Recent political events point to an increased likelihood of a Labor Party election victory in 2019, making the implementation of its proposed changes to franking credits more likely. Much has been written on this change including its impact on SMSF pensioners, its unfairness, its potential impact on equity markets and the perception that an underlying motive is to move people out of SMSFs and into industry funds.

However, in all the heated discussion, one key advantage of SMSFs has been largely overlooked: control. Some SMSF trustees will still be able to exploit this feature of SMSFs to minimise or remove the financial impact of the franking change while at the same time undertaking strategic estate planning, the fruits of which they will enjoy while still alive.

The benefit of control

Most people set up SMSFs because they want to exercise control over key aspects of the fund including its membership, investments, timing of investment sales to maximise tax outcomes, general administration and estate planning. Our students at the University of NSW are taught this early in our SMSF course to demonstrate people are taking responsibility for their retirement.

However, the current franking discourse has lost sight of this major SMSF benefit. This article expands the discussion on one strategy available to SMSF trustees (mentioned in Matthew Collins’ article in Cuffelinks).

Adding adult children in accumulation mode to an SMSF in pension mode

The addition to an SMSF of younger family members who are still in accumulation mode and making taxable superannuation contributions will lead to an increase in the fund’s taxable income. The SMSF is a single taxable entity. Trustees can utilise the combined taxable income of both the pension and accumulation components. This can soak up some, if not all, of the franking credits otherwise lost from 1 July 2019 under Labor’s proposal.

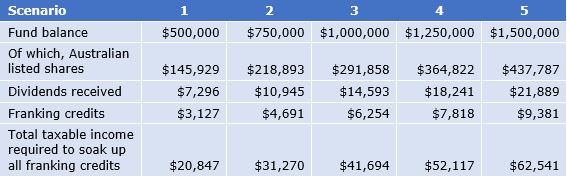

The table below sets out the potential franking credits lost assuming a two-member SMSF in full pension phase, a dividend yield of 5% and an asset allocation of 29.2% to listed Australian shares as per the latest ATO statistics (assume these shares are fully-franked dividend paying).

This stylised example shows the taxable income required to fully utilise all franking credits.

Where does the taxable income come from?

The increase would come from concessional contributions made by adult children added to the SMSF along with investment earnings on any existing accumulation balance rolled over. Given adult children in their 40s have been receiving superannuation contributions for 25 years (since 1992 albeit at lower rates than the current rate) the balances rolled into the SMSF may be significant. The full amount of the concessional contribution is classified as assessable income to the SMSF.

Assuming one child joins the SMSF and rolls over an existing balance of $150,000 and makes maximum annual concessional contributions of $25,000, the SMSF’s taxable income would increase by $32,500 ($25,000 + [$150,000 x 5%]). This would result in all franking credits being used in scenarios 1 and 2 above. Based on investment earnings of 5%, every additional $50,000 of accumulation funds rolled into the SMSF would increase taxable income by $2,500. Compounded over a decade or two (a feasible result given current longevity expectations), the financial result is material.

The outcome becomes more favourable if two or more children join the fund (up to four children could join the fund if the current proposal to increase the limit of SMSF members from four to six commences in 2019). While ATO statistics point to a slight fall in four- and three-member SMSFs in recent years, the increased scope for strategic planning emanating from the proposed change may reverse this trend.

Benefits of the strategy

The addition of children to an SMSF who are still in accumulation mode can be an effective strategy for several reasons:

First, existing SMSF pension members will not want to ‘lose’ money after 1 July 2019, and increasing the fund’s taxable income partially or fully retains the benefit of franking. In effect, the SMSF is achieving the same result as an industry or retail fund which will not lose the ability to use franking credits.

Second, by utilising their parent’s franking credits, children can tax-efficiently increase their retirement savings. This could occur at a time when they are dealing with significant financial commitments like mortgages and school fees thus providing a welcome financial boost.

Third, and perhaps the most overlooked reason, is that the proposed change provides an opportunity for SMSF pensioners to implement an estate planning strategy that takes effect while they are still alive. Effectively, SMSF pensioners will be able to legally and tax-efficiently pass on some of their estate to their children by reducing the tax liability on their children’s super contributions and earnings. Again, the compounding effect over many years may be significant. Furthermore, rather than the usual scenario of their estate being transferred to their beneficiaries after their death, parents will be able to enjoy their retirement years in the knowledge that their children are simultaneously reaping the benefit of their SMSF structure instead of losing some of their retirement benefit to a legislative change.

Potential drawbacks of the strategy

Of course, all strategies come with risks and potential problems.

First, in return for joining the SMSF, children would have to take on the associated trustee responsibilities, although this may lead to greater engagement with their superannuation.

Second, family life can be complex. Marriage breakdowns, estranged children or family in-fighting are common and may prove too much of an impediment to this strategy. No doubt, some people will understandably not want to go anywhere near mixing finances with family life.

Third is the issue of fairness. More of the benefit of franking credits otherwise forfeited would accrue to the children with greater existing accumulation balances or making larger concessional contributions because the franking credits are applied proportionately (i.e. they save the greatest amount of tax). However, this could encourage children to make greater contributions.

Fourth, a risk for children joining the SMSF is that investment returns may be less than those earned in their existing retail or industry fund, or they may sacrifice favourable insurance arrangements.

Such impediments are not insurmountable and may even be a catalyst to ‘professionalise’ the SMSF and take a more holistic, whole-of-family approach, to financial planning. Against the backdrop of the ongoing Royal Commission and other changes occurring in the financial advice industry, Labor’s proposed change represents an opportunity for SMSF trustees and their advisers to consider a more forward-thinking approach. Of course, the policy proposal is facing considerable public opposition, and its final form or timing are unknown at this stage.

Dr Rodney Brown is a Lecturer in Taxation and Business Law at the University of NSW Business School, including the Master of Tax and Financial Planning course. He completed his PhD at the London School of Economics after working as a financial planner in Sydney. This article is general information based on a current understanding of tax law and Labor’s proposal, and it does not consider the circumstances of any individual.