From 1 July 2019 new legislation provides an opportunity for recently retired individuals to contribute to super without needing to meet the work test. In this article we will review the work test requirements and the new exemption.

Contributions test varies by age

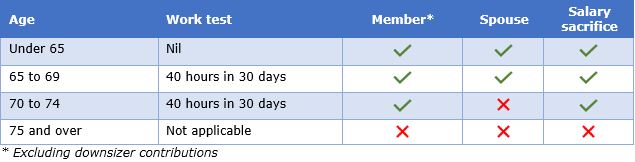

Individuals under age 65 are eligible to make voluntary contributions to super regardless of their employment status. However, after age 65, individuals must meet the work test. The following table outlines the different types of contributions and the age-related conditions that must be met:

The work test requires individuals to be gainfully employed for 40 hours in a 30 consecutive day period in the financial year in which the contribution is made.

Trustee acceptance of contribution

Super fund trustees cannot accept voluntary contributions from members over age 65 unless they meet the work test. The work test only needs to be met in the financial year in which the contribution is made. Accordingly, it is possible for the work test to be met after the contribution is made. However, some fund trustees require the member to be able to make the work test declaration at the time the contribution is made.

Gainfully employed definition

Gainfully employed is defined in super law as:

Employed or self-employed for gain or reward in any business, trade, profession, vocation, calling, occupation or employment.

The definition requires an expectation of income or profit in return for personal exertion. For an employed person this is generally easy to prove via a PAYG payment summary or income statement. Unfortunately many self-employment ventures do not result in financial gain, but the expectation needs to be there. An activity which is of a personal or hobby nature will not qualify even if there is financial gain.

Volunteering will also generally not qualify as there is no employer/employee relationship.

Work test exemption

The new work test exemption provides a one-time opportunity to make voluntary contributions in the year after retirement if the following contributor meets the following conditions at the time of contribution:

- Age 65 to 74

- Total super balance is less than $300,000 at the previous 30 June

- Met the work test in financial year prior to the year the contribution is made

- Not used work test exemption previously

- Contribution made after 1 July 2019

Once the work test exemption has been used for a financial year, it cannot be used again in a later financial year, however multiple contributions can be made within the financial year subject to the contributor’s age at the time of each contribution.

The new work test exemption provides an opportunity for individuals to make non-concessional contributions if they triggered the bring forward rule whilst they were under 65 but were not able to fully utilise the bring forward rule at that time.

Case study

Dawn was 64 on 1 July 2018 and she contributed $140,000 before her 65th birthday on 1 March 2019 when she permanently retired. Under the three year bring forward rules Dawn could contribute $160,000 by 30 June 2021 however she would need to meet the work test in the year she makes the contribution.

If Dawn’s total super balance is under $300,000 at 30 June 2019, she could contribute $160,000 in 2019/20 using the work test exemption.

Concessional contributions, including catch-up of unused concessional contributions cap amounts, could also be used.

Another area where the work test exemption will be valuable is for small business CGT contributions. For many small business owners, selling their business is their retirement plan and they often have small accumulated balances at retirement.

In many instances we see a great deal of effort put into the complex tax side of determining eligibility for the small business CGT concessions however sometimes the eligibility to contribute to super after age 65 is overlooked.

Case study

Arthur and Martha sell their small business at age 68 and 66 in July 2019 and embark on a round-the-world tour for the next 12 months. The proceeds from the sale of the business are received in August 2019 and arrangements made for small business CGT contributions and the appropriate forms to be made to their super fund in September 2019.

Under previous law, Arthur and Martha were not eligible to make the small business CGT contributions to super unless they met the work test in 2019/20.

However, if their total super balances are each under $300,000 at 30 June 2019, they may use the work test exemption to make their small business CGT contributions.

Superannuation guarantee contributions and downsizer contributions are not impacted by the new measure as they are not subject to a work test.

Julie Steed is Senior Technical Services Manager at Australian Executor Trustees. This article is in the nature of general information and does not consider the circumstances of any individual.