The Weekend Edition includes a market update plus Morningstar adds links to two recent highlights from the week.

An hour into the media conference following Tuesday's increase in the cash rate to 0.35%, the Reserve Bank Governor Philip Lowe delivered a mea culpa. He said there would be an internal review later in the year of how the Reserve Bank provides forward guidance, that is, its predictions about the future course of interest rates. Lowe had earlier admitted he was embarrassed by the repeated guidance that cash interest rates would not rise until at least 2024. His confidence lulled many borrowers into a false sense of security that they did not need to fix loan interest rates.

To use Lowe's own words, he “should have done better”. He said he "does not want to predict what the Board will do". Then why did he even attempt to make a forecast about cash rates two to three years ahead when circumstances were changing quickly? It's amazing to recall that only three months ago, at his Press Club Q&A session on 2 February 2022, he said:

“Cast forward six months, what's likely to happen? I suspect we won't be buying as many electronics, we'll be going to cafes and travelling and the supply side problems in the chip market are now being resolved and the price of chips are coming down. I suspect on that category we'll go back to more normal rates of increase. The same with cars.”

He was expecting inflation to moderate by the middle of the 2022. Now the forecast for 2022 headline inflation is 6% and underlying inflation of around 4.75% versus the Reserve Bank range of 2% to 3%. He went further, again criticising market traders for pricing in substantial rate rises when he said:

"We keep looking at the markets and trying to understand what they're telling us, but I still struggle with how the same interest rate reaction is priced in for Australia and the US.”

In November 2021, he had been even stronger:

“I find it difficult to understand why rate rises are being priced in next year or in early 2023.”

Yet on Tuesday, he said, "I don't want to offer comments on the plausibility of market rates", which he has done for months. He said, "I'm not going to be drawn on fiscal policy" when he had encouraged governments to spend, for example, in October 2021:

"The fiscal responses by the Australian Government and the state and territory governments have also been providing welcome assistance in supporting household and business balance sheets."

In turning from dovish to hawkish within a few months, the Governor should indeed feel "embarrassed" and the review of the Reserve Bank which both sides of politics have promised after the election now has an even stronger reason to proceed. The review should look at all aspects of the massive support to the economy which has added fuel to inflation, including lending almost $200 billion to commercial banks at 0.1% for three years which contributed to the property price surge of 2021.

It was no surprise that leading cash rate forecaster, CBA's Gareth Aird, was unimpressed, as he was not expecting this week's increase. He said:

"Today’s decision means the RBA walked away from their April guidance that data over coming months (emphasis on plural) would inform their decision on the cash rate. Rather than wait for official data on the evolution of labour costs ... the Governor has instead today cited the RBA’s “business liaison” and “business surveys” to make the case that wages growth is moving sufficiently higher.

The business surveys had for some time indicated that wages growth was moving higher, so it was a surprise that the Board only today decided to put weight on “unofficial” wages data.

Reading between the lines, the RBA has simply been caught off guard by the strength of the Q1 22 CPI data ... We are disappointed in some aspects of the RBA’s communication today."

Amid the fear and inevitability of rising rates, another number has been overlooked. The economic growth for Australia for 2023 is forecast at only 2%, and Lowe also said on Tuesday:

“By mid-2024, headline and underlying inflation are forecast to have moderated to around 3%.”

The main lesson from all this, as Philip Lowe admits, is not to hang on his every word each month. He said the Board "follows the data" and is not on a preset path. He does not know what the future will bring and the thousands of pages of tea leaf analysis whenever he says a word like 'patience' or 'sustainable' have not helped anyone.

In fact, there is a decent chance that central banks will be forced to reduce interest rates within a year or two to stimulate the slowing economy. There is now considerable speculation about the so called 'neutral' cash rate, the point which neither stimulates nor contracts the economy. KPMG said:

"Some economists are now suggesting, that given the level of debt being carried across households, this neutral rate is now somewhere around mid-1%. KPMG considers it is most likely to be lower than historical levels, and probably closer to 2% to 2.5%."

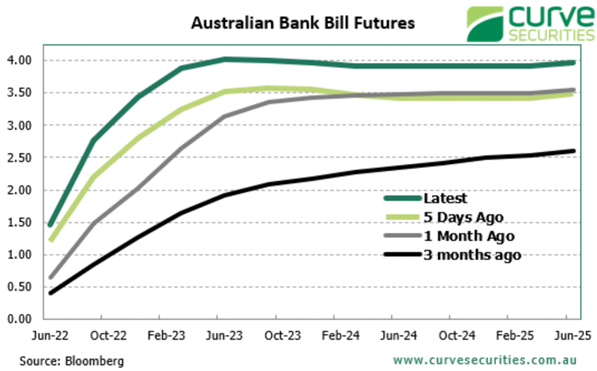

Which is well under current market rate expectations. Here is the latest trading in bank bill futures, at 4% by early 2023. Surely this can't happen, or we will see mortgage rate rises of 3.5% to around 6%, which would kill the residential property market and lift mortgage defaults. The Reserve Bank will not go there, but the market just keeps pushing higher.

One good side of rising rates is that savers will finally receive some reward, albeit not in real terms until inflation is under control. The rise in interest rates brings back into play that wonder of investing, compounding. As Charlie Munger (yes, him again) said, think long term because, “The first rule of compounding is to never interrupt it unnecessarily.”

A couple of charts stood out this week that summarise world markets.

The first shows why supplies of many goods from China are held up, with ships stuck around Shanghai. Scarcity of products feeds inflation as manufacturers and businesses face supply shortages.

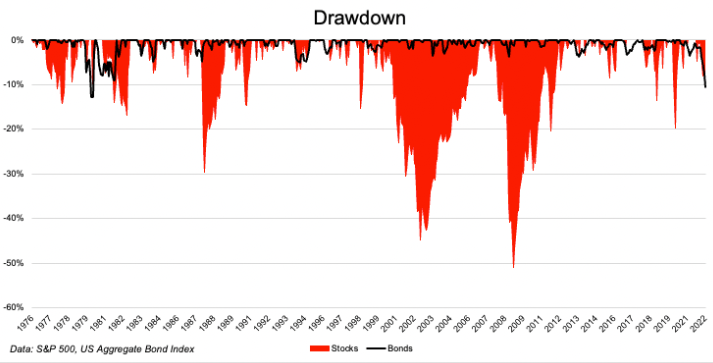

And second, the argument for a diversified portfolio where falling stockmarket returns are compensated by rising bond prices is not working at the moment as both US stocks and bonds have both fallen over 10% for only the second time in at least 50 years.

Graham Hand

From AAP Netdesk: The Australian share market has suffered its worst session in 10 weeks as traders reconsidered whether the US can tame inflation without tipping the world's largest economy into recession, The S&P/ASX200 closed on Friday down 159.1 points, or 2.2 per cent, to 7205.6, while the broader All Ordinaries fell 171.6 points, or 2.3 per cent, to 7467.6.

For the week the ASX fell 3.1 per cent, its worst stretch since a 3.9 per cent loss for the week ending 30 October 2020. It was also the ASX's worst daily loss since a 3.0 per cent drop on February 24 of this year. The market is now down 3.2 per cent for the year. Every sector on Friday fell at least 1.5 per cent, except for consumer staples which dipped just 0.2 per cent.

The sell-off followed an even worse session on Wall Street, where the S&P500 dropped 3.6 per cent and the Nasdaq fell 5.0 per cent.

The ASX's tech stocks were hit worst on Friday, collectively falling 4.5 per cent as Xero fell 9.1 per cent to a nearly two-year low of $86.57. Whispir, Redbubble, Airtasker, Nuix, Temple & Webster, Domain, Kogan.com, Megaport, EML Payments and Seek were among the tech or tech-focused companies sinking to their lowest levels in at least a year, with Temple & Webster and Whispir both down by double-digits.

Macquarie Group fell 8.0 per cent to a two-month low of $186.90 after cautioning it would be tough to maintain current growth levels in view of market volatility and rising interest rates. Still, the diversified financial giant delivered a record profit for fiscal 2022. All four big four banks were down, with NAB dropping 2.0 per cent to $31.62, CBA down 1.3 per cent to $102.40, Westpac dipping 0.8 per cent to $23.83 and ANZ falling 0.6 per cent to $26.76.

From Diana Mousina, AMP Investments: It was a turbulent week for markets after the US Federal Reserve raised interest rates by 0.5% at its May board meeting. This outcome was expected by the market and economists and the market actually rose from comments by Fed Chair Powell that 0.75% rate rises were “not something that the committee is actively considering” which alleviated fears of an extremely aggressive short-term rate hike profile from the Fed. The market pushed out US interest rate hikes out further over the next 1-2 years, with US interest rates now expected to reach close to 3.5% in a year. We think the US fed funds rate will peak closer to 3%.

The initial post-Fed rally was more than reversed the next day, with US shares down by 0.2% over the week and still 14% from its January high (with the tech-heavy NASDAQ faring even worse, down by 23% since early 2022). Australian shares are 3.1% lower over the week, but have outperformed over the past few months compared to global counterparts because of its lower relative tech weighting and high commodities exposure. Globally, Eurozone shares were 4.6% lower this week, Japanese shares rose by 1.6% (although markets were mostly closed this week for the national holiday of Golden Week) and Chinese shares were up by 3.3% (although markets were also mostly closed because of the Labor Day public holiday).

In the short-term, the outlook for shares is still messy and there may be more downside as markets worry about a significant economic slowdown or “hard landing” and aggressive interest rate hikes but signs of US inflation peaking and solid economic fundamentals (strong labour market, high accumulated savings) should be positive for shares on a 6-12 month view.

In this week's articles ...

The results of our Reader Survey on the 2022 election show clear expectations among our readers, but the 1,000+ comments received also demonstrate significant disillusion with our political process. It echoes statements made by former Reserve Bank Governor, Ian Macfarlane, who told the Actuaries Institute this week:

"Governments respond to what voters want them to do. At the moment voters, by and large, are terrified with someone coming up with a policy that will hurt part of the economy, part of the population. Talking about taxation, there’s no way a political party is going to put that forward because it will guarantee they won’t get elected.”

This policy failure is annoying many of you. Check the comments and results.

Stephen Hayes runs global property portfolios at First Sentier, and we sat down with him to discuss how commercial property is changing. He says the focus on office towers and shopping malls misses the main opportunities among exciting changes in many other parts of the property sector.

When Scott Morrison called the election for 21 May, betting agencies had the Labor Party at $1.33 to form government, with the Coalition at $3.25. That converts to a 75% probability of Labor winning and it is still at that price after a month of campaigning. Tony Dillon explores if the betting markets provide any predictive power.

The headlines are filled with negative news which has unsettled global financial markets. Panos Mamolis believes Australia is better placed than many other economies.

Are markets at an inflection point? Nick Griffin argues that the hit to growth shares is temporary while Marcus Burns believes we have returned to an environment where fundamentals and valuations will again drive returns.

Amid the war in Ukraine, the investment industry is debating whether countries should recognise the defence industry as a positive contribution to social sustainability. Victoria Maclean argues that arms do not belong in ESG funds.

Two bonus articles from Morningstar for the weekend as selected by Editorial Manager Emma Rapaport.

Veteran fund manager Paul Xiradis took the stage at Ausbil’s adviser roadshow on Wednesday with a simple message: good times lie ahead for Australian equities, writes Lewis Jackson. And Tom Lauricella delivers six charts on the bond market's big selloff and where it may go from here.

This week's white paper is from Magellan on holding global listed infrastructure securities as a way to help protect a portfolio against inflation.

Latest updates

PDF version of Firstlinks Newsletter

ETF Quarterly Report from Vanguard

IAM Capital Markets' Weekly Market Insight

ASX Listed Bond and Hybrid rate sheet from NAB/nabtrade

Monthly market update on listed bonds and hybrids from ASX

Indicative Listed Investment Company (LIC) NTA Report from Bell Potter

LIC (LMI) Monthly Review from Independent Investment Research

Monthly Funds Report from Cboe Australia

Plus updates and announcements on the Sponsor Noticeboard on our website