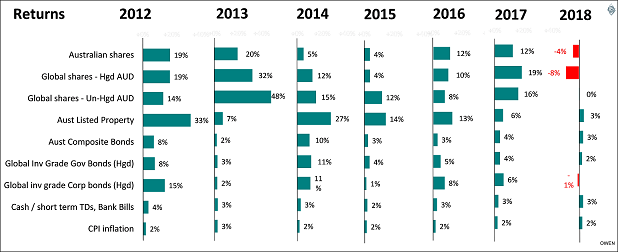

A year ago, at the start of 2018, we wrote that 2017 topped off an unprecedented six-year rally in every major investment asset class. Never before in history had each of the main asset classes enjoyed positive ‘real’ (after inflation) returns for six consecutive years. The previous record was four consecutive years from 1925 to 1928, before the 1929 crash and 1930s depression.

The end of the illusion

We also noted that the 2012-2017 rally was unlikely to continue into a seventh year because the main drivers of asset returns were fading. Central banks were scaling back and reversing their 'QE' (quantitative easing) asset buying programmes, the US Federal Reserve was raising interest rates and Chinese growth rates were slowing. Asset prices had risen everywhere in the boom but it was an illusion - a house of cards propped up by ever-increasing piles of debt built up by governments, companies and households since the GFC.

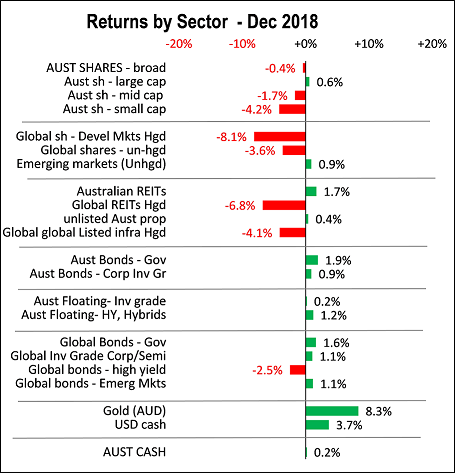

As it turned out, 2018 saw negative returns from share markets almost everywhere and lower returns from other types of assets.

During the six-year boom, many investors became complacent and started to believe that asset prices would keep rising forever – just like the euphoria of previous booms before they burst. People forgot about asset allocation because everything went up. The previous five years from 2007 to 2011 were more like the usual pattern, with a mix of positive and negative returns. The only year when everything went up was 2009 in a rebound from the 2008 crash.

After having been relatively bullish on shares after the 2016 Brexit vote and Trump election, we reduced allocations to Australian and global shares in portfolios during 2018. Our two most likely scenarios were: 1) a sudden inflation scare, and 2) a global slowdown scare. We reduced the currency hedging on global shares to prepare for a fall in the Aussie dollar, and we added US dollar cash and gold. By July and October 2018, we removed exposures to global corporate bonds and increased government bonds.

With QE now over in the US and Europe and interest rates rising in the US, 2018 was a return to the more usual pattern of mixed returns, and 2019 will probably be similar with positive and negative results in different asset classes.

Asset allocation is well and truly back

Even when equity markets fall, portfolios can be protected by asset allocation and hedging strategies. For example, unhedged global shares usually smooth the pain because the falls in global shares are partially offset by currency gains as the Australian dollar falls, as it almost always does in global sell-offs. Gold (in Australian dollars) and US dollar cash were the best-performing assets in December 2018, as shown below, and also for the whole of 2018. The latter two are not traditional long-term holdings in most portfolios but unusual global conditions sometimes call for unusual strategies.

In the booms, the most common questions I hear relate to a fear of missing out, such as ‘Should I gear up?’ or ‘Which do I like better: [bubble stock A] or [bubble stock B]?’, and the like. A year ago the markets were booming, especially in tech stocks, crypto currencies, ‘fintech’ and emerging markets. The questions were almost all about how to get in on the action.

However as soon as there is a wrinkle in the markets the questions turn to impending disaster, such as ‘Is this another GFC?’ or ‘Is this the end of the world as we know it?’

Four main factors involved in market crashes

I have studied many different types of market bubbles and busts, and four main elements tend to be present in almost all bubbles that ended in busts. Here is a summary, together with brief comments on the current environment and a current ‘risk rating’ for each:

1. Over-pricing of assets - Moderate to High risk

Before the late 2018 sell-offs many markets were over-priced, including US and Chinese tech stocks, healthcare and global consumer brands. The price falls in recent months do not reduce the risk of collapse. Over-priced markets never drift back quietly and calmly to fair pricing. They tend to swing wildly from over-shooting savagely on the upside to over-shooting savagely on the downside. Markets are driven by wild emotions, not quiet logic.

2. Speculative fever - Moderate to High risk

US and Chinese tech stocks led the recent boom in share prices. We also saw the recent boom in dozens of new ‘crypto-currencies’ and ‘initial coin offerings’ that jumped on the Bitcoin bandwagon, and also the booms in ‘fintech’ and ‘green tech’ stocks that are as revenue-free and profit-free as the 1990s dot-com boom. Busts in crypto, fintechs and green techs are unlikely to expand into broad market collapses unless losses start to trigger broad selling and margin selling in the broader market, as they did in the 2001-02 tech wreck, and in 1929.

In Australia the boom in high rise units is on a par with similar speculative property booms in Australia in the 1880s, early 1970s, late 1970s, and late 1980s, all of which ended in banking crises, widespread bankruptcies and corporate losses, deep economic recessions and broad share market collapses. Prior busts were triggered by sudden withdrawal of capital and/or interest rates hikes. This time it is the sudden withdrawal of capital from China and from the local banks.

3. Leverage - High risk

US margin loan volumes are on a par with the peaks prior to the 2008-09 GFC and 2001-02 tech wreck, but not as high as in 1929. This is a clear sign of extreme debt-fuelled speculation.

The extremely low interest rates since the GFC have led to a massive build-up in debts at all levels in almost all countries: government debt, corporate debt, housing debt, personal loans, and margin loans. This makes the entire system highly vulnerable to interest rate rises. The likely impact of rising US interest rates and rising US dollar on emerging market governments and companies was the main reason for removing emerging markets shares from our portfolios before they fell in 2018.

4. New financial instruments and participants - High risk

Not only is this a high risk condition present in the boom, it is also a likely candidate for the trigger for a broad crash. In 2008, it was the sub-prime financial innovations like Option-ARMs, MBSs, CDSs, CDOs and the like that underpinned the 2000s boom, and triggered the US banking crisis and in turn the sudden collapse in bank finance, the instantaneous global banking contagion and the broad stock market collapse in every country.

The explosive growth of Exchange Traded Funds (ETFs), High Frequency Trading (HFT), and ‘algo’ (algorithmic trading) now dominate markets. ETFs control nearly half of listed investment markets globally, and investors assume they are risk-free in the sense that they can instantly sell all holdings necessary to meet any sell orders. In an asset class such as high-yield bonds, this may be difficult. Some ETFs rely on derivatives or gearing which are untested in a crisis, relying on thousands of counterparties around the world.

What lies ahead?

Returning to the two big questions.

First, ‘Are we going to get another GFC-like sell-off?’ That’s easy. Of course we will! We have had several 40%+ sell-offs in the past, with one every couple of decades, and we are sure to see another in the future.

Second, ‘Are we at the start of one now?’ That is more difficult.

The conclusions from the above analysis are:

a) Many of the conditions in past cycles are present now: markets are over-priced, including shares, bonds and properties (commercial and housing); speculation is rife in a number of areas; there are high levels of debt at all levels in almost all countries; and there are also a number of financial ‘innovations’ that could present unknown risks or unforeseen consequences.

b) There are also several potential candidates for triggers for a broad collapse: rising interest rates, government or regulatory attacks on business; a possible collapse in trust in a major element underpinning market confidence; and also the possibility of military strikes or hackers rattling investors and triggering a spiral of sell orders.

What to do with portfolios now

All we can do is assess the conditions as we see them, identify the sources of risk, and steer the ship toward areas where the opportunities are greater than the risks. Usually this means going against the herd.

US and China remain the centre of attention. President Trump will run into more trouble with Congress, with the Democrats back in control of the House. There are gathering signs of slowing consumer confidence and spending, and the Fed is likely to raise rates further.

China is entering another cyclical slowdown, and this is dragging down commodities prices. This is bad for commodities exporters like Australia and it could also trigger another bout of global bankruptcies in oil/gas/steel companies like in 2015. Chinese corporate defaults are also rising rapidly. Xi has anointed himself Emperor for life but he is coming under increasing pressure from within the party to play hardball with Trump as he is being blamed for the trade war. Chinese stimulus announcements rebooted global markets in March 2016 but this time Xi appears to be favouring military expansion over internal stimulus.

Locally, the Hayne Royal Commission is due to publish its final report shortly. The recommendations are sure to call for radical and far-reaching changes to the current system of cartel price gouging. Much depends on the outcome of the Federal election which is due by May 2019. This is likely to see major changes to both the government and the make-up of the legislature, in particular the Senate. On current numbers Labor is likely to win but will be hampered by a fragmented Senate. This will make it difficult to implement many of their policies including scaling back negative gearing, increasing capital gains taxes and removing franking credit refunds.

Prices of Australian houses and especially high rise units will probably keep falling. The main sources of funding are likely to continue to restrict supply with banks restricting lending and the Chinese government limiting capital outflows. Bad debts and bankruptcies will gather pace but it is likely to take some time to build to crisis levels that impact broader spending and demand.

It's a time to remain defensive in portfolios with vigilance to make further adjustments to protect capital and capitalise on opportunities.

Ashley Owen is Chief Investment Officer at Stanford Brown. This article is for general information only and does not consider the circumstances of any investor, and is based on markets at the time of writing.

Ashley will be presenting on his outlook for markets on 7 February 2019 in Sydney. Stanford Brown is offering 50 complimentary tickets to Cuffelinks readers. For details, please contact: [email protected].