It’s 9am on a Saturday morning and a new apartment project is being launched somewhere in Sydney’s north. The queue started to form at the display suite hours earlier, and hundreds of anxious buyers crane their necks to see who is ahead of them and to watch for queue jumpers. The display includes a spectacular model of the building, while artist’s impressions on large posters show wide curved balconies overlooking gardens and parklands. The strong pre-launch marketing campaign to thousands on the real estate agent’s database and heavy advertising have built the enthusiasm into a frenzy. It’s a nervous wait, each person knowing they will have only a few minutes to decide whether to lay down a million dollars for a small two-bedder. Does it have the right aspect, is it high enough, how may car spaces? … what, a hundred have already sold in the first hour! I’ll take that one!!!

So much for the Reserve Bank’s recent warning of an oversupply of apartments, the inability of many Chinese buyers to settle on earlier purchases, the tightening of lending policies by banks. The Fear of Missing Out (FOMO) drives a market where the developer can name almost any price.

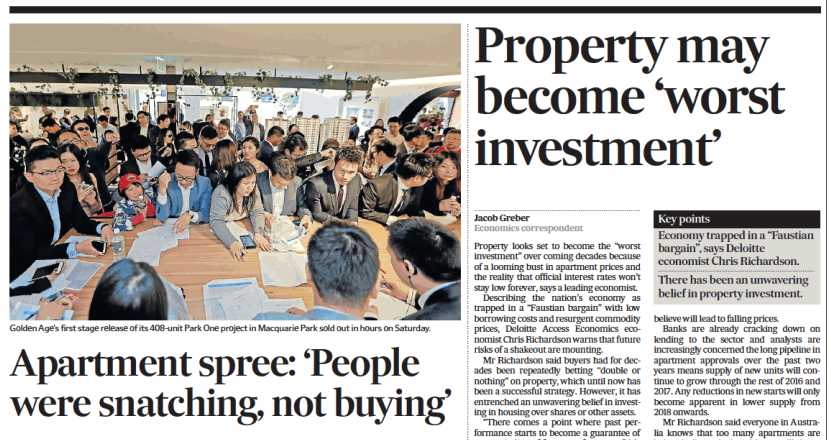

This week, The Australian Financial Review demonstrated the differences of opinion. On the same page where it reported 230 first-stage apartments sold out in a few frantic hours in one development, Deloitte Access Economics was forecasting the ‘Faustian bargain’ of declining prices and bad investments.

Source: The Australian Financial Review, 17 October 2016

My personal experience

In mid-2013, we bought an apartment off-the-plan for our daughter, and she moved into her new home at the end of 2015. This article draws from our experiences during the two-and-a-half years of construction and the subsequent months living there.

For those interested in a blow-by-blow description, we wrote a blog throughout the construction period, starting as the excavators first moved in, all the way to the landscaping. The blog has already received over 70,000 views as owners watched their dreams come to fruition.

The blog is attached here. It covers far more detail than most readers will want, with hundreds of photographs of the building, the anguish of delays, the dealings with the developer and the council and the amazing changes in the surrounding area of Pyrmont, Darling Harbour and The Bays Precinct.

This article does not enter the debate on whether it’s a good time to buy property or not. Rather, it focusses on the risks and rewards of buying an apartment off-the-plan.

Advantages of buying off-the-plan

The apartment was not bought for investment reasons. It was time for our daughter to move on from the family home, and we needed a particular location, size and design to meet her needs. Some of these comments are therefore not investment-related, although I expect they will have widespread applicability.

1. Enjoying watching the construction

We regularly visited the site as part of creating an historical record of how an old flour mill was being converted into a modern building of 135 apartments. The mill was originally built in 1896 and, after almost a century of operation, ceased production and fell into disrepair. Only three sides of the old façade remained, held up by steel beams, in a prominent location near the gateway to Sydney heading to the west.

We loved the design, the way the new building ‘stepped over’ the old, retaining part of Sydney’s industrial heritage in an otherwise modern structure, as shown below.

The building stands at the top of an escarpment at the edge of Pyrmont/Ultimo, at the end of a narrow road of heritage terraces. It took months to dig four floors of basement parking out of solid sandstone, and then as the building grew, the mill façade had to be ‘tied’ to the new structure while hoping the old walls did not fall into the massive hole.

This process of photographing the site, communicating with other owners on the blog, watching the surrounding area change and eventually moving in, was an unexpected pleasure. It created a special bond with the building, knowing so much about how it had been created.

2. It’s the way to buy a new apartment

For anyone who wants a new apartment, buying off-the-plan is almost the only option. It is possible to wait for a building to be completed and see if some buyers sell or renege around settlement time, but unless there is a major fallout, a minority of apartments come onto the market at this time, greatly limiting the choice. It’s unlikely that the pick in the building – the quiet side, the private outlook overlooking the garden, the best view or the location away from the pool and lifts – will suddenly appear. These good apartments need to be grabbed early off-the-plan.

3. It may be possible to make some design changes

We had some specific design requirements, and fortunately the developer accepted with considerable grace our desires to change the internal layout of the apartment. We switched the two bathrooms, redesigned the kitchen and a bathroom, removed a wall from one of the bedrooms and relocated electric switches. No doubt this was an exceptional experience, although more common in top-end apartments. It would have been extremely difficult or expensive to make such extensive changes in an established building, but done early enough in the design and build stage, it was not costly to accommodate. It made the end result a bespoke design instead of the inevitable compromise of an established apartment.

4. Ability to plan the funding of the balance

The 10% deposit allows long-range planning on the funding of the balance. There is no rushing around for finance or a quick sale of assets. Of course, any gains in price for an investor are leveraged by the 100% exposure to the market, the type of gearing not available on other asset classes. This is a double-edged sword, and it is far more likely that prices will fall from this point forwards than it was in June 2013. Even when we were buying, we could feel the early stages of a price surge, although nothing of the coming Sydney stampede. Some apartments in this building were sold prior to settlement for handsome returns.

Disadvantages of buying off-the-plan

Many financial planners advise their clients never to buy off-the-plan due to the uncertainties and inflated costs involved, and anyone going through this method of buying should consider the risks. Over 200,000 apartments are expected to come onto the Sydney, Melbourne and Brisbane markets by 2018, raising questions about where the demand will come from.

The two main problems experienced in our building were:

1. Uncertainty when it would be completed

When we bought the apartment in June 2013, we were told it would be completed by the end of 2014. The date gradually moved out quarter by quarter until it was a year late. This was not too difficult to manage since our daughter simply stayed with us longer, but it introduces great uncertainty for anyone renting or needing to sell. How long do they rollover their existing lease? When do they put their property on the market? These problems would not occur with an existing property.

You can see in the blog the progress of the building. We visited the site nearly every month, and we asked workers about progress and towards the end, completion dates. The dates gradually slipped by, not due to a dramatic event like flooding or bad weather, but more because of its tight access in an inner city location. The building ‘topped out’ in August 2014 but it wasn't completed for another 16 months.

Many buyers became worried about the ‘sunset clauses’ in our contracts. There were news stories about developers rescinding contracts once certain dates had passed, leaving owners without their apartments and developers with massive windfall gains as they resold to new buyers. We settled three months before our sunset clause, and the NSW Government changed the law in November 2015 to prevent this unscrupulous practice.

2. Different product than the one promised

The overall building design delivered significantly as expected, and in fact, the quality of design and finish are probably better. As we were closely involved in the ongoing design of the apartment, there were no surprises.

But other owners had significant issues, such as layouts not as originally specified, walls where windows with views were expected, and some apartments were smaller than the original design. The contract gave the developer the right to deliver an apartment with a size variation of up to 5%, which on a 120 square metre apartment is a significant six square metres. Of course, there have been complaints about fixtures and fittings not being as expected and while these have generally been resolved, there is none of this doubt when buying an existing place.

Some of the surrounding infrastructure, such as the public lift from the property directly to the light rail station, was not completed for another six months, as the council refused to certify it until some issues were fixed. Lend Lease’s construction work in Darling Harbour also compromised access to the city for far longer than was originally advised.

The following disadvantages apply more generally rather than in our case.

3. Potential victims of clever marketing

There is a pleasure and excitement in owning real estate that few other investments can match. On the investment side, the marketing highlights negative gearing benefits, capital gains discounts, rental returns. It rarely quotes the correct strata fees as nobody knows what the body corporate will set. Other costs such as council levies, stamp duties and maintenance costs are ignored in the colourful brochure. Instead, the focus is on the shiny new building, the landscaped gardens, the convenient location and the amazing facilities. Many new apartments cost more than established dwellings nearby, where the seller does not have the marketing gloss.

An owner occupier may not be overly concerned at paying 5-10% more to move into a new apartment, but an investor may see lower returns, and anyone planning to sell before settlement will need a strong market to recover the stamp duty and legal costs. The impending supply in eastern capital cities suggests the price performance of recent years will not be repeated.

4. Inability to obtain finance and leveraged losses

While most people buy an apartment with a financing plan, the actual visit to the bank or broker usually occurs as settlement approaches, which may be a couple of years after the original commitment. It is not possible to know the willingness of banks to lend in a particular suburb or on a type of property. The bank will engage a valuer to assess the property value, usually lending around 80% in the current market (this loan-to-valuation ratio has fallen due to worries about future prices). The value is not what the buyer paid, but what the bank could realise on a sale less costs. For example, a property costing $1 million may be valued at $900,000 nearing settlement, and the maximum loan may only be $720,000. The $180,000 (in addition to the initial $100,000 deposit) is a lot to find for someone who was expecting the bank to lend the full $900,000, and the risk of non-settlement rises. The buyer may face a loss of the deposit, or more if the developer takes legal action.

A valuation firm, WBP Property Group, conducted research on 1,794 off-the-plan sales in Victoria between December 2009 and August 2015 and found half the properties were valued at less than the original purchase prices, with the average loss of $40,000 or 9.4%.

Conclusion

Our experience buying off-the-plan had its highs and lows. We enjoyed writing the blog and watching the building rise from the sandstone, and we now have a unique record of the transformation of part of Sydney’s industrial history. The end product for us has lived up to expectations after we stayed actively involved with the developer. The construction delays were annoying, and I can certainly see the advantages of buying a finished product which gives greater certainty of the outcome.

Graham Hand is Editor of Cuffelinks. Every experience buying a property will be different, and I have deliberately not entered the debate about whether it's appropriate to buy a property for your children, even if you can.

Shane Oliver of AMP Capital has written this research paper on the outlook for Australian housing.