(Editor's introduction: Peter Thornhill is well-known to our readers for advocating a multi-decade investment strategy based on the long-term merits of industrial companies for income. For example, to show his consistency over time, his previous articles in Firstlinks are here. In this short update for 2022 numbers, he again checks the long-term return from industrial shares, adding a comparison with listed property. He argues that for investors with the right risk capacity and investment horizon, there's only one place to invest).

***

It's that time of year when the data allows me to update the presentation many readers are familiar with, based on my books, courses and articles.

There are many definitions of 'investing'. For me, it means one thing: The use of money productively, so that a regular income is obtained.

This guides my portfolio decisions. I do not focus on the so-called volatility of share prices. Over decades, I see a rising stockmarket producing ever-increasing dividends. And that's income for me.

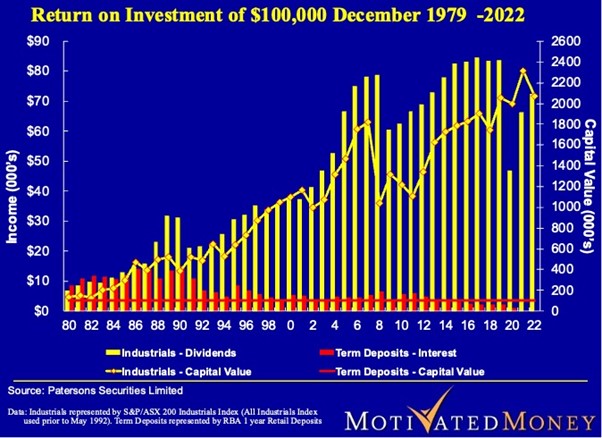

Industrial share versus cash since 1980

Let's start with my key slide, Australian industrial shares versus cash. Term deposits and cash are where many investors hide for safety, but how do they define risk?

The ‘Covid crash’ of 2020 is like all previous market setbacks. They are relatively short-lived.

Whilst this time, share prices were not overly affected, dividends were severely hit. However, as expected, dividends are recovering quickly as the effects of the lockdown dissipate. If one is in tune with history then this pandemic is no different to those we’ve been exposed to for the last 2000 or so years.

What about Resources and All Ords?

The recent strength of resources stocks supported by supply problems from Ukraine and Russia may lead some investors to argue for inclusion of these companies in a long-term portfolio. Or the broader All Ords Index rather than only industrials. But as the following chart shows, it does not pay off over time.

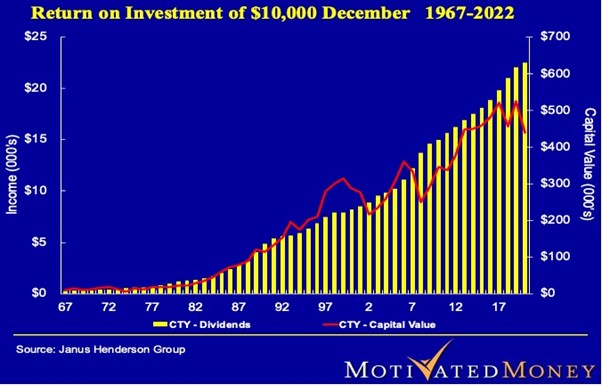

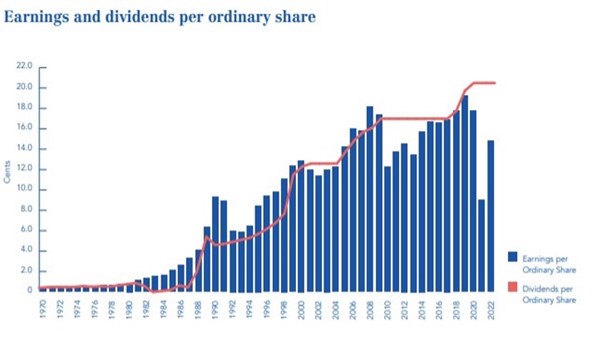

My 56-year investment

The next slide regular readers will be familiar with. It is a UK-listed investment company which forms part of my investments resulting from an 18-year sojourn in the Old Dart back in the 70’s.

Despite all the current and prior market turmoil, this chart is always a source of comfort. An income that has risen every year for the last 56 years.

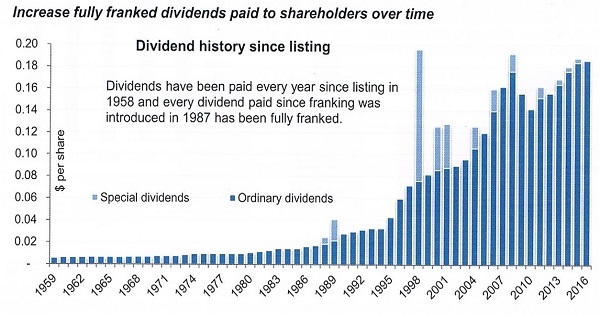

In our home market, there are similar Listed Investment Companies (LIC’s) displaying the same characteristics.

Milton is a great example, although it has now merged with Soul Pattinson.

The Soul Pattinson dividend history is equally comforting.

Another one of my favourites is Whitefield which is celebrating its 100th anniversary this year.

My strong preference for this one is the fact that it only invests in industrial companies and no resources.

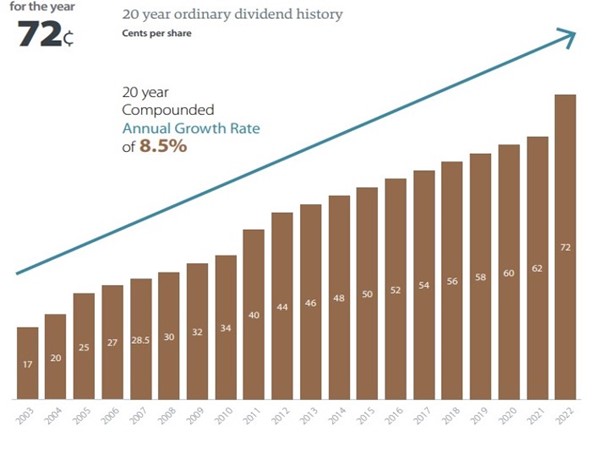

Despite earnings volatility, the ability of a LIC to smooth their dividends is clearly evident.

Suffice to say that with an ever-growing income stream over 30, 40, 50+ years, one’s life can remain focussed on what is really important: family, friends, and career.

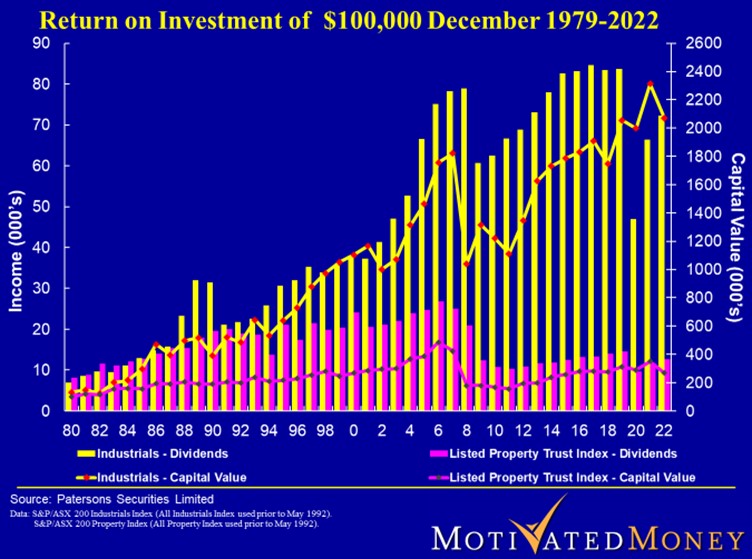

Finally, let's check the long term of listed property?

Firstlinks often includes articles on the benefits of investing in property, including listed securities. It's an asset class that probably appeals to many Australians.

I believe adding property and resources to industrial shares is a no-no. Whilst it may slightly reduce the volatility, the opportunity cost over a lifetime is lead in the saddle bags. Volatility does not measure risk!

Despite some good periods, property suffers times of significant setbacks.

10 predictions for 2023

Like religion, financial forecasting meets a human desire to know the unknowable. It doesn’t matter whether the forecasts are accurate or not, people sleep better at night under the assumption that there’s a predictable future laid out ahead of them. Here are a few of mine for 2023:

1. A lot of things will happen that no forecaster thought to include in their predictions for 2022. These events will include the obvious consequences of the current economic and political environment. So obvious, in fact, that they weren’t included in the predictions.

2. Many things won’t happen that many forecasters did include in their predictions for 2022. This will be a result of unforeseen circumstances, black swan and six sigma events, annual anomalies that crop up one in a million years.

3. A small number of the vast number of predictions about 2022 will randomly come true and the predictors will be proclaimed gurus. This will be despite the fact that it was their 1,000th prediction and the first one they got right.

4. All predictions will be adjusted throughout the year so that the forecaster’s final prognostications, announced on Christmas Eve 2023, will be very close to accurate.

5. Those fund managers who outperform for the year will cite their skills, systems, intelligence and uncanny ability to time the market as the reasons for their outperformance. While acknowledging that past returns are no guarantee of future returns, the past returns will be included in advertising materials in very large font.

6. Those that underperform will cite the randomness of markets and that any one bad year will obviously be followed by a good one, because underlying it all they have superior skills, systems, intelligence and uncanny ability to time the market. Marketing materials will include performance statistics over a more appropriate time frame.

7. Dividends will be more important than capital gains, unless the market goes up a lot. If the market goes up a lot, capital gains will be more important than dividends.

8. Every CEO in the country will be in the top quartile of CEOs in the country. They will get paid accordingly.

9. Markets will fluctuate. The All Ordinaries will go up, down or sideways in both the first and second halves of the year.

10. There will be a new computer trading system that will infallibly make you rich overnight as none of the systems sold over the last 20 years seem to have worked for anyone else apart from the spruikers.

Peter Thornhill is a financial commentator, author, public speaker and Principal of Motivated Money. He runs full-day courses in the major capital cities explaining his approach to investing "in the vain hope that not everyone is frozen with fear".

This article is general in nature and does not constitute or convey specific or professional advice. Share markets can be volatile in the short term and investors holding a portfolio of shares will need to tolerate short-term losses and focus on a long-term horizon, and consider financial advice.