Recent press would have you believe that Chile’s pension system is the solution to the perceived cost problems in Australia’s superannuation system. This is due to a combination of media sound biting of a report by the Grattan Institute (and subsequently the Financial Services Inquiry) which, while interesting and a motivator for important discussion, is ultimately incomplete, open to alternative interpretations, and in my opinion flawed. The Australian superannuation system is highly complex – there is no silver bullet which takes it to the next level.

Chile’s default fund auction system

Chile has a well-regarded pension system. The overall system, which includes the government- provided pension, was ranked 8th out of 18 countries (each selected as having a developed retirement income system) in the 2013 Melbourne Mercer Global Pension Index (Australia ranked 3rd). The FSI highlighted an important feature of their system in its Interim Report:

“Other mechanisms could also be deployed to drive fees down. One example is the approach introduced in Chile in 2008, where — unlike Australia — superannuation contributions of all new members are placed in the same default fund. Default fund management is auctioned on the basis of fees, creating stronger competition between funds for default fund status. Since these arrangements started, the fees charged by successful bidders in Chile have fallen by 65 per cent, although fees on other funds have not fallen to the same degree.”

This comment was likely based on a report produced by the Grattan Institute titled, “Super sting: how to stop Australians paying too much for superannuation”.

Grattan Institute analysis of Chile’s pension system

In Chile, workers contribute to approved pension funds, known as AFP’s (Administradora de Fondos de Pensiones). Currently there are six AFP’s each offering five investment options based on investment risk (simply named funds A, B, C, D and E). The Chilean government implemented a broad range of pension system reforms in 2008, and to address concerns regarding the cost efficiency, the government introduced a tendering process. Every two years, all AFPs tender to be the default fund for new contributing workers. New defaulted fund members cannot leave the directed AFP for two years but can switch investment option. Each option charges the same administration fee. All existing members of the default AFP also have their fees reduced to the new level. Since introduction, the Grattan Institute notes that the successful tenderer fee has fallen 65% to a fee less than 0.20%. This headline number is definitely worthy of attention. Unfortunately AFP’s with large memberships have not been winning the tender recently and so the fee reductions have not benefited the majority of the population.

In my opinion the Grattan Institute adopts the view that a certain way to improve performance is to reduce fees. The logic of such a view, also shared by the Super System Cooper Review, is that investment management makes little difference to performance but fee differences make a large difference in performance. To support their view they undertake analysis which shows that:

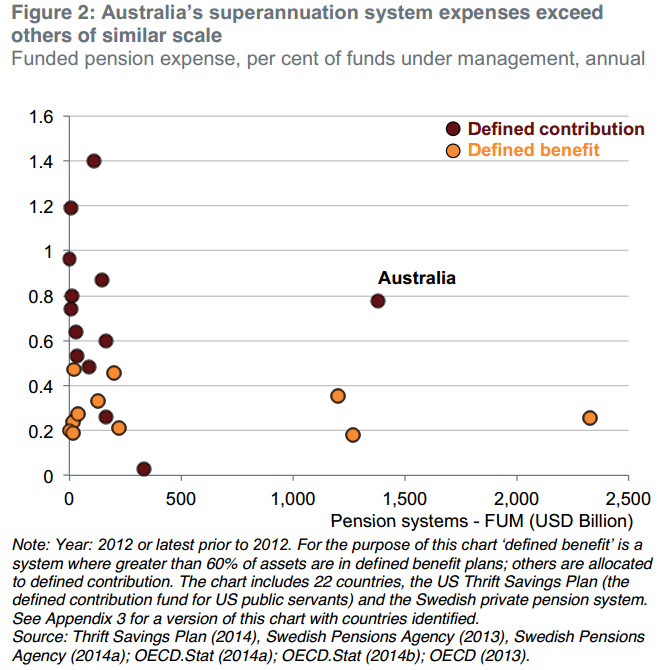

- Adjusted for system size, Australia’s super fund fees are much higher than those in other countries, as demonstrated in the following chart taken from the Grattan report:

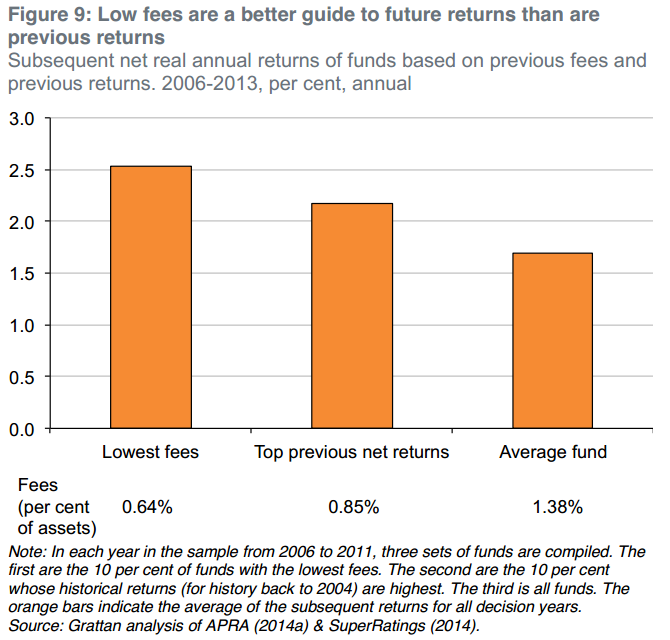

- Outperformance does not persevere (if a fund outperforms in one year there is little continuation of that outperformance in subsequent years). This argument is summarised in the following chart:

- Fees are high because of the failure of account-holders and employers to put sufficient pressure on super funds to reduce fees

- Super funds seek to differentiate by providing a range of product features and services, rather than focus on fee reduction

- MySuper will not result in substantial fee reductions.

To reduce fees the Grattan report proposes a two-part solution:

- Select default funds in a fee-based tender (similar to the Chilean process)

- Encourage a more active choice program through the Australian Tax Office hosting a ‘choice platform’ which compares an individual’s current fund to that of the default fund (tender winner), and allow an opportunity to instantly switch to the default fund.

(As a side note, the Chilean experience of tendering is not viewed as a universal success. In 2013 a special committee of the Senate approved a range of measures including creating a publicly-administered alternative to the current privately operated system. This is in response to concern that the tendering process has not delivered population-wide benefits).

The Grattan Institute deserves commendation for producing some analysis and venturing some opinions which should, at the least, require self-reflection amongst super fund providers. Ultimately I disagree with their views and believe that their proposal would fail if implemented. Understandably there will be differences in opinion when a report is produced by people who are not directly involved in the superannuation industry (the three principal contributors are from an economics / academic background). While sometimes great industry innovations are generated by those from outside an industry, I don’t think we have a plausible game-changer in this case.

I make a number of points in response to the Grattan Institute:

- Global cost comparisons have historically been difficult because every country’s retirement income system has a unique structure providing different features and services. Some services are provided or subsidised by governments. A simple chart (the first one above) as provided Grattan does not tell the full story (but clearly raises important questions)

- The assessment of active management skill is flawed, most notably in the statistical tests applied against the objectives of the system. Super funds focus on long term performance and ultimately retirement outcomes, yet the statistical testing by the Grattan Institute focuses on the perseverance of short term performance. I question the relevance of this statistical test, especially when the large differential in fees observed in the early 2000’s no longer exists. Perhaps the short term test is conducted because it is more difficult to test longer term performance, as a much lengthier set of data is required. The key question is whether quality active management applied in well constructed portfolios will improve a fund member’s long term retirement outcome. This doesn’t just mean higher returns; it could also mean reduced risk. Surely the debate on active management needs to be a broad and forward-looking one. Based on the flawed construction of many passive indices, evidence of costly behavioural biases, and my own personal experiences of the impact of high quality active management on the return and risk outcomes of a portfolio, I believe that active management does have potential benefits. Surely super funds should have the choice about whether and how much they incorporate active management, rather than have that choice regulated away.

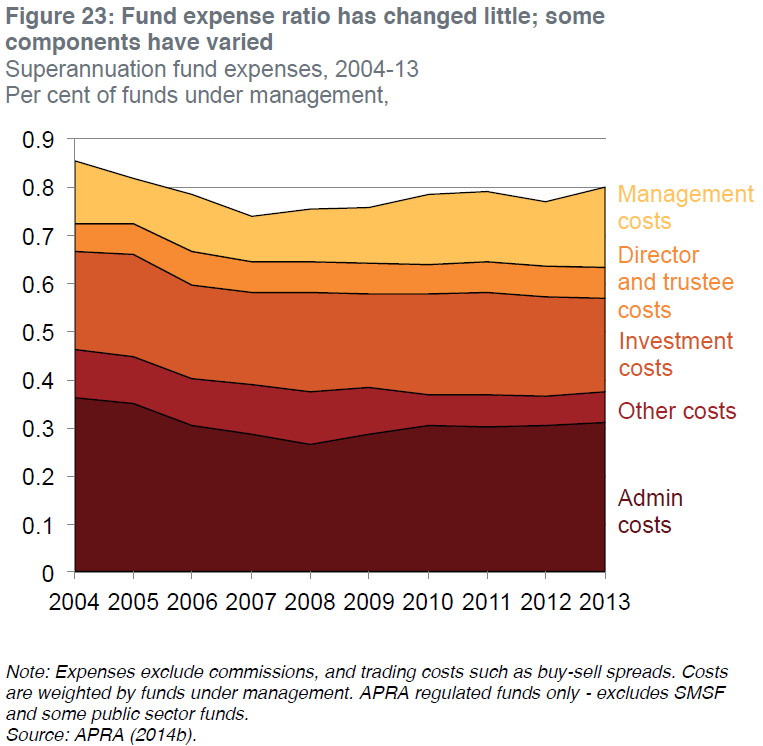

- The report fails to address the issue of where cost reductions can be derived, rather alluding to the potential for cost savings similar to that experienced in Chile. Yet the Grattan report itself provides a useful chart on this very issue:

- Based on this chart, from which areas can cost reduction be derived? It appears that investment costs are already quite low at circa 0.20%. Even if we assume a more conservative (higher number) for investment costs, we can see that the impact of a shift to passive management will deliver far lower benefits to those achieved in Chile. Indeed we can see that administrative costs alone are higher than the total fee for Chile’s last AFP tender!

- Finally, recommendations need to have a high chance of succeeding in practice. In this case success should be measured as system cost reduction. Undoubtedly the creation of a super choice platform would be a costly exercise. It is debatable how much choice would actually take place given the disengagement of many and the alignment of workers to their industry super fund. It would also not surprise to see funds increase advertising expenditure around tax return time – another cost to members with no investment return benefit.

Complexity of our super system

Cost is a crucial issue on which regulators and the industry need to maintain constant focus, but I believe the cost debate has many nuances to it. Does the system as it stands provide too many services and features? What is the economic cost of the substantial choice provided to Australians? What is the cost versus benefit of the substantial regulatory requirements placed on super funds? Which areas of the cost structure (as per the third chart) have the greatest potential for cost reduction? Unfortunately given the complexity of our system, a simple solution is unlikely to succeed; rather an ongoing collection of micro reforms, combined with ongoing fund merger activities, will lead to system cost reduction.

A final comment on the active management debate: in my opinion the investment management industry is experiencing a period of unprecedented dynamic change. The focus on member lifecycle outcomes, post-retirement solutions, the balanced versus lifecycle debate, smart beta and minimum volatility investments, represent just a small number of the current challenges, or opportunities, depending on your view. The lens through which performance outcomes are assessed needs to be refined further. It is those from within the industry which need to provide greater leadership in this area. From here we can then justify the sensible use of active management strategies.

David Bell is Chief Investment Officer at AUSCOAL Super. He is also working towards a PhD at University of NSW.