The powerful shift in recent decades toward indexing and other forms of passive investing has taken place for the simple reason that active investment decisions are so often wrong. Of course, many forms of error contribute to this reality. Whatever the reason, however, we have to conclude that, on average, active professional investors held more of the things that did less well and less of the things that outperformed, and/or that they bought too much at elevated prices and sold too much at depressed prices. Passive investing hasn’t grown to cover the majority of U.S. equity mutual fund capital because passive results have been so good; I think it’s because active management has been so bad.

Howard Marks, memo to clients ‘Selling out’, January 2022

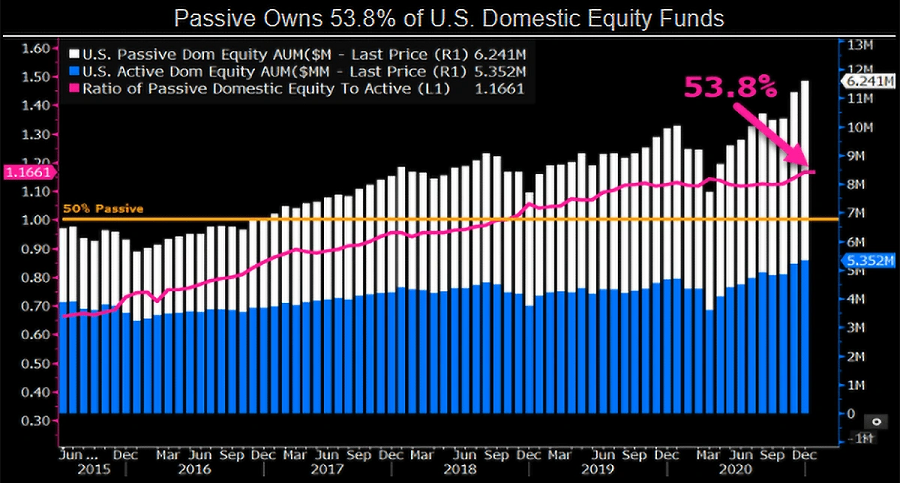

It’s commonly-accepted wisdom that the majority of active equity managers struggle to beat their benchmark after fees. The loss of confidence in the ability of many fund managers to justify their fees is so strong in the world’s largest market that, according to Bloomberg in the chart below, passive funds comprise about 54% of the US domestic equity funds.

Source: Bloomberg Intelligence

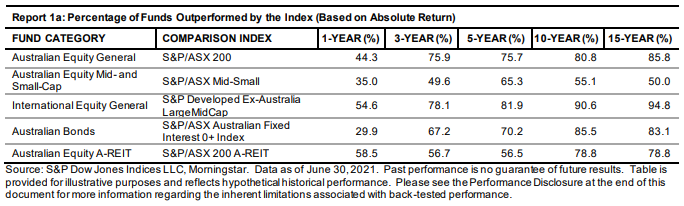

In the Australian market, the active performance data is not flattering, as shown in the table below. Standard & Poor’s Index Versus Active (SPIVA) Australia Scorecard reports on the three main equity fund categories:

Australian Equity General Funds: Over the 5- and 10-year horizons, 76% and 81% of funds failed to beat the benchmark, respectively.

Australian Equity Mid- and Small-Cap Funds: Over the 5- and 10-year periods, 65% and 55% of funds underperformed the benchmark, respectively.

International Equity General Funds: Over the 5- and 10-year periods, more than 82% and 91% of funds underperformed the S&P Developed Ex-Australia Large-Mid-Cap, respectively.

The number in the table is the % of funds outperformed by the index. Over long terms such as 15 years, large cap managers do poorly, with 85% to 95% of funds failing to match their index. Smaller- and mid-cap managers hold their own at around 50%.

There are some active managers who consistently deliver results, but the argument for an allocation to passive management is strong, at least as part of a core/satellite approach. That is, investors may choose to hold index or passive funds for a core position to save costs and participate fully in the market, but select active managers with strong performance who the investor regards highly.

What about the ‘outperform in down markets’ argument?

Many active managers acknowledge underperformance in strong markets but argue they are protecting capital by not backing the big (and now expensive) winners. An active manager may underperform simply by missing a big mover such as Afterpay in Australia or Tesla in the US, but who can blame them for avoiding such overprices stocks? They say they will more than compensate for lost relative returns when the market goes through a slower or weak period.

It’s a narrative which works sometimes but often not. In the US (and soon to come to Australia), Morningstar publishes a semi-annual ‘Active/Passive Barometer’, and in March 2021, a paper studied the results from the 2020 selloff due to COVID-19. The report concluded:

“The coronavirus sell-off and subsequent rebound tested the narrative that active funds are generally better able to navigate market volatility than their index peers. As we documented in our midyear 2020 report, active funds’ performance through the first half of the year showed that there’s little merit to this notion. Across all 20 categories we examined, 51% of active funds both survived and outperformed their average index peer during the first half of the year. The full-year result for active funds wasn’t much different. In 2020, just 49% of the nearly 3,500 active funds included in our analysis survived and outperformed their average passive counterpart.”

It's not encouraging for those investors looking to their active manager to recover performance when the market tanks.

When the case for active management is stronger

The rapid growth of index funds in Australia, most notable in the success of passive Exchange Traded Funds (ETFs), shows Australians have embraced the same investment philosophies as US investors, although far less as a proportion. In Australia, unlisted managed funds are still dominant.

However, there are some circumstances where index investing may carry unacceptable risks.

1. When the index is overweight in certain sectors

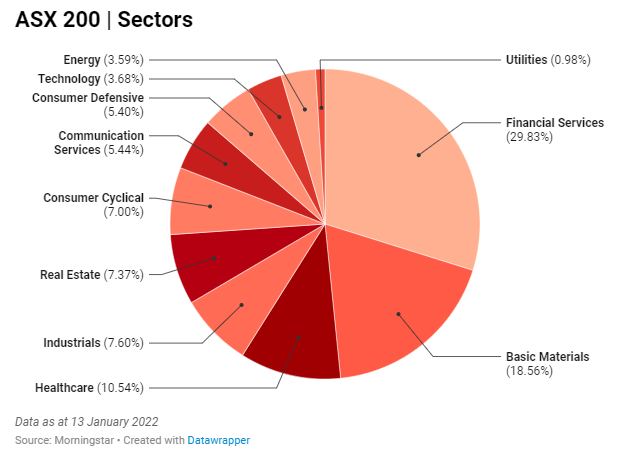

The Australian stockmarket comprises 11 main sectors, often based on the Global Industry Classification Standard, or GICS. To add to the confusion, there are also 24 Industry Groups and 68 Industries, so the terminology of 'sectors' and 'industries' in sometimes unclear.

While most investors believe buying an index exposure to, say, the ASX200 gives a diversified investment in 200 companies, it is heavily concentrated in the sectors of Financial Services (30%) and Basic Materials (18.5%). After BHP switches its dual listing to a single Australian listing, these two sectors will be over half the ASX200 exposure. That’s a lot riding on highly-leveraged banks and miners exposed to China and iron ore, as shown below. Technology is a modest 3.7%.

This lack of sector diversity shows why the days of home bias in Australian share portfolios should be long gone.

Sector concentration weighs heavily on the underperformance on the ASX versus other global markets. Financial Services is itself dominated by five banks and the sector has underperformed the broader market. In calendar 2021, the Australian market rose 18.6% but the tech-heavy US S&P500 was up 28.7%.

The rapid growth of ETFs facilitates investment in a wide range of themes and sectors. But investors should watch the composition of some of these ETFs by visiting the websites of the ETF providers and checking the weightings in the funds. Even in the large US market, Apple and Microsoft together comprise one-third of the Morningstar Technology and Communications Index.

There are thousands of indexes around the world, and many of them are not based on 'cap-weighted', or the market value of the company. One way to manage the concentration risk with the cost benefits of an index is to invest in a fund where stock selection is tied to another type of index. Some indexes do not automatically drive up a greater allocation to a company as its share price rises, as happens with a cap-weighted index. Examples include 'equal-weighted' or 'fundamental' indexes, both of which are available on Australian ETFs.

For example, VanEck (a sponsor of Firstlinks) says:

"The VanEck Australian Equal Weight ETF (MVW) equally weights the largest and most liquid stocks on the ASX. It is underweight the mega-cap resources and big banks relative to the S&P/ASX 200 Index. As at 30 November 2021, MVW’s portfolio is underweight financials by 12.58%, mega-caps by 18.47% and overweight large-cap (+12.07) and mid-cap (+6.62%) stocks."

2. When the index is overweight in certain stocks

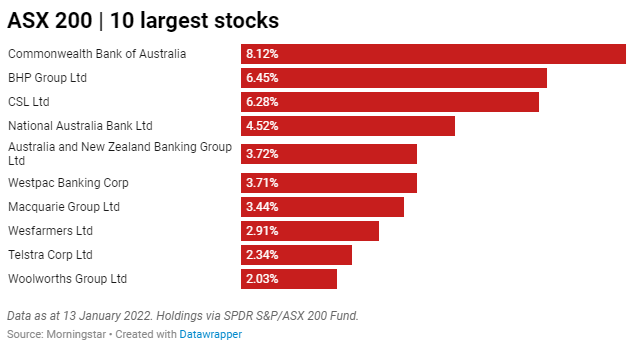

Along a similar path, Australia’s index is increasingly dominated by large companies, especially after stocks such as Sydney Airport and AusNet delist when bought by private equity or major funds. As shown below, 10 Australian companies each comprise over 2% of the ASX200, a total weighting of 44%.

In the next two weeks, BHP will become Australia’s largest company as it unifies its corporate structure with a single primary listing on the ASX. Morgan Stanley estimates its weight in the index will rise by about 4% above the level shown in the table below. ETFs tracking the index will become not only more concentrated in resources but one company will command over 10%.

Such index changes result in major buying and selling in Australia to rebalance. Morgan Stanley estimates local index funds will need to acquire $3.6 billion of BHP shares. However, there will be selling in the UK as their index funds no longer need to hold BHP. Other companies in Australia will be sold as their weighting falls, so the net new money into the market will be modest. The target date for completing the BHP change is the end of January.

Index funds are already preparing for BHP's big increase, with some buying in the UK where BHP trades at a discount to the Australian price (mainly due to the value of franking credits in Australia, but also recognising better liquidity). Vanguard has advised investors in the Vanguard Australian Shares High Yield ETF - which tracks the FTSE Australia High Dividend Yield Index - that:

"This index applies a 10% maximum weighting to any one company when the index is rebalanced semi-annually. To maintain these diversification requirements, a 10% cap will be applied to BHP based on the closing price on 21 January 2022. On the effective date, Vanguard fund weightings in BHP may be over 10% due to market movements.”

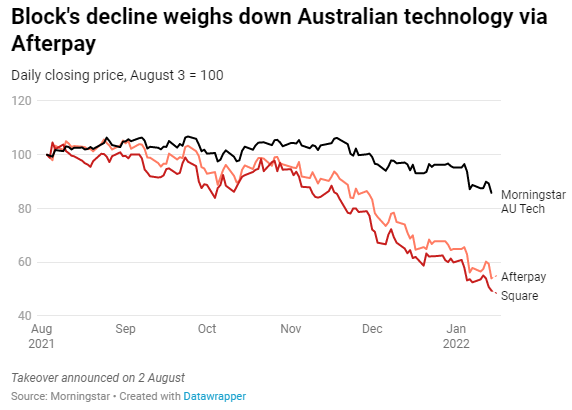

The influence of a single company, Afterpay, has significantly dragged down the Morningstar Australia Technology Index in 2022 year-to-date. APT represents one-third of the tech index and has fallen by about 50% since August 2021, when it was acquired by Block (previously Square), as shown below. The index has also not been helped by a fall from favour of stocks such as Nuix and Appen.

3. When the index holds illiquid assets

A highlight of recent developments with ETFs is the wide range of sectors, asset classes and specific themes now available. Investors can back their judgement on dozens of categories such as commodities, AI, robotics, crypto, EVs, cloud computing, clean energy and video games, all listed in Australia.

There is also better availability of fixed and floating rate funds, bringing income choices previously available only to wholesale and institutional investors. These include government debt, corporate debt, hybrids and floating rate notes.

This variety raises questions about the liquidity in difficult market conditions. On the plus side, an ETF based on Australian or global large companies should deliver good liquidity in all markets because the underlying investments themselves are liquid. An ETF or any index fund is simply a vehicle for holding assets, and if investors want to redeem, the fund manager (or market maker) sells the underlying shares or bonds to pay the withdrawal. Even in tough markets, the trading price spread of large companies usually remains firm.

However, Morningstar research around March 2020 during the peak of the virus showed some fixed interest ETFs faced spread costs of about 3%. With low interest rates, that is equivalent of more than a year of interest payments.

One advantage that Listed Investment Companies (LICs) and Listed Investment Trusts (LITs) hold over ETFs is the commitment of capital. The manager does not sell to meet redemptions, as liquidity is provided by buyers in the market. However, it's a double-edged sword as prices can move to a discount if there are few buyers, but at least the manager is not forced to liquidate. For this reason, some asset classes, such as non-investment grade bonds and private debt, are better in LIC/LIT structures than ETFs.

And that's the way the market has developed. With a few exceptions, the bond and note ETFs in Australia are predominantly government or investment grade, with a couple of hybrid Active ETFs which rely on the liquidity of hybrids.

A comment on the ease of selling and overtrading

Behavioural risk can be costly for investors who cut and run at the first sign of market weakness.

One of the benefits of ETFs is the ease of access. Anyone with a broker account can buy ETFs like any other share. But there are disadvantages in making buying and particularly selling so easy. Many people overtrade and would do better to buy and hold rather than try to time the market by jumping in and out. Ironically, there are benefits in some selling 'friction'.

In her book, “Good Habits, Bad Habits: The Science of Making Positive Changes That Stick”, Wendy Wood, a Professor of Psychology and Business at the University of Southern California, writes:

“Your behaviour is much more controlled by what’s easy in your environment than most of us think ... One of the really nice things about adding friction to a behavior is that it encourages you to do something else.”

To block bad habits, she says we need to add friction or restraints that turn easy, automatic behaviors into actions that require effort.

Check what’s in that index

As the Australian stockmarket becomes more concentrated in a few big names, and as ETF issuers move away from liquid markets into specialised sectors, it is increasingly necessary to check what is in an index. The word 'index' does not refer only to broadly-based market indexes, as there are thousands of them (Morningstar alone has 1,330 indexes). Investors should not simply buy an index fund and assume it is diversified.

Graham Hand is Managing Editor of Firstlinks. This article is general information and does not consider the circumstances of any investor.