The Weekend Edition includes a market update plus Morningstar adds links to two recent articles including a video interview.

Weekend market update

From AAP Netdesk: On Friday, shares had their best day since October 2020 on the ASX and gave brief respite for investors fearing the Reserve Bank will join the rate rise movement of 2022. All share categories were up and consumer stocks outperformed, gaining more than 3%. There was improvement of more than 2% for financials, telecommunications, property, healthcare and industrials.The S&P/ASX200 closed higher by 2.2% on the day leaving the index 2.6% down for the week.

On Friday, Synlait Milk had a whopping rise of 10.6% as it raised its forecast milk price as demand for dairy products outstrips supply in some regions.

Workers sick with coronavirus are challenging supply chains, while strong inflation is lifting production costs.

Sales of ventilators for coronavirus patients helped ResMed's second-quarter revenue rise 12%. There had been greater demand for sleep and respiratory care devices, helped by a competitor's product recall. Expenses rose, however, and employee-related costs caused expenses to rise 10%. ResMed was down about 0.5% at $31.25. In mining, Rio Tinto was among the best and rose about 4% to $113.76. BHP gained 2.7% to $46.92. Fortescue shed 0.1%.

From Shane Oliver, AMP Capital: Global share markets saw another rough week as concerns about inflation and monetary tightening intensified against the backdrop of ongoing Russian tensions over Ukraine and Omicron disruptions. However, there was a decent bounce at the end of the week from oversold conditions helped by an Apple earnings beat. The bounce in US shares saw them rise 0.8% for the week, but Eurozone shares lost 2.3%, Japanese shares fell 2.9%, Chinese shares lost 4.5% and Australian shares fell 2.6%. From their highs to their lows US and Australian shares have now had 10% falls, Eurozone shares have had an 8% fall and global shares have had a 9% fall.

Speculative and interest sensitive areas have generally been hit the hardest with falls to their lows of 17% in Nasdaq, 31% in Australian IT shares and nearly 50% in Bitcoin and SPAC IPOs getting pulled. Long-term bond yields mostly rose, although the rise has been capped by haven demand.

On Friday in the US, however, the S&P500 recovered 2.4% and Nasdaq a strong 3.1%.

Monetary tightening fears are continuing to intensify, led now by the US Fed. The Fed left rates on hold but indicated that it will end bond buying in March, likely start raising rates in March and will then commence quantitative tightening (or QT) by letting its bond holdings run down. Fed Chair Powell’s comments pointing to a possibly faster tightening cycle than in 2015-2019 (due to higher inflation and lower unemployment) and not ruling out a rate hike at every meeting added to market nervousness though how high interest rates will rise.

We expect the first Fed rate hike in March, four or five rate hikes this year (in line with market expectations) and QT to commence in the June quarter. QT could add to upwards pressure on bond yields but this could be positive to the extent that it helps maintain a positive yield curve making it easier to avoid a recession.

***

Anyone who operates a small business knows inflation has hit them for some time. A shortage of staff builds pressure into wage increases, freight costs rise with fuel prices and supply chain blocks mean greater competition for goods. Restaurants and cafes have long been paying more for meat and vegetables and passing higher costs on to customers. Residential building costs were up 20% to 30% in 2021, with timber, steel and concrete prices rising 20% to 50% or more.

Yet as recently as 14 September 2021, only four months ago, Reserve Bank Governor Philip Lowe took the unusual stance of giving interest rate guidance for years ahead, based on the inflation outlook. It was strange at the time, and it looks even stranger now. He even went as far as to question the market pricing in rate increases. Speaking in an address to the Anika Foundation, Lowe said:

"In particular, the Board has said that it will not increase the cash rate until actual inflation is sustainably within the 2–3% target range. It won't be enough for inflation to just sneak across the 2% line for a quarter or two. We want to see inflation around the middle of the target range and have reasonable confidence that inflation will not fall below the 2–3% band again. Our judgement is that this condition for a lift in the cash rate will not be met before 2024."

"I find it difficult to understand why rate rises are being priced in next year or early 2023. While policy rates might be increased in other countries over this timeframe, our wage and inflation experience is quite different."

In the most recent outlook in the December 2021 Board Minutes, inflation was described as "low in underlying terms". Then: "The central forecast was for underlying inflation to reach 2.5% over 2023."

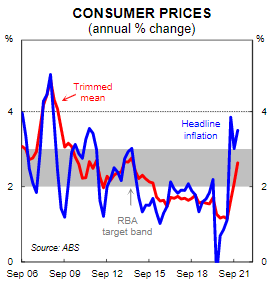

Well, it was higher this week. Lowe fronts the RBA Board next week to explain why "difficult to understand" is now obvious, and he was firmly off the pace. The RBA's preferred inflation measure, the trimmed mean (which excludes items recording large price increases or decreases) rose 1% in Q4 2021, well above the RBA's forecast 0.6%. The annual rate is now 2.6%, just above the mid-point of the 2-3% target range. On a six-month annualised basis, it is 3.5%.

CBA economists (the source of the above chart) wrote:

"The trimmed mean outcome was a massive overshoot on the RBA’s forecast for underlying inflation. We believe the RBA will need to make a fundamental adjustment to their 'low and gradual' inflation narrative in their upcoming communication next week. We shift our central scenario for the first hike in the cash rate from November 2022 to August 2022 (the risk lies with an earlier hike in June). We retain our view that the RBA will end the bond buying program at its Board meeting next week."

And on the day of the CPI release, the Australian market fell 2.5%. This week showed stockmarket investors what to expect as central banks move into a rate-tightening phase. Monday in the US was remarkable as it initially continued the sell-off from Friday, with the NASDAQ down 5% and the S&P500 down 4%. It looked like a major correction was underway. By the close, the S&P500 was up 0.3% and NASDAQ had gained 0.6% on the day. Heightened volatility has continued since.

Shane Oliver looks at the reasons for the recent sharp falls in stockmarkets and checks seven things investors should consider in deciding their next steps.

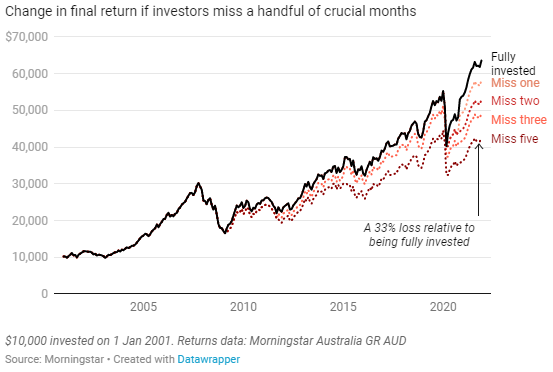

The investors most enjoying the market fall are those in cash who have long thought the market was too expensive. If only timing investing was easy. This chart from Lewis Jackson shows if $10,000 invested in Australian equities (the Morningstar Australia Gross Return Index) had missed only a few months of good returns, performance over the 20 years would be significantly down.

The rapid increase in wealth of most asset owners in 2021 also saw a surge in the size of Australian Exchange-Traded Funds (ETFs), rising 45% to $130 billion. The growth is impressive and it receives all the headlines for investment funds. But their unlisted competitors, the managed funds which mainly sit on platforms, hold $3.5 trillion. Barely noticed by the media and ETFs are the minnows. Yes, ETFs have a long runway but why are managed funds doing so well?

BlackRock's Larry Fink gave a high-profile talk last week, and Ollie Smith and Sunniva Kolostyak extract 10 highlights to summarise the view of the CEO of the largest fund manager in the world. On ESG principles:

“We focus on sustainability not because we’re environmentalists, but because we are capitalists and fiduciaries to our clients ... Every company and every industry will be transformed by the transition to a net zero world. The next 1,000 unicorns won’t be search engines or social media companies, they’ll be sustainable, scalable innovators – start-ups that help the world decarbonise.”

Ashley Owen looks at the growing inequality around the world and in Australia, with a minority enjoying the benefits of wealth distribution. In a new book published at the end of 2021, Ray Dalio, billionaire founder of Bridgewater, the world's largest hedge fund, predicts a 30% chance of civil war in the US within 10 years because of 'emotional polarisation'. Eventually, we will all suffer from rising inequality within nations and across the world.

Anyone nearing the ages of 55, 60 and 65 who may be considering ways to legitimately access their superannuation should check the retirement conditions of release. Liam Shorte explores some of the nuances and a focus on what 'gainful employment' means is especially important.

With the global worry about carbon emissions, many individuals manage their own lives to minimise their personal footprint. But Don Hamson offers an idea that will confront many people, that the typical superannuation fund is producing more carbon than the average Australian household. Check his argument and the numbers.

And Professor Kevin Davies explains how the Contracts for Difference (CFDs) work, why ASIC is cracking down on them for retail clients, and why anyone using them must know the highly-leveraged risks.

Two articles from Morningstar this week. Emma Rapaport interviews Johannes Faul on the implications of supply shortages for listed supermarket giants Coles and Woolworths, while David Meats checks supply and demand conditions for oil and explains why motorists are feeling the pinch at the bowser.

This week's White Paper is VanEck's ViewPoint, reviewing the end of 2021 in the context of decisions that seemed right at the time, in the heat of the moment, but all humans make mistakes.

Check below for the exciting guests and speakers at the upcoming Morningstar Investment Conference for individual investors, with online presentations and interviews for a day at a cost of only $25.

Graham Hand, Managing Editor

Latest updates

PDF version of Firstlinks Newsletter

IAM Capital Markets' Weekly Market Insight

ASX Listed Bond and Hybrid rate sheet from NAB/nabtrade

Indicative Listed Investment Company (LIC) NTA Report from Bell Potter

LIC Monthly Report from Morningstar

Monthly Funds Report from Chi-X

Plus updates and announcements on the Sponsor Noticeboard on our website

Morningstar Investment Conference for Individual Investors, all-digital event on 3 Feb 2022. Join us from wherever you are for research, insights, and analysis that can help you position your portfolio for the future. Register here.