the fund size.

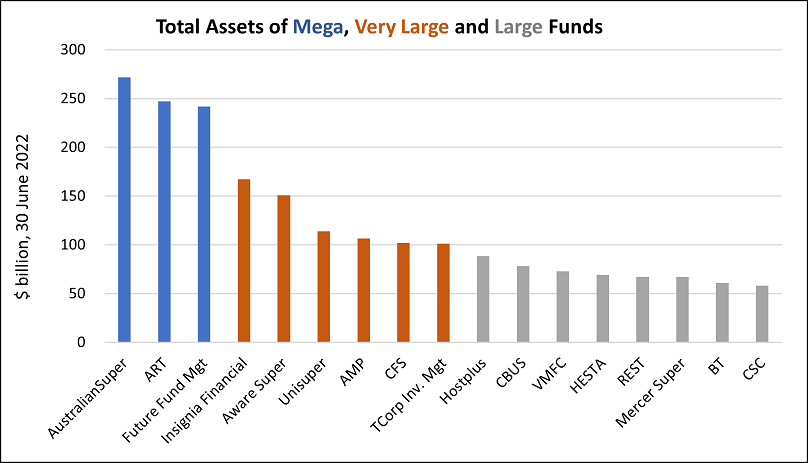

Australia now has mega-funds

Consolidation combined with member contributions and switching has created some large superannuation funds. Australia sported 17 funds with assets under management (AUM) exceeding $50 billion at June 2022 (see chart). Of these, 14 are superannuation funds. The biggest is AustralianSuper at $272 billion, with Australian Retirement Trust (ART) not far behind at $247 billion. The Australian superannuation industry has not only become systemically important – at $3.3 trillion at June 2022 it stands at around 1.4-times both GDP and the ASX market cap – but now contains some seriously large financial organisations.

Advantages of large size

Size brings two types of advantage. First is that it can be used to lower costs per member, i.e. economies of scale. Second, large funds can do some things that smaller funds and private investors cannot, i.e. economies of scope.

Large fund size can lower unit costs in three ways.

First is by managing assets in-house. The cost of running an internal team is fixed to some extent, meaning that the cost of managing a particular asset mix declines as AUM increases relative to paying a basis point fee to external investment managers. AustralianSuper now manages 53% of their assets internally while Unisuper is at 70%. The percentage managed internally is rising at most larger superannuation funds in part with the intent of limiting fees which come under regulatory and public scrutiny.

Second, lower fees may be negotiated with external investment managers for larger mandates.

Third, some elements of administration costs are fixed and can be spread over a larger member base. Research confirms that size does indeed reduce per-unit costs in administration.

While lower investment expenses combined with administration efficiencies hold out the potential for lower fees for fund members, it may not work out this way. Large funds might instead use their size to do things that might benefit members in other ways.

On the investment side, large size facilitates investing directly in ‘big ticket’ unlisted assets such as infrastructure or commercial properties. This can help with diversification and may provide access to unique opportunities. However, investing in unlisted assets is costly, which limits potential for fee reductions. The key benefit is in finding additional return sources in private markets that are not available to smaller funds (or private individuals).

Large size might also support more and better customised member services where significant resources need to be committed. Ability to customise may be particularly important in offering retirement income strategies going forward, noting that retirees have widely differing needs. While tailoring to these differing needs might be more effectively done under financial advice, there are many retirees who may not take advice and will look to their superannuation fund to assist them. A larger fund should be better able to cater for such members where doing so effectively relies on high levels of functionality through expensive systems and staff.

Disadvantages and challenges

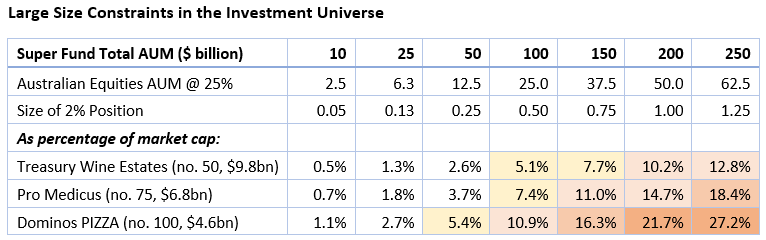

There are also downsides from being large. A key one is that the fund becomes constrained in taking investments that cannot absorb the larger licks of AUM required to make it worthwhile. This is the case in certain segments of the equity market, such as small-caps and even mid-caps. As a fund grows in size, it becomes harder to move an equity portfolio without incurring costs through ‘price impact’. The investible universe also narrows simply because there are limits to how much can be reasonably held of particular stocks.

To explain, the table below shows the percentage that needs to be held of the three ASX stocks ranked 50, 75 and 100 by market cap at time of writing, assuming that the fund targets a 25% weight in Australian equities and a minimum holding equal to 2% of the equities portfolio. For example, to hold a 2% position in Pro Medicus, a $100 billion fund needs to take 7.4% of the company, while a $250 billion fund needs to take 18.4%. Once a fund gets to ‘mega-fund’ status, it is doubtful they could prudently invest in Australian mid-caps in sufficient volume to make a meaningful difference, let alone invest in small-caps.

Such investment constraints matter if these smaller areas offer the best opportunities. This can be often the case as they may be under-researched or offer illiquidity premiums. Smaller funds and private individuals face no such size constraints. Instead, their challenge is having the capacity to identify and access good opportunities. While this might be done through investment managers, there are fees, and talented managers need to be identified.

In addition, large organisations are more complex, less flexible, more bureaucratic, and can find it difficult to coordinate staff to work towards a common purpose. These elements may easily create dysfunction that can work to the detriment of performance. Also, surveys suggest that large funds are poorer at delivering a positive personal experience to those members who engage.

Large funds can be challenged to find sufficient attractive assets to fill a big portfolio. AustralianSuper, for instance, received inflows averaging about $500 million per week during 2021-22. If there are insufficient attractive assets available, performance will be diluted. Whether this is the case depends on the pricing of large ticket assets, which in turn may vary with competition for those assets and market cycles.

Large funds need to construct operating structures to succeed at scale. This likely entails building an internal team with capabilities to invest in unlisted assets, noting that this area is somewhat specialised. Members will only benefit if the internal team performs, so that any cost savings are not wiped out by lower returns. Eventually there may be a need for overseas offices – AustralianSuper and Aware Super are taking this step. This only increases the degree of difficulty. Attracting and retaining skilled staff is particularly important, but tricky. Strong governance and a positive culture also matter.

Delivering enhanced member services can be challenging. It usually requires building systems, where projects tend to run over-time and over-budget and sometimes fail. No easy wins there.

In short, large size offers a mix of advantages and disadvantages along with many challenges. None of the benefits are guaranteed. Management has to execute well.

Potential systemic impacts

It is also worth noting that growth and consolidation in superannuation could have some systemic impacts. These are more likely to detrimental, although unlikely to be major. Our concerns fall into two groups.

First, the financial system would be stronger and more vibrant if populated by superannuation funds of various sizes. Concentrating assets in a handful of large funds could dent market resilience and competition, both of which are enhanced by diversity of participants. Institutional presence could be hollowed out in markets that large funds tend to pass over, such as those providing capital to smaller companies. This matters as institutions help enrich the market environment through research, price discipline, monitoring and liquidity.

Second is what happens if a large fund gets into trouble. Large funds have more members and a bigger footprint. Any ructions might cause damage on a broad front. While a run on a fund seems unlikely, it is not impossible given that member choice allows members to switch at call. The Your-Future-Your-Super test only raises the risks on this front. The losers would likely be members within the fund, as it scrambles to unwind it positions.

Capability matters more than size

Something of a ‘size is good’ mantra has been going around parts of the superannuation industry. However, size is not an automatic win. One consideration for members is whether a superannuation fund offers capabilities or services of value to them, ideally at a competitive fee.

Large funds have the potential to deliver aspects such as lower fees, enhanced exposure to unlisted assets and a richer set of services such as retirement strategies. But an even more important consideration is whether the fund will deliver. In the end, the capability of its management probably matters most of all.

Geoff Warren is an Associate Professor at the Australian National University and a Research Director at the Conexus Institute. This research is conducted with Scott Lawrence of Lawrence Investment Consulting. This article is general information not personal financial advice.