There’s a lingering statistic across Australia’s legion of 600,000 self-managed superannuation funds.

Collectively, SMSFs have about $890 billion invested into different assets on behalf of roughly 1.1 million people, according to the most recent Australian Tax Office (ATO) quarterly data.

But a more interesting number to look out for in the ATO data is the total amount that SMSFs still have allocated to low-yielding cash and term deposits.

Over the last decade it’s been hovering around the $140 billion mark, at times surpassing 20% of total SMSF assets under management.

The pros and cons of cash

Why many SMSF trustees choose to hold large amounts of cash is understandable, to an extent.

There is a common misconception that cash is a risk-free asset. It’s not prone to daily market volatility like shares are. It’s also liquid – you can generally get your hands on it quickly and easily.

Furthermore, cash savings up to $250,000 per account holder (including SMSF trustees) on deposit with an Australian authorised deposit-taking institution are guaranteed by the Commonwealth in the event the institution fails.

For self-funded retirees using an SMSF, holding cash enables quick withdrawals to fund everyday life in retirement.

Yet, cash does have inherent investment risks. Firstly, a decade of record-low interest rates has meant that cash as an asset class has delivered an average annualised income return of just 1.9% since 2012.

That’s lower than any other major asset class. Worse still, after taking high inflation levels into account, real cash returns have been negative for some time.

Bond inflows on the rise

What’s startling in the ATO’s latest SMSF asset allocation statistics is the low amount of money trustees have invested directly in fixed income debt securities (namely investment grade bonds).

It’s only about $10.5 billion in total, less than one-tenth of the amount invested in cash.

While the actual number is probably somewhat higher, considering that it is likely some SMSFs have invested in bonds indirectly via bond exchange-traded funds (ETFs), unlisted bond funds, and diversified funds that hold both equities and bonds, it is still surprisingly low given the superior risk-adjusted returns potentially available from fixed income.

Bonds are securities issued by governments or companies that they use to borrow money, and the investor buying the bond can expect to receive full repayment of their principal if they hold it until maturity as well as steady regular interest payments until then.

As such, bonds are considered a lower-risk type of investment than shares which can’t offer any expectations to investors of either full repayment or a steady income stream and which are usually more prone to market volatility.

Likewise, being slightly higher risk than cash, bonds are generally expected to outperform cash over the long term.

What’s clear is that a growing number of investors worldwide are liquidating their cash in order to take advantage of higher-returning, relatively low-risk, high-grade bonds, especially government-issued bonds.

That’s showing up in a range of other data, including statistics from the Australian Securities Exchange (ASX) covering monthly inflows into ASX-listed ETFs that invest in Australian and international bond issues.

In the latter half of 2022 investment inflows into bond ETFs ($2.2 billion) exceeded the inflows into Australian shares ETFs ($1.6 billion) – that’s rare.

What’s behind the heavy bond inflows?

There are three major factors underway that have led to the increased, and accelerating, inflows into bond products around the world.

1. Higher interest rates

To counter surging inflation, central banks around the world have rapidly increased official interest rates to quell consumer demand.

As official interest rates rise, so do the yields available to bond investors on new and existing bond issues. That obviously makes bonds more attractive to investors seeking higher steady income streams.

The higher income payments now available from bonds are expected over time to partially (if not fully) offset the bond price declines that occurred in 2022.

In 2023, Vanguard’s return expectations for fixed income have significantly increased compared to a year ago.

We forecast global bonds to return 3.9-4.9 per cent and domestic bonds to return 3.7-4.7 per cent over the next decade – a 2 percentage point increase on the 10-year forecasts we made a year ago.

The prospect of higher returns underscores the increased demand for fixed income from investors, and this demand is only expected to grow over the short-to-medium term.

2. Higher capital growth

Bond prices typically move inversely to interest rates, which means that as bond yields have increased, bond prices have fallen.

That’s made bonds cheaper to buy on the market than when yields were at ultra-low levels.

Bond investors can expect this to change over time, because once inflation levels fall it’s likely that central banks will start to reduce official interest rates.

For bondholders (whether they hold bonds directly or indirectly), lower interest rates will likely ultimately translate to higher bond trading prices, which will likely result in capital appreciation on their investment over time.

This is another key attraction for fixed income investors with a longer-term horizon.

3. Improved portfolio diversification

Lastly, it’s important to look at the traditional role of bonds in investment portfolios, which is to provide asset class diversification to help smooth out total investment returns over time.

There are strong diversification benefits to investors who hold both shares and bonds in their portfolios over longer periods.

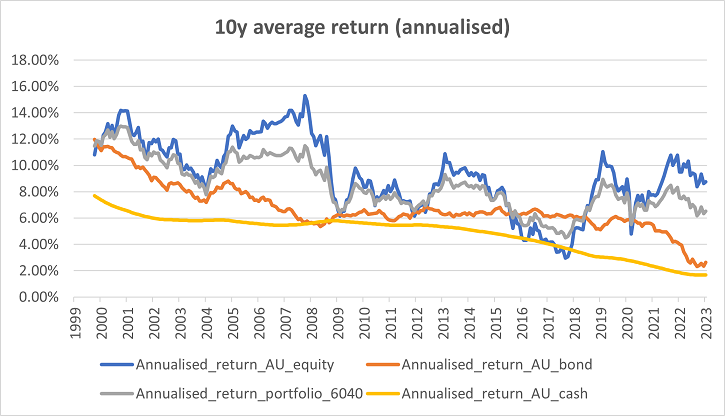

For example, Vanguard analysis shows the average annualised return from a 60/40 portfolio split between Australian equities and bonds over a 23-year period from 2000 to 2023 has been only slightly lower (around 1%), and with notably lower volatility, than an all-Australian equities portfolio.

Meanwhile, fixed income has consistently outperformed cash.

Source: Vanguard

While bonds do not outperform riskier asset classes such as shares over the long run, they typically have a more stable return profile because they are not prone to the same level of market volatility.

You can see this by comparing the orange line in the chart above (fixed income) to the blue line (equities).

Historical returns across a 23-year period show that bonds can deliver income, capital returns and diversification benefits at a manageable cost to total portfolio returns.

This underscores the worth of well-balanced portfolios, no matter the market conditions.

The key takeaway for investors from this data is that sticking with a diversified asset allocation covering fixed income and equities is a sound long-term investment strategy.

So, expect to see more portfolio rebalancing as investors capitalise on higher interest rates, lower bond prices, and the potential price upside from share markets.

This may see a reduction in the high amount of cash currently being held by SMSF trustees operating through a trust deed that authorises investments in bonds.

Jean Bauler is Head of Fixed Income at Vanguard Asia-Pacific, a sponsor of Firstlinks. This article is for general information purposes only. Vanguard has not taken your objectives, financial situation or needs into account when preparing this article so it may not be applicable to the particular situation you are considering.

For more articles and papers from Vanguard Investments Australia, please click here.