“People of the same trade seldom meet together, even for merriment and diversion, but that the conversation ends in a conspiracy against the public or in some contrivance to raise prices.”

Adam Smith, The Wealth of Nations, 1776

Every day in recent weeks, we read about bank culture in the media. It seems everybody from the Prime Minister down is talking about it. It will now be an election issue with Labor promising a Royal Commission if elected. At the recent sold-out ASIC Annual Forum, the theme was ‘Culture Shock’. The Chairman of ASIC, Greg Medcraft, said:

Every day in recent weeks, we read about bank culture in the media. It seems everybody from the Prime Minister down is talking about it. It will now be an election issue with Labor promising a Royal Commission if elected. At the recent sold-out ASIC Annual Forum, the theme was ‘Culture Shock’. The Chairman of ASIC, Greg Medcraft, said:

“Inevitably, it is the stories of poor culture and poor conduct in the financial industry which are splashed across the front page of the newspaper, which pop up in our newsfeeds, and which are the subjects of heated discussion on social media sites. This is particularly so in recent times – with financial advice, and now Bank Bill Swap Rate (BBSW) and life insurance, on everybody’s minds.”

Former CBA Managing Director and Chair of the Financial System Inquiry, David Murray, shot ASIC a cannonball when he told a Fairfax Media event on 5 April 2016 that it was:

“... extraordinarily disappointing that ASIC should go down this culture tangent which will do more damage than good … It’s anticompetitive, it’s inefficient, and to be perfectly candid, there have been people in the world who have tried to enforce culture. Adolf Hitler comes to mind. “

Is that the first time that ASIC and Adolf Hitler have been used in the same sentence? Murray later apologised for the reference.

Then Malcolm Turnbull weighed in with these strong words at a Westpac function on 6 April 2016:

"We expect our banks to have high standards, we expect them always rigorously to put their customers' interests first, to deal with their depositors and their borrowers, those they advise and those with whom they transact, in precisely the same way they would have them deal with themselves. This is not idealism, this is what we expect.

The truth is that despite the public's support offered at their time of need, our bankers have not always treated their customers as they should. Some, regrettably, as we know have taken advantage of fellow Australians and the savings they have spent a lifetime accumulating. Wise bankers understand that banks need to very publicly demonstrate that their values of trust, integrity, placing the customers first in every way, they must be lived and not just spoken about.

The singular pursuit of an extra dollar of profit at the expense of those values is not simply wrong but places at risk the whole social licence, the good name and reputation upon which great institutions depend." (my bolded emphasis)

Banking versus wealth management

I read the headlines and listen to the wise words about culture from executives apologising for poor treatment of financial advice and life insurance customers with some bemusement. I worked for CBA, State Bank of New South Wales (acquired by Colonial in 1994, which was then acquired by CBA in 2002) and Colonial First State (CFS) for over 30 years. Even when I ran a consulting company, a major client was CBA, and we worked on the merger of the CBA/Colonial businesses.

One of the CBA consulting assignments tells a story of bank culture. CBA wanted to increase the amount of its funding requirements raised from the newly-acquired asset management business. The bank was the largest issuer of securities in Australia, both short term and long term, and CFS (which had merged with Commonwealth Investment Management to form an investing behemoth) already held billions in CBA paper. We met with CFS cash and fixed interest fund managers to discuss how much more could be placed with the bank.

To say the fundies were uncooperative would be an understatement. They looked at me incredulously. Was I seriously suggesting that the bank now expected the asset management business to invest more in the bank’s paper because the bank owned the business? Did the bank really think it could give instructions on where investments should be made? The fund managers said it was their fiduciary responsibility to act in the best interests of their investors, and it was irrelevant what CBA wanted (one of the people saying this was Warren Bird, who now writes for Cuffelinks).

As an experienced banker, my first thought was, “Who do you think you’re talking to?”, followed quickly by, “Do you know who writes the cheques around here?” and similar. I kept the discussions polite and skulked off to plan another approach. That didn’t get far either. We bankers were given a lesson in fiduciary responsibility.

Naked Among Cannibals

I had worked in banking since 1979, schooled in the ways of maximising profit with no formal fiduciary or best interest duty to customers. I chronicled my experiences in the way banks price their deposits, loans and fees in a book published by Allen & Unwin in 2001 called Naked Among Cannibals: What Really Happens Inside Australian Banks. I was reminded of this recently when Noel Whittaker quoted the book in an article for the Courier-Mail on 13 March 2016. He said,

“Despite the predictable protests from the banks [about rate-fixing and life insurance], there is nothing new in this. In 2001, ex-bank executive Graham Hand published his bestseller Naked Among Cannibals, which contained more than 300 pages about corporate greed and unethical behaviour by Australian banks.”

Noel sent this newspaper cutting to me (complete with a very old photo).

Anyone wanting to take a journey into bank culture 15 years ago can read the contents page and first three chapters for free on Amazon books here or purchase the 320 page eBook version here.

The irony of wealth management’s problems

At the ASIC Forum, a speaker from the floor argued that CBA’s cultural problems are caused by its acquisition of Colonial, since the major scandals are not in banking but the wealth management business acquired from Colonial. He conveniently ignored the fact that CBA acquired Colonial in 2002 and has had 14 years to address any cultural problems.

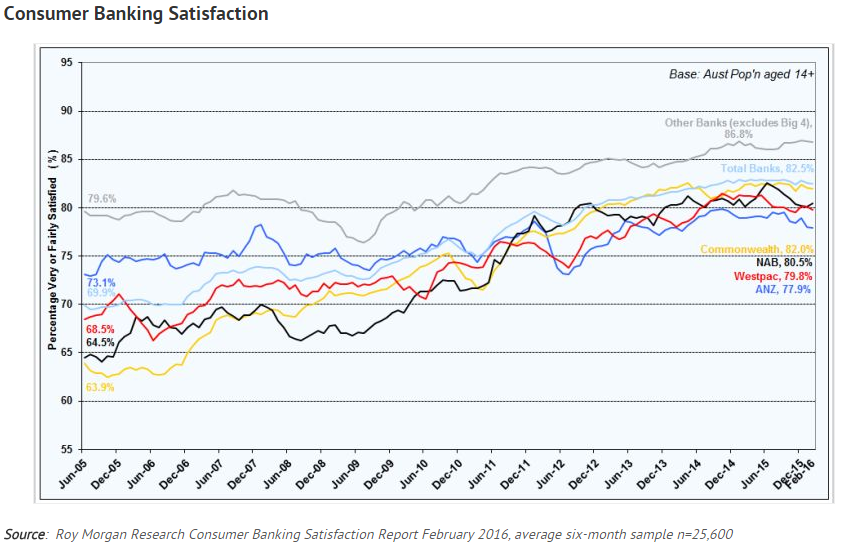

But it’s true that it’s not the banking activities giving CBA’s reputation a beating at the moment. According to Roy Morgan Research, CBA’s consumer satisfaction leads the major banks and is near an all-time high, as shown below by the yellow line. It was a distant last 10 years ago before Ralph Norris’s ‘Sales and Service’ campaign kicked off. There is no doubt that dealing with CBA branch and call centre staff is a better experience now than 10 or 15 years ago.

While the banks are being investigated by ASIC on BBSW rate-fixing, there is no ‘scandal’ around the ways banks price their products, as was a focus of my book. The major culture arguments are directed at the wealth management businesses of financial advice and life insurance.

CFS is the wealth management division of CBA and the responsible entity for the funds offered to retail clients, and it manages billions of dollars of assets across all sectors through Colonial First State Global Asset Management. This ‘vertically-integrated’ structure in the wealth industry is also subject to review by ASIC, including, of course, financial advice.

I did not work in either life insurance or financial advice (neither was offered under the CFS brand), so I will confine my comments to asset management and product development in CFS.

The Corporation Act 2001, Section 601FC(1), under ‘Duties of a responsible entity’ says:

“In exercising its powers and carrying out its duties, the responsible entity of a registered scheme must … (c) act in the best interests of the members and, if there is a conflict between the members’ interests and its own interests, give priority to the members’ interests.”

In the dozen years I worked at CFS, from 2001 to 2012, this responsibility was taken very seriously. It was common for the senior legal representative in meetings to divert management from a preferred course of action because in his view, the action was not in the best interests of clients. There was often a lively debate about how to structure a product or communicate with clients, but someone always made sure the fiduciary duty was front and centre.

That’s the irony for me. Wealth management is taking most of the culture blame, but in my personal experience, in funding, product development and relationship management, the fiduciary obligation was well-understood and respected.

The Prime Minister is right that the support the government and regulators gives the banking system creates an implied obligation to play a social role and consider multiple stakeholders. But his statement that banks should be “placing the customers first in every way” will be a cultural anathema for many bankers.

What are examples of bank cultural problems?

There is no legal fiduciary duty in banking, and so culture and ethics must play a greater role in determining appropriate actions. Culture is the combination of beliefs, values and attitudes that guide behaviour. There is no legal person in meetings saying you have a best interests duty.

I sat on the pricing committees of three banks from 1979 to 2001, and we usually priced our products according to what the market could bear. My book details unscrupulous practices to extract extra margins from deposits, loans and fees. (I admit I’m no longer as well-placed to comment on the present culture of these committees, so someone else can fill this gap).

In 2003, I presented a Perspectives segment on ABC’s Radio National. The text is linked here. The segment was called ‘A Banker’s Dictionary’. I explained five terms - entanglement, milking, mating calls, lagging and parasites - we used in pricing committee which would make any current CEO blush. It’s unlikely in these days of political correctness that the terms are still used.

But more important than the words is whether the activities they describe still exist. Even for an outsider, it’s possible to demonstrate they do.

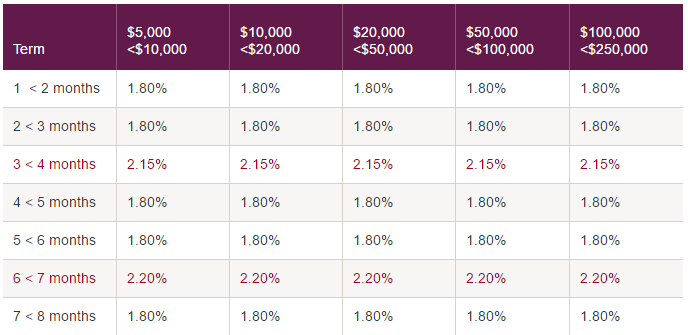

To ensure this article does not single out CBA, consider the current Westpac term deposit interest rate schedule, as shown below for 6 April 2016.

The red rates are the ‘special’ offers. Why is the 3 month rate 2.15% when the 2 month and 4 month rate is only 1.80%? It does not reflect the shape of the yield curve. Westpac has no particular need for 3 month money. It is the rate designed to attract new clients.

But there’s an excellent way to extract more profit margin from customers over time. Until recently, Westpac had the special offer at 4 months. When this deposit matures, the bank will retain the special at 3 months and the 4 month investor will automatically rollover to the lower 4 month rate above. Like all banks, Westpac relies on what we called ‘retail inertia’. The majority of investors don’t call the bank for a higher rate, they simply allow the deposit to rollover for the same term. Then the cycle starts again. As the 3 month depositors who were initially attracted to the special rate approach maturity, the special will switch to 4 or 5 months, and the 3 month people will rollover at a lower rate. Same when the red 6 month rate switches to 7 months.

Is that fair? Few people want 1.8% for 4 months when 2.15% is available for 3 months, but 1.8% is what the maturing deposits will rollover into.

It’s very profitable. The interest savings on billions of dollars of term deposits rolled over at a saving of 0.35% are worth millions of dollars a year in extra revenue. Banks watch the maturity pattern by term of original lodgement and set the special rates where the least number of rollovers will receive the higher rate. We called this ‘milking’ the deposit, although I doubt such a pejorative term is now acceptable.

For the record, CBA now places maturing term deposits into a Term Deposit Holding Facility (earning a rate of 1% for amounts between $10,000 and $99,999) until instructions are received from the client. You can judge whether this is a fairer policy.

Banks also know that the more a customer is ‘entangled’ in an account, the less likely they are to leave. The best examples are at-call (cash) transaction accounts which link to direct debits to pay electricity bills, loan repayments, credit card balances etc, and direct credits receiving interest, salaries, dividends, etc. These accounts are so entangled that the client cannot face the paperwork of changing to another bank or product. So why would the bank bother paying a decent interest rate on the balance? Most money in at call or cheque accounts receives negligible interest despite all banks or their subsidiaries having more attractive deposit products. Shall we tell the client to switch to the online account that pays 3%? Are you mad?

There are many examples like these: slowly lagging cash rate reductions into lending rates but passing on increases quickly, or charging interest rates on credit cards of over 20% (which have so many embedded direct credits and debits that it’s hard for people to leave). And the mysterious calculations of early repayment fees on fixed rate loans, as previously described here.

My book goes through the evidence in a far more systematic way for any bank board member who wants to explore how much these practices are in the past or the present.

Are we at a cultural turning point for banks?

There has never been as much scrutiny on bank culture as in the last few weeks. Every major bank at either CEO or Chairman level has made a statement about customer focus and ethics. The Chairman of National Australia Bank, Ken Henry, said in a speech on the future of banking on 5 April 2016 that he even welcomes the criticisms:

"Any business that really has a passion for customers has to be open to criticism and it has to welcome, even encourage, debate. Importantly, being open to criticism and welcoming of debate is not only in the interests of customers, it is very much in the interests of shareholders. This is an important part of what it takes to create a strong and sustainable business."

I went to university with Ken, and he's a good bloke. But I do wonder if he has closely studied his bank's pricing policies when he says:

"In a successful business the customer drives product design and the suite of products offered. No customer is encouraged to buy something they don’t need or charged more than they need to be charged to cover the cost of providing the product. No customer of a successful business buys something that they don’t understand well enough to have a high degree of confidence that the product will deliver what they want, when they want it."

That's a high bar to jump. How does it fit with NAB transaction accounts paying interest of 0.01% and NAB credit cards with interest rates of 21.74%?

For the moment, change seems to come only when forced on the banks, as Carl Rhodes, Professor of Organizational Studies at UTS, recently summarised:

"This is not an ethical responsibility the banks have taken on voluntarily through their 'ethical cultures'. Responsibility was thrust upon them as a result of the actions of citizens, employees, regulators, and journalists. If it wasn’t for them, the scandals would remain covered up."

Why is wealth management the target?

So why is CBA permanently in damage control around wealth management more than banking?

There’s no simple explanation. The financial advice failures were exposed by the GFC when people who had been placed into inappropriate products (such as those sold to clients of Storm Financial) lost a lot of money. With some exceptions, the complaints were due to the loss in value of the investments, and then the bad behaviour was uncovered. If the market had continued to rise, little would have surfaced. Who would be complaining about leveraged exposure in a booming market? And it's a much better story to show a person suffering after a heart attack and being denied a life insurance claim than a $30 fee on a dishonoured cheque. No depositor in an Australian bank has ever lost money, because the Reserve Bank and the government always steps in. The deposit guarantee during the GFC is an example.

I’m not excusing the bad practices in financial advice or life insurance, but rather, pointing out that in my experience, there were at least as many cultural and behavioural shortcomings in banking, beyond the rate-fixing and rogue traders we read about. As David Murray said when asked how effectively banks are embracing culture:

“Not very well at all. I think that we’re in a process now of sorting this out. In the public mind, it’s all to do with ethics, but ethics is a necessary but not sufficient component of solving the problem.”

To all my banking friends who hate me writing this, remember that whistleblowers are now meant to be revered, not reviled. Culture has, apparently, changed.

Graham Hand is Editor of Cuffelinks and comments from any current member of a bank pricing committee are most welcome. And anyone else, of course.