Coinciding with 30 years of compulsory superannuation, the start of a new financial year and the introduction of the Retirement Income Covenant, we surveyed our readers to find out how they spend their retirement.

As the survey was limited to retirees, the response from about 700 readers is excellent. Thanks for participating and sharing your wisdom from experience.

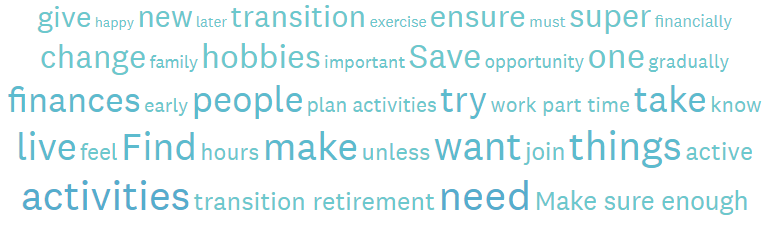

A complete analysis of the results with charts is in this article. Here we focus on one of the questions.

Do you have any tips for people approaching retirement?

The word cloud from this question neatly summarises important points:

One of the main messages concerns time management. Use it well. Retirees enjoy the freedom after a lifetime of work and the ability to spend more time with family and other interests but don't waste the opportunity. Make it a period without money troubles by owning your own house and using super well.

We received thousands of comments and it is impossible to feature them all in an article, so we have moved them all into a PDF. But here is a sample:

- Definitely plan something productive in your week. Gardening, volunteering, renovating or whatever helps maintain a sense of worth. Golfing and cycling are great but in my experience don’t fulfill the need to feel productive in the long term. Also, if you are spending hours a day checking and researching your investments, just be aware that you are not doing it “for your retirement”, you are making it your retirement. Which may be fine.

- Take one day at the time and all fall into place in time.

- Don't. The social aspect of work, the sense of purpose, can be hard to replace unless you have a serious set of interests or family to be involved with. Keep working - for many professionals it defines who you are.

- Be open minded to continue learning new things away from where your career took you. Give back to community where you can and ensure you have a big enough nest egg that pesky market fluctuations aren’t an issue.

- Get out and enjoy. “SKI”…. (Spending the Kids Inheritance)

- Just do it if you can afford to...Life is short...make sure you retire debt free, especially with no mortgage

- Make the decisions together with your partner if you are lucky enough to have one, about where to live and how to accommodate the priorities of both of you.

- You need to break the work habit. After my wife and I retired, we went on 3 month world travel in year 1 and year 2. This broke the daily cycle which I found important.

- There’s no magic moment or a time when one should retire

- Have a wide range of interests, care for others and do not let the ‘Old Person‘ in.

- You have to keep busy even in retirement. Busy people are happy people. Find some hobbies. Do some exercise. Lots of people do gardening which is what I do. I enjoy it and it keeps me fit. I also go for a walk in the morning. I enjoy being outside. I go to the National Parks a lot. I only spend limited time inside at the computer. You need something that keeps you jump out of bed in the morning. Something to get up for. Everybody has things they like. Pursue something you love and just keep going until the end. Don’t sit all day in the most comfortable chair. Do something. Challenge your brain every day to hopefully keep dementia away.

- Just do it. It is wonderful being fit enough to still be able to travel and do physical activities Don’t wait too long

- Have a rough idea of how you will use your new found time. Plan a few years ahead, its great to work towards it, setting your goals. Live within your means.

- Do it gradually 2) Keep interested and involved 3) By all means help look after grandchildren but beware of committing to a regular schedule. It becomes a tiring routine and grandchildren may start taking you a little too much for granted.

- Do it in mid 60s. Speaking to lots of my older golfer friends when you hit 70, you won't be able to physically do a lot of things as well as before and health problems will start to set in-unless you are one of the lucky ones-but I don't like your chances.

- It took me about 2 years to fully appreciate retirement. If you can do some part-time work or voluntary work for that two years the transition can be easier. Work on keeping physically fit. Make sure that you retain a significant circle of friends and see them often. Regular catch-ups over a coffee at a cafe works for me.

- Look after your health in the years well before retirement and be financially secured.

- Develop new interests, reach out to meet new people, go and search for interesting and useful activities to participate in the community. Nobody will come looking for you.

- Ensure you make a list of things you want to do in the rest of your life. I’m still to take up fly fishing!

- Don't let yourself get confused by listening too much to all the wisdom of third parties who have not retired but want to give you advice what you need to do. Do what you want and think is best for you. Whether this is gardening, cycling cooking or tinkering with electronics or SW development does not matter as long as you and your partner give each other some free space and enjoy the majority of time together. Eat together speak to each other, enjoy your company. Happy days!!

- Talk to people who have retired. Transition. Educate yourself on potential pitfalls.

- Do the homework regarding the funding of retirement.

- Work out what you really enjoy about your current employment and do it on a smaller scale.

- Stay active in some role, either with sport or social activity, or volunteering, grand parenting, or in casual paid work - as these all add some structure and timetable to your week. Don't waste your days laying about or watching TV. Get out and about in some form and enjoy the freedom you have worked hard for!

- Don't stop work completely unless you have no choice. Keep you options open to continue working part time and take your time transitioning to full retirement. For most people, if you think you have enough funds to retire then you probably don't have enough funds without compromising your desired lifestyle excessively.

- Make sure you have enough money and maintain social and family ties, have some interests and keep fit.

- Corporate employment can deskill you for a life of independence. Approaching retirement pick up some individual skills that would enable you to pickup short term but well paid contract work.

- I took advantage of the pandemic to really scrutinize my spending habits and budget. I realised I didn't need as much money in retirement as I originally thought and therefore was able retire earlier than planned.

- Maximize your superannuation. Make sure you have plenty going on in your life outside of work.

- Pay off your house and top up your Super. Plan lots of travelling before you are in your 70's.

- Buy new stuff if required like fridges, cars, washing machines etc. They are expensive when you don’t have an income coming in

- Look to your superannuation, because that will be the foundation on which you can live a comfortable life.

- Gradual if possible. Ensure money flow is more than adequate for what you plan. Think carefully about what you want to spend your time on. Ensure you have friends or join a group to make new friends. Volunteer using your talents

- Salary sacrifice. Being financially independent removes a huge worry.

- Keep in touch with your friends and family. Try to minimise debt before retiring, if possible. Have a go at a new interest, meeting new friends and contacts in the process.

- Save as much as you can while still working. If you have had a job where you work long hours, try going part time before stopping altogether. This will help with the transition.

- Have interests you really enjoy. Eg. My membership of outdoor group with many activities. I found it difficult to find a meaningful volunteer role due to my travel activities as many rely of frequent and regular attendance say 48 weeks per year.

- Become exposed to stock market investing (even in small way) ASAP. Join as many local activity groups before retiring (e.g. local politics, service and community interest clubs, Aust. Shareholders Assn., Sporting Clubs)

- Don't be a burden on others because you didn't arrange wills and get rid of excessive possessions

- Men are bad social animals, ring people, make lunch dates. Must have people.

- embrace the change and make a better place to live for yourself

- Wind down your spending as you near retirement to see how much money you can live on.

- Don’t do nothing. Find things to do regularly even if they are very minor

- Keep yourself motivated. Step outside your comfort zone. Keep learning

- I tried to scale back from 5 days a week to 4 days a week but the project work kept on coming even on my days off. The scale back didn't really work but still got a pay cut.

- Plan and write your lists and then talk to those you know who have retired from your particular field. Think carefully about what you WILL do and then judge if this is practical for you. Visualize yourself as a retired person and then think about your lists of to do's and consider how practical they are depending on your health, finances, spouse's thoughts and aspirations

- Make sure you have enough money to avoid having to deal with Centrelink.

- Plan ahead and engage with your hobbies and any planned volunteer activities. Work part time near your retirement Have a financial plan.

- Retire early while still fit mentally and physically.

- Most people overestimate in their minds just how much money they need to retire comfortably. Whilst its not a small amount, its not a billion dollars either, so don’t put yourself in an early grave trying to achieve a level of wealth that’s unrealistic for the actual lifestyle you intend to live

- I strongly favour tapering into retirement: gradually reduce working hours and take on outside interests over time. Don't make a step change.

- Plan to ensure that you have things to do in retirement. If you having nothing to fill the vacuum, you will become bored and depressed.

- Staged retirement. Keep your friends, Do not go to live elsewhere, especially coastal holiday place.

- Don't feel guilty of just taking it easy and do not be pressured into doing things you don't want to.

- Prepare for what you will do on the Monday morning of the start of your retirement.

- Try to design a glide path of gradual move to no work. Secure some part time activity before making the jump. Retirement (even an active one) doesn't have to be expensive. Guard against relevance deprivation. It is not speed that kills, it is the sudden stop.

- I went to my first retirement seminar when I was 30 years old, not when I was 60 years old. Since that day I have been able to plan backwards from my planned retirement at 60yo. Unfortunately I had to medically retire at 57 but the plan was in place

- Keep yourself busy especially volunteering with a purpose. Keep yourself fit. Enjoy sleeping in some days. Walk the dog daily. Make sure you have enough money to retire comfortably without worry when the economy goes bad.

- Engage a financial planner even if it’s only to ensure you are on the right track for retirement & the future ahead. Ideally educate yourself about your investments long before you retire. If possible go from full time to part time work to ease into retirement.

- Natural eating (no medicine, and alcohol is not medicine). Natural exercise (including climbing, swimming, jumping). Natural risk-taking (physiological, mental, financial).

- Read as much as you can on the issues, especially on funding and relationships. Having enough income helps adjust to the obstacles that will come sooner or later. I found 'The Barefoot Investor' an excellent guide to investing and it summarises my attitude after 40 plus years of investing. One of its concepts is to support charities as an integral part of your expenditure.

- Engage a financial adviser to plan your "portfolio" and mechanics of implementing a structure that can provide optimum financial benefits from the opportunities available.

- Contrary to the normal advice - I'd say don't overplan. I certainly didn't as I didn't intend to retire when I went on Christmas holidays but at the end said to my wife 'for the first time every I don't really feel like going back to work (I loved my job). Look for opportunities to do things you haven't done or have not been able to do while at work. Build new social networks (mine comes from the community transport volunteering).

- Read everything about planning for retirement. Join the Association of Independent Retirees (AIR) a national not for profit organisation advocating for those funding their own retirements. Do your homework - life in retirement can be cheaper than working life. Investigate where you live and why - no point spending huge money on a house and not having enough to live comfortably. Stay healthy so you can enjoy retirement - being a healthy weight and basic fitness extends your life and your enjoyment. Travel is easier if you are fit and healthy. Don't plan to retire and play golf everyday unless you have a plan B - what if you can't play golf because of injury? Bad weather? Don't become a slave to your children and spend your retirement looking after grandchildren at the expense of keeping in contact with friends.

- Prepare financially to the best of your ability have confidence in your decision and know what simple things in life you enjoy and do them it’s your time do as you wish not others expectations.

- Unless super balance is very large try to continue part time work for a few years. This has advantaged me more than I realised at the time.

- Make sure you've paid off the house and can generate over $100k tax free income per annum and then enjoy!

- Plan ahead both in what lifestyle you want and how you will achieve it and fund it ongoing. Put money away for your travel aspirations.

- Retire at the same time as your partner.

- Do not think of retirement as just that short time between work and death. It can be a wonderful time of our life. We just need to re-invent ourselves. Our focus needs to be on mental and physical health, rather than career and building assets.

- Make a plan and potentially start an 'interest' that is viable in your senior years

- Plan for retirement a few years before, so that you have weighed out your options and make preparations. Finance is the area most covered but it is truly dependent on what you want to do with your time. Focus on family, health and spiritual areas.

- Life is too short, so do it while you have your health, sound mind. You can always find something to do. Even some trading if you have some spare disposable cash.

- Transition into it. Develop a hobby’s and interests before retiring

- Make sure your finances are good. Get out of debt as quickly as possible and start compounding your money.

- Take an interest in your Super (now!). If you do not have many interest outside work, start looking for some. If possible scale back work or start taking Long Service on half pay, short term retirement also has economic benefits.

- Unless you will work part time, develop some hobbies before you retire

- Experience things like overseas travel early before health issues arise.

- Take it as it comes. Be frugal, look for value in your spend. Remember there is still much to smile about.

- Salary sacrifice as much as possible. (The govt will assist as a low income person) Consider selling home and moving to suitable country location, then invest proceeds in a suitable fund.

- Use it, or lose it. A good life is the attitude you bring to it. Every day is in your control - good or bad. Stay fit doing some form of regular exercise, eat a balanced diet, stay involved and connected to friends, family or acquaintances. Try and learn something new each day, no matter how small. Manage what is in your sphere and don't fret or worry about what you can't control or change. Stay informed and involved with your financial position.

- Pre retirement, start doing or learning things of interest that can be expanded in retirement (musical instrument, bridge, crafts, etc)

- I’m mostly invested in index funds with some sector funds I think will generate alpha ( or at least very close to market returns in a worst case). I rarely buy individual shares unless i think I’ve found a no brainer- which the market doesn’t throw up very often and most often simply reinforces the lessons of why low cost index investing allows you to beat most professional active managers over long time frames, assuming they’re in business over a long time frame! I never sell because the market performs poorly. You can’t successfully get a job by blindly picking a company and not knowing anything about it or understanding it’s business. You can’t successfully pick a stock/ etf/ fund by blindly picking a company and not knowing anything about it or understanding it’s business.

- I think its obvious you need to get to the point where you don’t have to think about money then you can do anything.

- Plan carefully, because earning money does make a big difference to your psychological state ... feeling free to spend / give money ... make sure you have enough to satisfy your individual lifestyle. Pay off your debts before you stop earning. Diversify your assets.

- Work as long as you can while you are enjoying it. You are retired a long time and there is no going back.

- Try to be without debt or make arrangements to make it happen soon after. Learn to cook and clean the house. Be prepared to de-clutter. Get financial advice if needed. Start looking at the share market at least 10 years before retirement.

- Try and prepare by having a good think about what it is you would enjoy. develop other interests. make sure to take the opportunity to join and enjoy new company and friends.

- research and be prepared to take up new activities. Never played bridge before but now have played in comps overseas

- It won't be as glorious and you think but it will be better than being at work (usually).

- you job title is not who you are. enter the final quarter with a spirit of enquiry, stay fit and healthy in body, mind and soul and kick with the wind

- Approaching 50’s be ready things can change suddenly. Start realigning your personal wealth portfolio to ensure you have income generating assets. Cash flow is king.

- Keep active and involved in community and with family and friends.

- Keep as fit as you can, and remember that alcohol will pickle your brain and can encourage dementia.

- Manage life expectations well in advance of retirement so that the transition is seamless. Line up other things to do that don't cost money.

- Make sure you have the credit cards you want or similar as it becomes much harder to change banks when you are a self funded retiree even if your assets are in the millions.

- Plan ahead so that you have something active and stimulating to do - not just golf occasionally or walking the dog. If you just sit down in a chair (or at a holiday resort) and do nothing, you have set yourself on the downhill slope to losing muscle tone and mass, and losing brain sharpness, and consequently aging rapidly.

- Plan ahead. My retired brother-in-law has excellent advice. He says: "Keep trying new hobbies until you find ones you like." On a whim, I experimented making artworks out of beautiful, colourful fabrics. I've also taken some much admired photos and had them put on canvas. I found that creating things gives me satisfaction.

- Plan for retirement at least 10 years before to enable a comfortable lifestyle.

- The expectancy of life (in retirement) is a further 20 years of living. Health is a pressing concern, such as becoming overweight. The second essential is to have a plan for the ensuing 20 years.

- Go for it when you are ready as you don't know whats around the corner especially if you wish to travel or start new business venture

- As much as possible, have a realistic plan for what will fill your time with worthwhile activities (and not just golf). Keep active, both mentally and physically (as health does become problematic for many) and contribute your time to what you consider to be some worthwhile causes. Financially, get good advice and stick to it (thanks Morningstar) and don't focus too much on short term market movements or sweat the small stuff.

- Start planning finances and attitudes so you slip into a pattern of your choice, not uncontrolled circumstances you may find yourself in.

- Retirement is different for everyone, but think about how you will spend your day, and the next day and even for the next 20 years. Consider daily golf for twenty years.. Really?

- Try to transition gently so the change is not so abrupt. Consider a 3 or 4 day work week if that is possible. Have a plan for what you want to do in retirement and start to put it in place before you retire. Double check your financial position and if possible allocate more to retirement savings while you are still working. Start thinking about how it will be when you have no income from employment, and have to live off your savings only. That can be destabilising for some. Make sure you have realistic budgets and income expectations from your savings.

- Ensure your future income is sufficient. Invest in sustainable dividend producing shares. Get a dog.