In English, we say, “The squeaky wheel gets the oil.” The Chinese say, “The baby that cries the loudest gets the milk.” In other parts of Asia, they say “The nail that stands out gets pounded down.” In the Australian funds industry, the ‘wheel’ or the ‘baby’ or the ‘nail’ is Exchange Traded Funds, or ETFs – the noisy upstarts who demand attention as the centre of the investible universe.

Well done to them for creating this illusion, and their strong growth has reflected this high profile.

To the great credit of the issuers, the likes of Vanguard, VanEck and BetaShares decided a decade ago that if their ETF businesses were to grow, they needed to promote the benefits of the product structure and education first and their own brand name second. Investors learned about low costs and ease of access as if these attributes were unique to ETFs. And along the way, every milestone was breathlessly celebrated in the media as if they were the second coming.

Managed funds ceded profile to the ETF upstarts

Despite a fraction of the history of managed funds, ETFs have built a reputation that managed funds can now only envy.

A recent article in The Australian Financial Review, for example, shouted the headline, ‘Aussie ETFs set to crack 2 million investors in 2022.’ Firstlinks does the same, the first publication to note the ETF $100 billion milestone in February 2021. New fund listings are greeted like a cure for cancer.

In a 2022 outlook piece, CBA Economics discussed passive investing and the expectation that investors will be more risk averse in 2022. Then:

“the strong performance of diversified portfolios and listed equity Exchange Traded Funds (ETFs) may be difficult to replicate in 2022. As at November 2021, listed equity ETF market capitalisation was up 31.8% on the prior year.”

ETFs cleverly associated themselves with index or passive investing, and with that, cheaper costs. But managed funds were offering cheap index funds long before ETFs came along, and there are plenty of 'active' ETFs which are not cheap.

Managed funds ceded the space. When was the last time anyone wrote a headline about managed funds, such as when they ‘cracked’ $3 trillion (yes, trillion)? There is nobody promoting unlisted managed funds, and if media coverage is the gauge, it would be easy to think managed funds are an historical edifice. While individual fund managers devote their marketing budgets to the launch of their exciting new listed ETF, or their Listed Investment Company (LICs also have their own marketing association, LICAT), or their own brand name, managed funds chug away in the background.

Managed funds dominate the Australian market

According to ICI Global, in its Worldwide Public Tables for the end of 2021, the total assets in Australian unlisted managed funds were valued at about $3.5 trillion (ICI Global is part of the Investment Company Institute, representing funds globally with total assets of US$43 trillion or about A$60 trillion. This gives Australia a solid 6% of global managed funds).

The total size of Australian ETFs at the end of 2021 was … wait for it … start getting excited at the earth-shattering number … $134 billion.

That makes ETFs in Australia less than 4% of the size of the managed funds industry. Growing rapidly, tick, attracting new investors, tick, hitting the headlines, tick … tiddlers, tick.

LICs are well down the scale, suffering from their inability to pay selling fees to brokers and financial advisers, and where once they competed for size with ETFs, they hold only $56 billion or 1.5% of the size of managed funds.

Where is all this unlisted fund money sitting?

There is no public database of unlisted funds in the same way as offered by Australian exchanges, the ASX and Chi-X. To learn where the money is flowing requires access to institutional participants who process the transactions or monitor the markets.

Managed funds are the investment vehicle used by most financial advisers, who place their clients on platforms for ease of administration. For example, using the newer technologies of managed accounts, advisers can adjust the portfolio of all their clients in one transaction, greatly improving the efficiency of their back office. Managed funds flows therefore give an insight into what advised clients are doing.

Calastone claims it records 95% of Australian managed fund flows passing across its network, representing transactions between platforms and fund managers on behalf of investors. These flows are not the direct investments on a listed exchange and exclude ETFs.

Calastone reports that managed fund net inflows rose to $36 billion in 2021, up from $14 billion in 2020. The main gains were in equity funds, up 174% to $15 billion from only $6 billion in 2020. Investment flows were strongest mid-year but fell away by December. As ETFs have also experienced, international equity funds rose significantly, as well as small caps. Fixed income was doing well until inflation fears spiked.

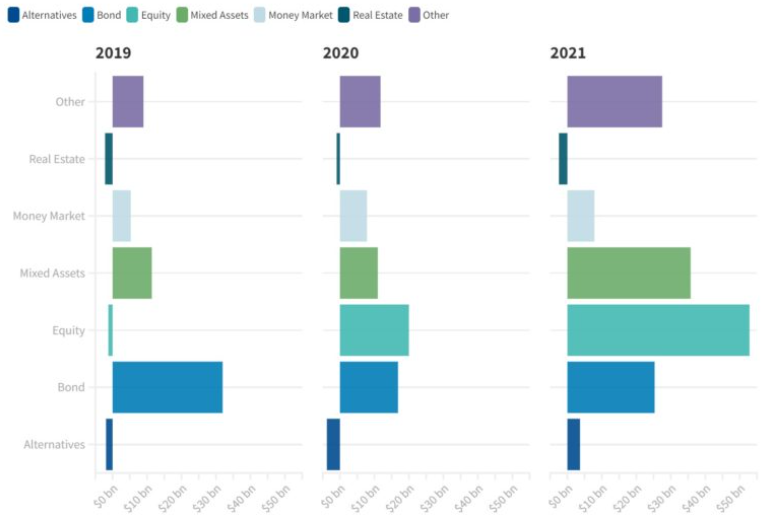

The chart below shows the strong flows into equity managed funds in 2021, suggesting fears of their demise are exaggerated. The increase from 2019 is especially notable.

Net fund flows into Australian managed funds by equity category

Source: Calastone

At this stage, it is unlikely that 2022 will match 2021, as July 2021 was the strongest month for inflows which then fell each month as Omicron and inflation hit confidence. Both factors will reduce flows this year. The global switch is on for Australian investors, with two-thirds of investments in 2021 in overseas markets compared to only half in 2020.

Ross Fox, Head of APAC at Calastone said:

“Australians have saved in record amounts during the pandemic, stowing away a seventh of their disposable income in 2020/21, almost three times more than in 2019. They were rather cautious with all this cash in the first year of the pandemic. But by 2021, as a clearer exit route emerged in the form of vaccines, fund flows responded dramatically. The flood of capital into managed funds in 2021 is a direct consequence of both higher risk appetite and piles of ready cash on household balance sheets. They are not alone. Investors around the world have behaved in a similar way.”

Equity and bond flows dominate, with equities a clear winner.

Net fund flows by asset class, global

Source: Calastone

What are the Australian platforms?

In retail funds under management, according to Plan for Life, the top five administrators are the IOOF Group (boosted by the recent acquisition of MLC), BT Financial, AMP, CBA/Colonial and Macquarie. Each holds over $100 billion on their platforms. The rapid risers over recent years have been the managed account providers, netwealth, Hub24 and Praemium, while Mercer, Perpetual and Challenger are also in the Top 10. Most other providers were in outflow. Annual gross inflows have been steady at around $190 billion a year.

The Top 10 hold about $1.1 trillion (as at end September 2021) in retail managed funds, up from about $900 billion a year earlier, across wraps, platforms or master trusts. The wraps are the biggest winners and most of the money is superannuation. For traditional platforms, the surging markets in 2021 contributed most of their fund growth and they will fall if the markets take a hit. They hold large balances built up over prior years before the landscape became more competitive.

In wholesale funds under management, Plan for Life data shows total balances of $1.5 trillion in September 2021, up from $1.1 trillion a year earlier. Leading providers who feature for wholesale services to institutions and not retail include State Street, Vanguard, Victorian Funds Management, UBS, First Sentier, Pendal and BlackRock. A lot of this money is passive index, a business Vanguard is stepping away from for institutions. Combined with the changes as AMP and IOOF, the data is highly volatile with earnings and business changes affecting flows.

While it is sometimes difficult to reconcile different sources of data across trillions of dollars, the fact remains that managed funds (in their many formats) continue to thrive in Australia despite the bigger profile given to their ETF competitors.

What are some implications?

These numbers present opportunities for investors and ETF issuers.

ETF issuers know there is a massive runway for growth, as despite their high profile, they represent less than 4% of funds versus 25% in the US.

Investors should realise there is more choice among thousands of managed funds than the 250 ETFs, and with proper platform use, the extra cost can be minor and might be worth paying for the efficient platform functionality. Some platforms can only be accessed via financial advisers, involving an advice fee, but some allow direct participation. It can be an easy way to put all investments in one place for tax and administration purposes.

ETFs are a welcome and burgeoning part of the investing landscape, with ease of access, low cost (for index options) and their variety of sectors and themes. No doubt they will win market share from managed funds, especially as adviser numbers dwindle, but for many years, managed funds will reign - despite few people talking about them.

Graham Hand is Managing Editor of Firstlinks. This article is general information and does not consider the circumstances of any investor.