The Weekend Edition includes a market update (after the editorial) plus Morningstar adds links to two additional articles.

Markets seem fixated on whether the US Federal Reserve will change policy and slow hikes in interest rates. Arguably, an issue that’s just as important, if not more so, is when China will ease Covid lockdowns. The timing of this will have a significant bearing on the fates of commodities, inflation, and interest rates over the next 12 months.

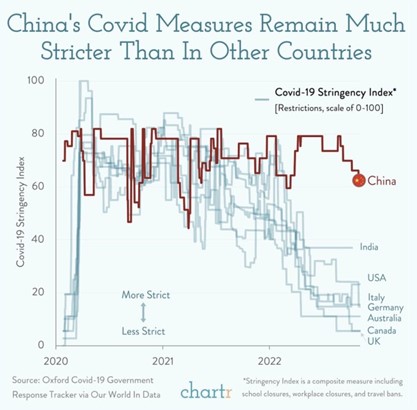

A recent surge in China-related stocks suggests investors believe that recent Covid lockdown protests in China will force the government’s hand to lift lockdown measures sooner rather than later. We think these investors will be disappointed as Xi Jinping will lose domestic credibility if he does this. Much more likely is that China cracks down on the protests, keeps the lockdown going until Covid cases decline, then gradually re-opens and stays open. This way, Xi can declare a success over Covid and ensure protests don’t get out of hand and threaten social stability – which is the Communist Party’s greatest fear.

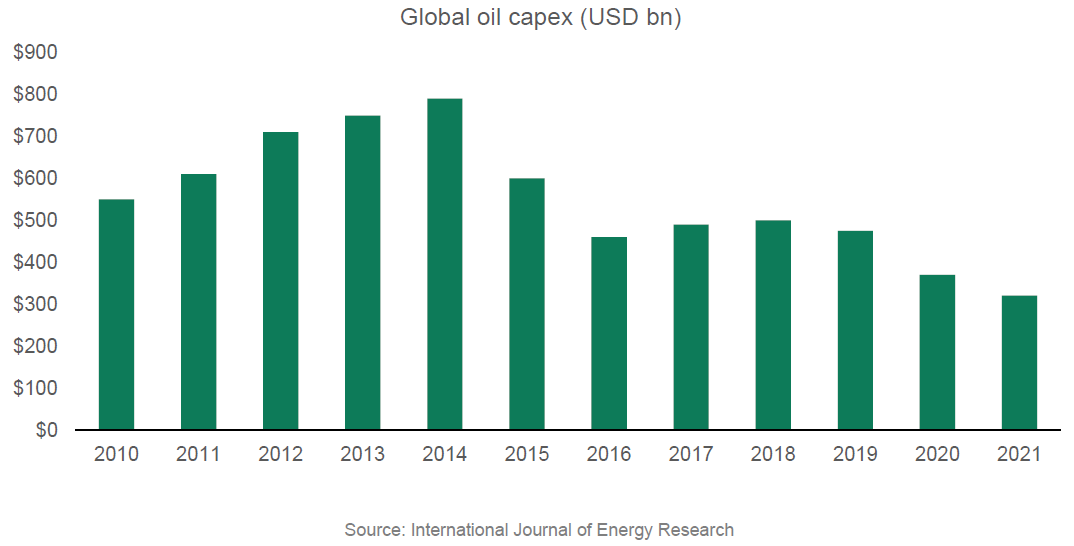

If re-opening happens in the first quarter of next year, as we anticipate, then oil and industrial-related commodities are expected to soar. Energy and the likes of copper remain extremely tight markets given massive undersupply of these commodities. A reopening may also see another spike in global inflation, and interest rates could potentially rise as well.

How widespread are the protests?

Your author lived in Asia as an investment analyst for more than four years, including in China and Hong Kong, and one thing I learned is to be sceptical of opinions on China from those outside the country (including mine perhaps!). China is a huge, diverse place and commentators often generalize and simplify the reality of what is a complex country.

That’s especially the case when it comes to issues such as protests. What seems clear is that there have been a number of relatively small protests over Covid lockdowns across several cities in China over the past week. What is less clear is how widespread the anti-lockdown sentiment is and how much of the protests are also anti-Xi Jinping.

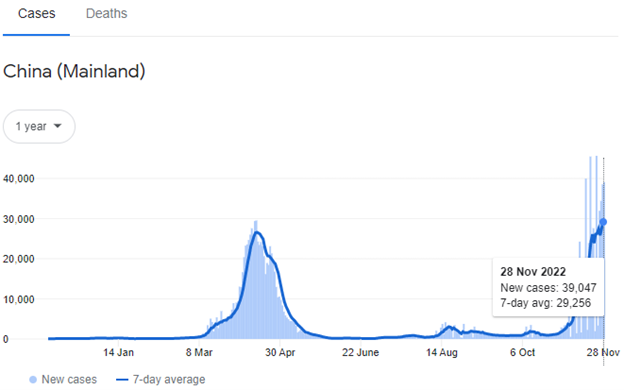

What’s bizarre is that China remains locked down even though cases remain exceptionally low. The latest daily new case number of 39,047 is tiny for a country with a population of 1.4 billion. Keep in mind that daily cases peaked in Australia above 150,000. China’s current new cases are the equivalent of 700 Australia-wide cases, when adjusted for population.

Note that from May to October of this year, China remained locked down despite daily new cases being below 2,000 for the entire period.

Source: Google

There’s no doubt that businesses are being impacted by the Covid protests. Apple supplier Foxconn has had severe disruptions at its iPhone factory in Zhengzhou. Those livestreaming the protests say workers were beaten by police. It appears lockdowns were only part of the worker grievances, though, as claims of overdue pay emerged too.

Government support measures

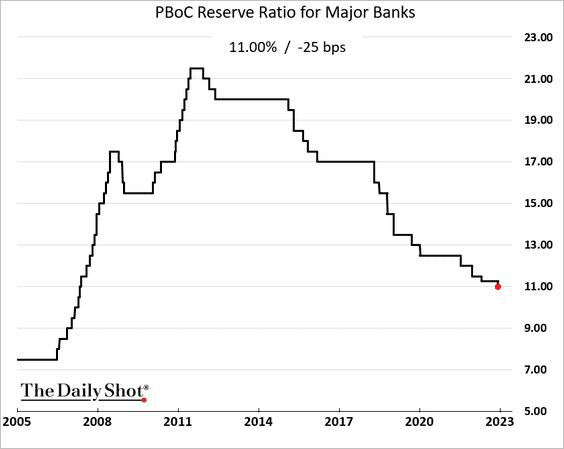

The backdrop for these ongoing lockdowns is daunting. The lockdowns are causing China immense economic pain and the government is trying to spur the economy through a variety of supportive measures. The People’s Bank of China has announced a 0.25% cut to the reserve requirement ratio to 7.8% and says it’ll inject around 500 billion yuan (A$104 billion) in long-term liquidity.

The government has also stepped-up support for the ailing real estate sector. This includes 250 billion yuan (A$52 billion) for bond financing of private property developers and the announcement of 16 measures to support the housing market, including supporting issuance of construction loans and encouraging banks to extend mortgage repayments for home buyers.

When will China reopen?

President Xi Jinping has taken personal responsibility for China’s Covid-zero policy. He lauded the country’s efforts in 2020-2021 when cases remained low and pointedly referenced overseas case numbers at that time to highlight the success of his policy.

With the latest lockdown protests, there are three probable scenarios which investors need to consider:

- The lockdowns stay until Covid essentially disappears, or at least gets to very low numbers. That’s likely to mean a further prolonged period of lockdowns, which have already been in place for nearly three years. China may get more vigorous in extinguishing any protests.

- Lockdowns ease immediately and the country puts up with any subsequent increase in Covid cases. The protests may be too much of a danger to social stability and that forces the move. China had started to gradually re-open over the past few months until this latest spike in cases.

- Protests are quelled, and China remains locked down until Covid cases ease somewhat. They then re-open and stay open. This way, Xi can declare victory over Covid, protests die down and the economy gets up-and-going again.

Markets seem to be betting that on scenario 2. It seems to us that the greater probability lies with scenario 3. The reason is that opening now after almost three years of Covid-zero rhetoric would dent Xi’s credibility. It’s a dangerous thing for a dictator to lose credibility.

Scenario 3 would appear to be a win-win for Xi and the Chinese people, who are no doubt craving freedom from being locked down for so long. First though, protests need to decline and Covid cases need to go down.

If we had to guess, we would pin reopening around Chinese New Year. However, that’s purely a guess given it’s dependent on both Covid cases and protests.

What happens to markets under these scenarios?

Let’s look at the likely market reaction to each of the scenarios.

Under scenario 1, China’s economy would continue to slow, and it would dampen demand for goods and inflation globally. Commodity prices might fall. That would help worldwide inflation to ease, perhaps a lot. And that would be supportive of the US Federal Reserve slowing interest rates hikes.

The concern might become one of slowing economic growth rather than inflation. Continued lockdowns would hurt exporters such as Australia and European countries such as Germany.

While stocks might bounce initially, any hints of a slowdown would cap any upside. Bonds would likely be the largest beneficiary. Commodities would be in the doldrums for some time to come.

Under scenario 2, there would be a significant and near immediate spike in Chinese holidaymakers and spending on goods such as luxury goods would boom. Demand for energy and commodities would re-accelerate as the economy surges.

Your author remains positive on the likes of oil and copper as both are significantly undersupplied and any pickup in Chinese demand may send prices higher, potentially a lot higher.

Scenario 2 would be positive for commodities prices, emerging markets’ stocks and currencies. It would be bearish for interest rates and bonds, and for countries with indebted consumers.

While Australia would appreciate the higher commodity prices, higher inflation and higher interest rates would weight down the consumer and, of course, the housing sector.

Under scenario 3, it would be the same as scenario 2 except with a time delay. We are guessing the first quarter of 2023 might be the time, though there are many variables which will determine that.

China’s long-term problems

We’ve talked about scenarios for China over the next 12 months, but the long-term picture for the country remains problematic. There are three main issues:

- A prolonged real estate slowdown, not unlike Japan in the 1990s. For far too long, China stimulated real estate and infrastructure to pump up economic activity and GDP. The effectiveness of that stimulus has waned, slowing economic growth, and resulting in falling residential and commercial property prices. Homes in so-called 3rd and 4th tier cities have seen price declines of up to 20% since 2020. Kenneth Rogoff, Professor of Economics and Public Policy at Harvard University, suggests these cities account for more than 60% of China’s GDP so any slowdown there will have broader implications. He also notes the real estate sector accounts for roughly 23% of China production and 26% of final economic demand.

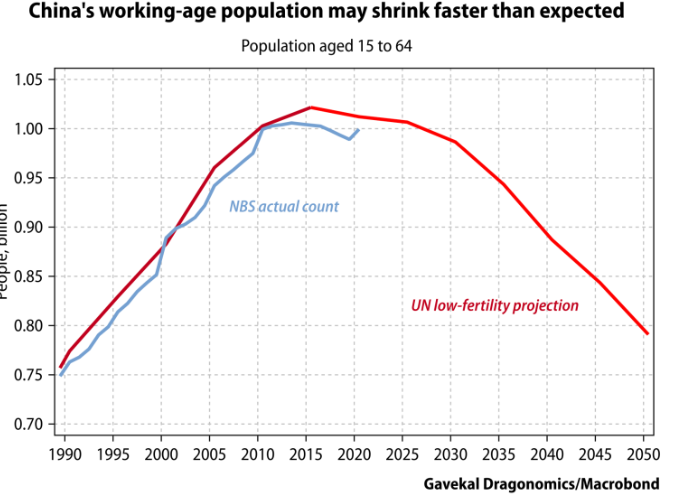

- Demographics also bode poorly for China’s long-term economic growth prospects. The UN estimates that China’s working age population may decline by two-thirds by the end of this century. China’s long-time one-child policy is mostly to blame.

The importance of a shrinking working age population is that it weighs on economic demand. After all, GDP (gross domestic product) equals the population growth rate plus GDP per capita. A paper by Rand Corporation found that a 10% increase in the fraction of the population aged +60 decreases the growth rate of GDP per capita by 5.5%. “Two-thirds of that reduction is due to slower growth in labor productivity of workers across the age distribution, while one-third arises from slower labor force growth”, according to the paper.

- China’s 20th Party Congress in October clearly emphasized security and stability as priorities and deemphasized the economy. The focus on security is understandable given the US has effectively declared a tech war through its restrictions on semiconductors, initially implemented against Huawei and extending them to include all Chinese corporations (a recent article in Firstlinks provides more detail on this). But it doesn’t bode well for the private sector. Internet companies have already gone through a regulatory assault aimed at purging “bad habits” associated with online gaming, live-streaming, music, and private tutoring. There’s no sign of government incursions into the private sector letting up any time soon.

In this week's edition ...

Potential changes to superannuation remain a hot topic. This week, we have Jon Kalkman as our guide on how the super system was originally designed and how we ended with the system we have now. He says the numerous changes to super over the years have complicated a system which was flawed from the outset.

Meanwhile the equity or inequity of super tax breaks for retirees has provoked intense debate among Firstlinks' readers. Some view these breaks as a travesty while others believe they're fair. We try to shed more light on the issue by collating the views of a number of our readers.

Shane Woldendorp of Orbis Investments suggests investors face a difficult decision when choosing a fund manager. He outlines four principles for choosing the right active manager which can help make a difference to investor portfolios.

After a dismal year, could bonds be set for a comeback? Tim Dowling of Aquasia thinks the pullback has opened up opportunities in asset-backed securities and RMBS, especially for those investors looking to maximise returns from investment grade assets while also reducing their exposure to interest rate risk.

Australian small caps have also been hammered this year and Simon Brown from Tribeca Investment Partners is hunting for value. He thinks tech, consumer discretionary and building materials look interesting. And stocks benefitting from the renewable energy push are also attractive.

Andrew Mitchell says investors who abandon fund managers because of the recent market downturn are making an error. He provides compelling evidence that even if you have the 'perfect portfolio', large drawdowns are inevitable.

We also look at how cryptocurrency advocates seem to be in total denial that their war against fiat currency has ended. FTX’s downfall should prove the final straw as the world is moving on from crypto mania and it'll be better off for it.

In the weekend update by Morningstar, Christine St Anne reports on Morningstar senior analyst, Brian Han's, four key investment themes for 2023, including potentially more trouble ahead for the world's social media giants. And Nicola Chand investigates whether the RBA's rate hikes are already having some impact on inflation and the Australian consumer.

This week's White Paper comes from Pinnacle Investment Management affiliate, Hyperion Asset Management, reflecting on recent portfolio performance and the importance of keeping a long-term view.

Finally, we recently did an article on the need for company directors to get director identification numbers (director ids) by 30 November this year. The ATO has announced it won't penalise around 700,000 company directors who have yet to apply for director IDs if they do so by 14 December.

***

Weekend market update

A stronger-than-expected reading of November payrolls didn’t bother the bulls on Friday, as US stocks recouped steep early losses to settle little changed for a second straight day following Wednesday’s intense rally. Treasurys similarly rebounded from an initial selloff as two-year yields finished at 4.28% compared to 4.25% yesterday while the long bond finished at 3.53%, its lowest since September. WTI crude pulled back to $80 a barrel, gold edged lower to $1,812 per ounce and the VIX slumped to 19, its lowest since early April.

From AAP Netdesk: The local share market gave back most of Thursday's gains on Friday, but still put in a respectable showing for the week. The benchmark S&P/ASX200 index closed on Friday down 52.9 points, or 0.72%, to 7301.5. For the week the index finished up 42 points, 0.58%, its fifth week of gains out of the past six weeks. The broader All Ordinaries closed down 50.5 points, or 0.67%, to 7503.5.

The interest-rate-sensitive real estate sector was the biggest loser on Friday, falling 2.7% as Goodman Group dropped 4.1% and Charter Hall fell 5.1%.

The energy sector was close behind, dropping 2.5% as Santos lost its appeal of a court ruling that overturned approval of its $4.7 billion Barossa gas project off the coast of NT. Santos fell 3.8% to $7.15, Woodside dropped 2.6% to $35.71 and Beach Energy dipped 2.4 per cent to $1.80 as it raised its bid for Warrego Energy. Warrego, a Perth Basin gas explorer now the subject of bids from three parties including Gina Rinehart's Hancock Energy, was up 8.7% to a three-year high of 28.25c.

In the heavyweight mining sector, losses for the iron ore giants were outweighing gains for goldminers as the price of the precious metal hovered just below $US1,800 an ounce. BHP dropped 1.6% to $45.76, Fortescue Metals dipped 1.4% to $19.68 and Rio Tinto retreated 1.1% to $111.94. Newcrest gained 2.1% to a six-month high of $21.09, Northern Star rose 1.5% to a seven-month high of $11.08 and Evolution climbed 0.7% to a five-month high of $2.88.

All the big banks were lower, with CBA down 1.4% to $106.95, ANZ down 1.2% to $24.65, Westpac dipping 0.7% to $23.76 and NAB dropping 1.0% to $31.38.

From Shane Oliver, AMP: Global share markets mostly rose again over the last week rising to new recovery highs on the back of more signs that inflationary pressures may be peaking & central banks becoming a bit less hawkish amidst optimism about an easing in Covid rules in China. The positive global lead saw Australian shares rise for the week and they are now down by just 2% for the year to date. The gains in Australian shares were led by materials, IT, Telco and health stocks, with miners benefiting from signs China is easing its Covid rules as did oil, metal and iron ore prices. Bond yields fell further and the $A made it back above $US0.68 as the $US fell.

The past week saw more positive signs on inflation and interest rates:

- Fed Chair Powell’s comments were far less hawkish than feared and if anything leaned a little dovish, explaining the relief bounce in share markets mid-week. While he said there was “still some ways to go” on inflation and that the terminal rate will likely be “somewhat higher” the latter was a downgrade from “higher” early in November and he provided a strong indication that the pace of hikes will slow and said that this is “a good way to balance the risks” to the economy.

- US core personal consumption deflator inflation slowed again in October to 5%yoy from a high of 5.4%yoy in February.

- Eurozone CPI inflation also slowed in November with core inflation stable, possibly enabling the ECB to slow the pace of rate hikes this month.

Australia’s new monthly CPI Inflation Indicator also showed more signs of having peaked.

There is likely more to go yet for central banks, and labour markets still remain too tight for comfort, but the increasing evidence of easing inflation pressures suggest we may be nearing the peak in the rate tightening cycle.

With US inflation leading that in Australia by around six months, the signs of a slowing in the US - highlighted by our Inflation Pipeline Indicator - augur well for Australia too. But there are a range of domestic signs as well pointing to a peak in inflation here, probably this quarter.

As noted above, the ABS’s new monthly CPI Indicator is showing signs of slowing. To be sure it needs to be interpreted with lots of caution, particularly as it excludes 30% of items included in the quarterly CPI including gas and electricity which will boost the quarterly CPI this quarter and as such the RBA is unlikely to read too much into it just yet. But it does appear to be slowing and if 70% of the quarterly CPI is cooling down that has to be a positive sign. The 3-month rate of change in the monthly CPI Indicator peaked in April at 2.5% and it is now 1%.

James Gruber

Latest updates

PDF version of Firstlinks Newsletter

ASX Listed Bond and Hybrid rate sheet from NAB/nabtrade

Indicative Listed Investment Company (LIC) NTA Report from Bell Potter

LIC Quarterly Report from Bell Potter

Plus updates and announcements on the Sponsor Noticeboard on our website