As we review the daily headlines chronicling the tug-of-war between inflation and interest rates, we are reminded what a difficult job macroeconomic investors have and how grateful we are to be fundamental investors.

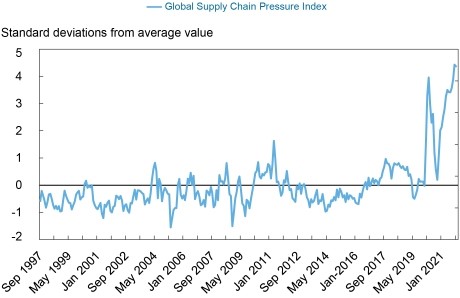

As challenging as it was to predict Covid-19, it would have required truly profound foresight to conceive that a supply chain crisis would rank amongst the most impactful financial consequences of the world’s first pandemic in modern history. And yet, as of this writing, the supply chain situation and its resulting inflationary implications have captured investors’ and policymakers’ attention to the degree that the New York Federal Reserve has recently created a new Global Supply Chain Pressure Index (GSCPI) to help track the health the global system.

While the underlying cause of this newfound supply chain focus is unfortunate, we believe the increased attention will be positive in the long run for both the companies innovating within the supply chain space and consumers globally.

Since before the outbreak of Covid-19, our Global Growth team has been analysing and investing in companies working to increase supply chain efficiencies. In this article, we take the opportunity to review two companies that we see as well-positioned to support a more efficient and robust global supply chain to the benefit of all stakeholders.

Sources: New York Federal Reserve Bank, Bureau of Labor Statistics; Harper Petersen Holding GmbH; Baltic Exchange; IHS Markit; Institute for Supply Management; Haver Analytics; Bloomberg L.P.; authors’ calculations. Note: Index scaled by its standard deviation.

Note: The information provided should not be considered a recommendation to purchase or sell any particular security.

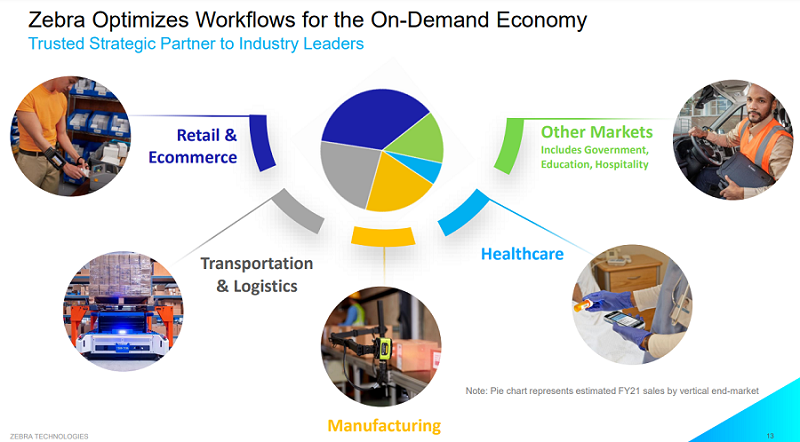

Zebra Technologies Corp – Omnichannel automation and integration for retailers

Zebra Technologies Corp (Zebra) designs, manufactures and sells automatic identification and data capture products. Its barcode printers and scanners help companies manage their inventories and assets investment more accurately and efficiently.

Zebra’s products and solutions facilitate the digitisation of a company’s physical workflows so that they can be more effectively implemented, tracked, and analysed in real-time. For example, Zebra’s RFID solutions enhance warehouse managers’ capacity to audit and record incoming and outgoing freight, by enabling significantly faster throughput and reduced error rates. Pairing these RFID capabilities with Zebra’s barcode scanning technology allows for real-time, point-to-point freight tracking throughout the world, which enhances resource planning and customer response. These scanners and data analysis capabilities allow retailers to accept returns and reintegrate merchandise back into existing inventory.

The company is one of the leaders in its market. Its research spending is nearly twice that of its nearest competitor, helping to maintain its market position. Zebra has reduced its debt and now has the capacity to pursue acquisitions and or share repurchases. Profitability metrics have also improved in recent years.

Zebra is experiencing robust growth, due to both recent acquisitions and several underlying secular trends. Companies are increasingly investing in scanners and other equipment to compete with Amazon's fulfillment speed and customer service. Retailers are also investing more in omnichannel sales, and Zebra's products help keep track of inventory and route sales to customers through the most convenient location. Other areas such as health care are underpenetrated but growing markets for data capture and analysis technologies.

Increased expectations of on-demand fulfillment and rising costs of logistics and inventory storage, places the company in a compelling position to help its clients and their consumers reduce waste and increase service reliability through more effective inventory management systems technology.

DSV Freight Forwarding – Creating scale-based economies for all stakeholders

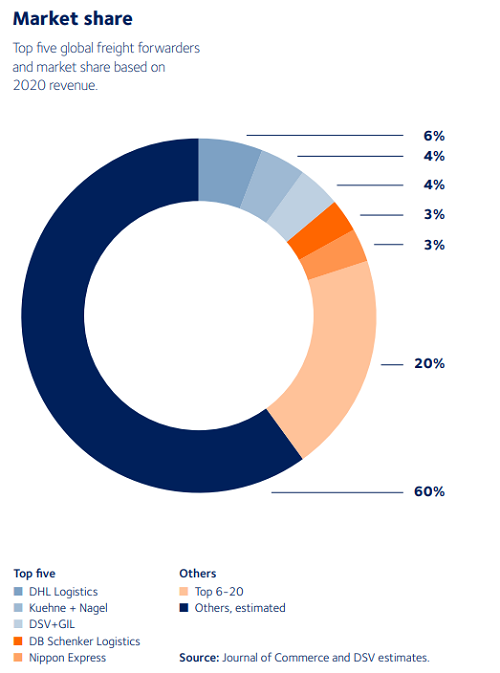

DSV is a global transportation and logistics company. Acting as a facilitator and coordinator, DSV serves companies looking to ship goods across the globe across a variety of transport methods including, land, sea and air. The company acts as the metaphorical grease in the wheels of a complex global supply chain. In 2021, the company shipped over 4 million tons of air and sea cargo, with each shipment having its own unique requirements that DSV had to coordinate.

2021 was a very challenging year for DSV due to Covid-19’s disruption of global supply chains. However, the scale and capabilities that DSV possess placed it in a compelling competitive position to serve its customers.

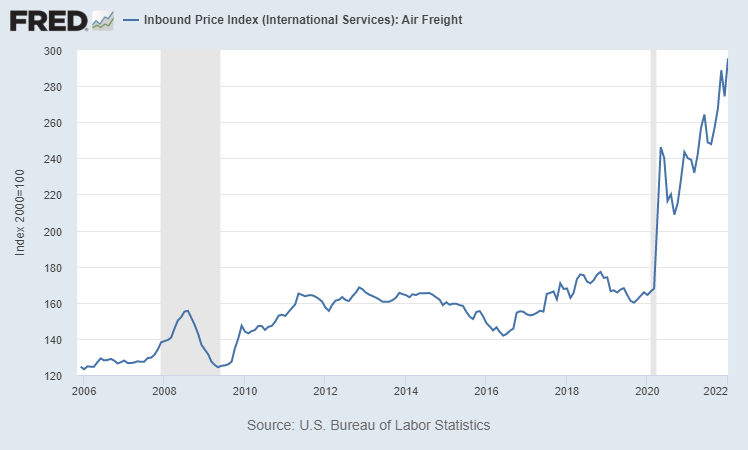

For example, with a large portion of transcontinental passenger aircraft grounded - planes that usually carry 40-50% of all airfreight - a severe shortage of airfreight capacity developed nearly overnight, often stranding freight in various regions. DSV’s large-scale and established agreements with dedicated freight aircraft owners enabled it to secure air cargo space for its customers to keep their freight moving.

Air Freight Inbound Price Index (2006-2022)

Additionally, with airfreight capacity materially reduced, rates to ship freight via air increased substantially. Here too, DSV’s scale and existing rate agreements enabled them to provide superior relative cost to their customers.

DSV is one of the largest and fastest-growing freight forwarders in what has historically been a highly fragmented industry. We see significant room for continued market share gains and consolidation in the large, highly fragmented freight and logistics markets. DSV’s recent acquisition of Switzerland-based Panalpina Welttransport Holding AG has the potential to create significant value for both stakeholders and shareholders, similar to what the company achieved with its successful UTI acquisition.

DSV’s culture and people are at the core of its competitive advantage. Logistics is a complex and rapidly evolving business, and it requires both rigorous processes and employee focus to achieve excellent customer service while preserving margins.

We believe the combination of greater scale, focused culture and strong global trade trends over the longer term places the company in a compelling position to expand its market-share whilst achieving attractive margins.

Better supply for a better-coordinated future

Economists have long remarked upon the power of trade to bring people together, but it took the Covid-19 pandemic to show the degree to which we are all adversely impacted when our supply chain infrastructure breaks down.

It is our expectation that the renewed focus on the infrastructure underpinning our economies from stakeholders spanning individuals to corporations, NGOs and governments will highlight the value that companies such as Zebra and DSV provide by investing in innovation to deliver more reliable and efficient supply systems.

Francyne Mu is a Portfolio Manager of the Franklin Global Growth Fund. Franklin Templeton is a sponsor of Firstlinks. This article is for information purposes only and does not constitute investment or financial product advice. It does not consider the individual circumstances, objectives, financial situation, or needs of any individual.

For more articles and papers from Franklin Templeton and specialist investment managers, please click here.