I recently surveyed our portfolio and was stunned by the magnitude of the daily price moves. It was only 1.50pm yet APN Outdoor was up 4.32% on no announcement, TradeMe was down 2.77%, Healthscope was down 2.64% and Challenger down 1.92%.

Now, it is true that we don’t give two hoots about short-term movements. In the short run, price movements are largely random and will always be far more volatile than valuations. Prices can move on the back of sentiment and other factors that have little or nothing to do with the underlying business. A company’s valuation will change much more slowly, roughly in line with the growth in equity, from the retention of profits and redeployment of those profits at rates of return exceeding its cost of capital.

Unprecedented movements

Nevertheless, it seems that an unprecedented number of stocks have been hit with issues which have wiped significant amounts off their value, almost overnight. I cannot recall many other periods when a conga line was so populated with companies whose share prices have taken a 10-20% hit in a single day.

Recently, the announcements of the arrest of Crown Resorts executives in China caused its share price to fall almost 20% from $12.95 on 14 October 2016 to $10.40 12 days later.

Healthscope, the operator of 45 private hospitals, announced on 24 October that first quarter admissions for some procedures had slowed and that if the experience of the first quarter were repeated for the next three quarters, earnings would be flat for FY17. This caught the market, that was expecting 10% earnings growth, by surprise and the shares initially opened down 27%. As I write this, the shares are trading 24% lower than the closing price before the announcement.

Ardent Leisure’s shares have fallen by 25% following the Dreamworld tragedy, Blackmore’s shares are down 33% and Bega Cheese’s share price is 22% weaker. Unlike Woolworths, whose long-term competitive issues have resulted in a gradual weakening of its share price, the above examples have been rapid.

The questions on investors' minds are:

- Given examples where shares were ‘priced to perfection’, and the propensity for businesses to inevitably stumble or naturally endure weaker periods as part of the normal cycle, do these moves indicate a much deeper issue about market valuations overall?, and

- Are investors, who have been virtually frog marched into equities by rapidly diminishing returns from term deposits, overestimating returns and underestimating the risks of share market trading?, and

- Should the volatility be seen as ‘risk’ or as ‘opportunity’?

Volatility clusters

Volatility is still taught at school in the form of risk and portfolio construction, and dominates Wall Street thinking. However, our practical understanding of volatility has moved on somewhat from the days of Bachelier applying probability theory to French bonds, and the subsequent and elegant-but-flawed work of Eugene Fama’s Efficient Market Theory. Bachelier’s assumption that price changes are statistically independent and normally distributed is not borne out in the real world. The tails of the normal distribution curve fail to even remotely predict the frequency with which large price moves occur. Enter Benoit Mandlebrot, who observed that volatility tends to cluster around points in time, and after longer periods of lower volatility.

While roulette wheels spin by chance, over time the share prices of Blackmores, Woolworths or BHP don’t move by chance. But because prices can be described as if they move by chance, that has been how they’ve been described. As the aphorism goes, to a man with a hammer all problems look like a nail. And so odds and risks are being miscalculated.

The investor is best served by the work of Benjamin Graham, who without the benefit of a computer, observed that in the short run the market is a voting machine, but in the long run it is a weighing machine.

In the short run, prices will frequently move independently of the underlying business, but in the long run they cannot help but follow the accretion or diminution of the value of the underlying business.

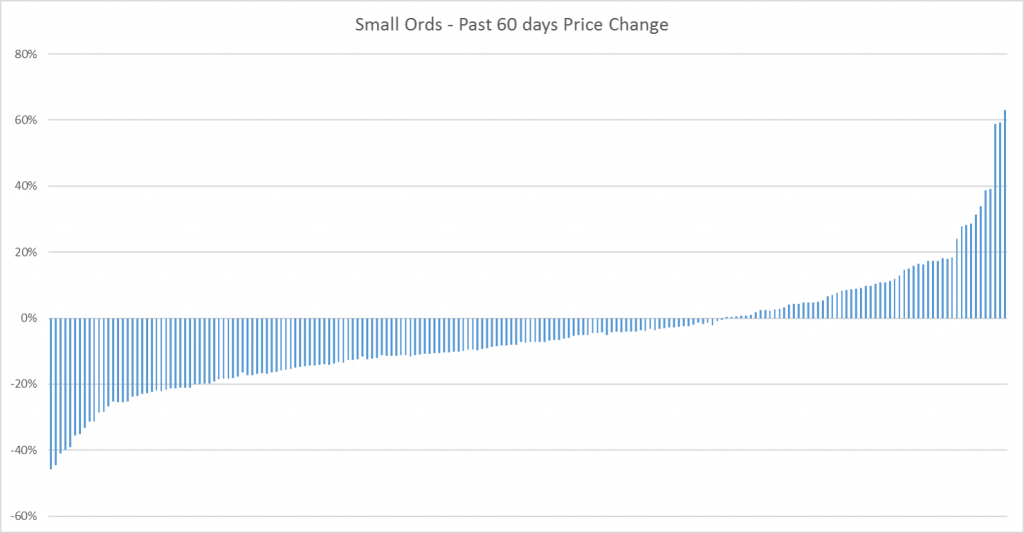

The following chart shows the movement, over the last 60 days, in the share prices of the companies that make up the Small Ords Index. There are some remarkable changes.

Source: ASX, The Montgomery Fund

Markets at high earnings multiples

In general, the frequency and magnitude of negative share price moves suggests a general overvaluation of markets. We know for example that the CAPE Shiller P/E ratio for the US S&P500 is at the 97th percentile at the moment – in other words, the earnings multiple has only been exceeded on 3% of occasions. Similarly, the P/E ratio for the Australian Materials index is at an all-time record as it is for the S&P/ASX200 index ex banks. This is to be expected when interest rates are at multi-century lows, however forecasts of a ‘new normal’ extended period of low interest rates is simply another version of ‘this time is different’, the four most dangerous words in investing.

Investors who own companies trading on high multiples need to be on their guard, especially those in large caps offering little or no growth thanks to high payout ratios (Telstra and the banks), challenged business models (Woolworths, Wesfarmers) or cyclical industries (it will take much less time for BHP and RIO to ramp up production if the price of iron ore rises again thanks to the mine development work having already been completed during the last boom).

Investors also need to be wary of the elevated prices of infrastructure stocks such as Transurban, Sydney Airports and Auckland International Airports. They are only justified by the application of the weighted average cost of capital calculation in valuing those businesses. Due in part to low interest rates and high levels of debt, the result is a high estimated valuation. But should interest rates rise, the justification for these valuations disappears, and the two listed airports are situated on a vacant block at the end of a global cul-de-sac, which hardly justifies them being the world’s two most expensive listed airports on an EV/EBITDA basis.

When market valuations are extreme, investors need to be wary of any stumble or miss in market expectations. Inevitably, it will be through this mechanism that extreme valuations are de-rated. In time, we will look back with surprise at the low rates of returns managers were committing their investors to for extended periods.

Ultimately, however, lower prices are a good thing. All investors should see themselves as net buyers over time. It is only through this lens that they will make wise decisions with respect to quality and value.

Net buyers want lower prices in the future. With that in mind, investors should always see heightened volatility as an opportunity, as long as the long-term economics and prospects for the business are bright. In the case of an operator of 45 hospitals with the ability to manufacture more hospital beds at one-third of the cost of the government, and in a market where the number of people over the ages of 65 and 85 are growing as a multiple of the population, we believe this is the case.

Roger Montgomery is the Founder and Chief Investment Officer of The Montgomery Fund, and author of the bestseller ‘Value.able’. This article is general information and does not consider the circumstances of any investor.