It's a worry when a simple survey of financial literacy shows half of men and nearly two-thirds of women cannot answer correctly five simple questions. It's even worse when 13.4% are wrong on the majority of the questions, especially when we expect people to understand credit cards, buying a house and even the most complicated financial subject of all, superannuation.

Surely, Cuffelinks readers will nail these questions. The survey below will take only a minute or so to complete.

The Household, Income and Labour Dynamics in Australia (HILDA) Survey is a nationally representative longitudinal study of Australian households. Now in its 13th year, it collects information annually, from the same pool of people, on a wide range of aspects of life in Australia, including household and family relationships, child care, employment, education, income, expenditure, health and wellbeing, attitudes and values on a variety of subjects, and various life events and experiences.

Of particular interest to us here at Cuffelinks were the findings on financial literacy.

In his opening remarks for the section on Financial literacy and attitudes to finances, Roger Wilkins, Deputy Director (Research) of the HILDA Survey, says:

"Despite rising levels of income and wealth in the Australian community, the issue of financial literacy remains highly relevant, with many policy-makers in the wake of the 2008 Global Financial Crisis bemoaning the widespread lack of financial knowledge."

And:

"Financial literacy is defined by the OECD International Network on Financial Education (2011) as: 'A combination of awareness, knowledge, skill, attitude and behaviour necessary to make sound financial decisions and ultimately achieve financial wellbeing.'

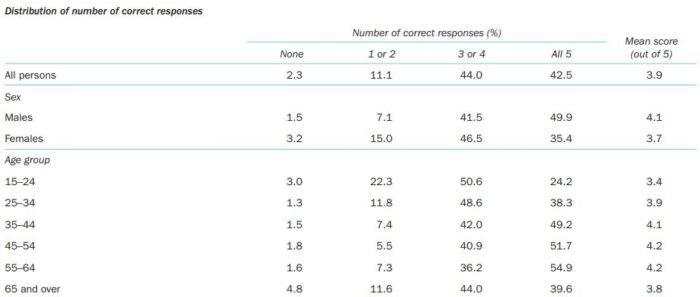

"In Wave 16, the HILDA Survey included measures of basic financial literacy using an approach pioneered by Lusardi and Mitchell (2014). Five questions, respectively covering numeracy, inflation, portfolio diversification, risk versus return, and money illusion, were administered in the interview component."

Respondents were classified into three levels of financial literacy: low (two or fewer correct answers); medium (three or four correct answers); and high (all five questions answered correctly). As the table shows, 13.4% of people are in the bottom category, 44% are in the middle category and 42.5% are in the top category. There was also a significant gender divide, with men collectively scoring 4.1 out of 5 and women scoring 3.7.

We are interested in how Cuffelinks readers compare with this survey, so we have replicated the five questions in a quick quiz, linked below. We'll come back with the results next week.

Create your own user feedback survey