The Weekend Edition includes a market update plus Morningstar adds links to two additional articles.

Although commonly attributed to Winston Churchill, he was not the first to say the famous words:

“Democracy is the worst form of government, except for all the others.”

What he did say (on 11 November 1947) is similar but more expansive:

"Many forms of government have been tried, and will be tried in this world of sin and woe. No one pretends that democracy is perfect or all-wise. Indeed it has been said that democracy is the worst form of government except for all those other forms that have been tried from time to time …’

Despite the extraordinary achievements and progress of billions of people over centuries, we have not improved on a system of government which involves a person walking into a polling booth every few years and marking a box for a preferred candidate. Democracy comes with troublesome flaws such as media influence, lobbyist access to politicians for favours, backroom deals, party politics and faulty personalities, but theocracy, autocracy or oligarchy are worse.

Democracy is dysfunctional but we have not come up with anything better.

Monetary policy is the same. It is flawed in its application but we have not devised an improvement, such that our central bank's attempts to fulfill its responsibilities under the Reserve Bank Act are blunt and imprecise. The Act says:

"Its duty is to contribute to the stability of the currency, full employment, and the economic prosperity and welfare of the Australian people."

Look up 'monetary policy' on the Reserve Bank's website and it says:

"The Reserve Bank is responsible for Australia's monetary policy. Monetary policy involves setting the interest rate on overnight loans in the money market (‘the cash rate’)."

That's mainly it. The cash rate, plus some activities on money supply. To contribute to the prosperity of the Australian people, the central bank weapon of choice is setting the cash rate. Consider some way this fails:

1. There are about 10 million households in Australia (ABS 2022) but only one-third of them have a mortgage. Most people are not hit by higher mortgage payments, yet that is the primary inflation control mechanism.

2. Increasing the cash rate stimulates the economy by boosting the nominal incomes of millions of Australians through higher term deposit and bond rates. If anyone argues it is not stimulatory because the older people who are the savers do not spend as much as younger people, consider this:

3. Fiscal policy often works in the opposite direction, as governments give cost-of-living relief when inflation rises, putting money into pockets when the central bank is trying to take it out.

4. The cash rate increase does not directly hit borrowers. It relies on the 'transmission mechanism' into bank lending rates before repayments are hiked. Banks lent billions on long-term fixed rates which are maturing over 2023 and into 2024, such that the impact on borrowers feeds slowly into the system but then hits severely.

5. Monetary policy is primarily demand-side economic management. It aims to expand or contract economic activity by controlling the cost of money. But in the current cycle, inflation is significantly driven by supply-side factors, such as Russia's war in Ukraine, the pandemic's impact on supply chains and natural disasters in Australia. None of which are sensitive to interest rate changes.

6. Rising cash rates feed into parts of the inflation calculation, the Consumer Price Index (CPI), generating an updraft. The Australian Bureau of Statistics advises:

"Housing is the highest weighted group in the CPI, accounting for around one quarter of the basket. It includes new dwellings purchased by owner occupiers (houses, townhouses and apartments), rents and major renovations."

Consider how supply shortages have driven up inflation, contributed to a decline in construction and rising rents. Says Bill Mitchell, Professor in Economics and Director of the Centre of Full Employment and Equity at the University of Newcastle:

"So we enter a ridiculous circularity. The RBA hikes interest rates. Rental inflation accelerates even though the other factors driving the overall CPI inflation trajectory are in decline. The RBA then claims the CPI inflation is not falling fast enough. The RBA hikes again … Rinse and repeat."

Borrowers who can least afford higher repayments are hit the most. Its doubtful they feel an increase in the cash rate 11 times in a year from 0.1% to 3.85% has improved "the economic prosperity and welfare of the Australian people".

The Reserve Bank and Governor Philip Lowe are acutely aware of the mental health implications of rising rates, and the Governor has made a point of meeting with suicide prevention agencies. The May 2023 Statement of Monetary Policy (page 32) includes this acknowledgement:

"Community services organisations have raised concerns regarding the sharp increase in demand for their services over recent quarters, including for financial aid, domestic violence and acute mental health support, food bank services and housing assistance. They note that there has been a rise in the number of people seeking assistance for the first time, including renters and people with mortgages."

A policy which causes severe mental health problems for strugglers but puts more money in the hands of wealthy savers is a deficient way to control inflation. The Reserve Bank acted the worst when leaving the economic stimulus of 'whatever it takes' in 2021 as inflation was already taking hold. It poured fuel on the fire when it should have withdrawn oxygen.

Of course, Australia's central bank was not alone, and this week, we publish a short extract from famous fund manager Stanley Druckenmiller's recent interview at the Sohn Conference 2023 in the US where he says of the Federal Reserve's actions a year ago:

"Then realising they have probably made the biggest mistake in the history of the Fed, they slammed on the brakes. They raised rates 500 basis points (5%) in the last year."

“I’m sitting here staring in the face of the biggest and probably the broadest asset bubble, forget that I’ve ever seen, but that I’ve ever studied.”

"If we get a hard landing, there will be unbelievable opportunities, and I don't want to miss those opportunities by blowing my money now and having some 20-30% loss where my head is all screwed up when those opportunities present themselves."

The Federal Reserve Act was signed into law in 1913, about 110 years ago, and for a leading voice in US investing to call the extremely loose monetary policy of 2021 "probably made the biggest mistake in the history of the Fed" is quite a claim.

This week's wage price index showed a rise at a decade-high 3.7% in the year to March 2023, and 0.8% for the quarter, both in line with expectations. After the release of the Reserve Bank minutes on Tuesday, CBA's Gareth Aird confirmed:

"Our central scenario puts the current 3.85% as the peak in the cash rate, while the near-term risk sits with another rate hike ... We continue to expect 50bp of rate cuts in Q4 23 and a further 75bp of easing in 2024 that would take the cash rate to 2.6% - a more neutral setting."

***

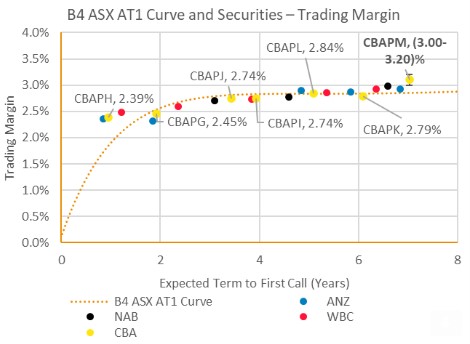

CBA has a new hybrid in the market, expected to list as CBAPM with an indicative margin of 3% to 3.2% and issue size of $750 million. The Bank will be swamped by demand, given the Bank Bill Rate is now about 3.9%. NAB economists came out this week expecting one or two more cash rate increases. Either way, a gross return of about 7% on CBA is a decent reward for the risk of hybrids. This chart courtesy of BondAdviser shows the relative value and extra return for longer term.

***

As 30 June is six weeks away, the Australian Taxation Office (ATO) has advised its three focus areas for this tax period:

- rental property deductions

- work-related expenses

- capital gains tax.

The ATO is especially critical of rental property owners:

"The ATO’s review of income tax returns show 9 in 10 rental property owners are getting their return wrong, and often sees rental income being left out, or mistakes being made with property related deductions – like overclaiming expenses or claiming for improvements to private properties."

The ATO has sophisticated data matching capabilities, and warns:

"Don’t fall into the trap of thinking we won’t notice if you sell an asset for a gain and don’t declare it ... Don’t bury your head in the sand."

***

In the time-honoured tradition of the Commencement Speech loved by US universities, Bill Gates gave the 2023 version to North Arizona students last week. As Gates says, he never actually graduated from any university, as he left Harvard after three semesters to start Microsoft. He's done well regardless. The advice he shared is worth a quick read, making these five points:

- Your life isn’t a one-act play.

- You’re never too smart to be confused.

- Gravitate toward work that solves an important problem.

- Don’t underestimate the power of friendship.

- You’re not a slacker if you cut yourself some slack.

***

Buy-Write funds have been available to retail and wholesale investors in Australia for many years - I worked on the design of one at Colonial First State about 20 years ago - but they are becoming more common, including many ETFs. Several new funds have launched on the ASX and Cboe listed exchanges in recent months. How do they work and do they suit the current market conditions?

Graham Hand

Also in this week's edition ...

The Quality of Advice Review has once gain shone a spotlight on the escalating costs of financial advice. While there have been a lot of vague statements about advice fees, they've been few specifics on the actual costs involved. Anne-Marie Esler from Padua Solutions breaks down the fees for us. She notes that while costs are skyrocketing, demand for financial advice remains strong.

Nicholas Paul of MFS Investment Management hails the cheapest global small cap valuations seen in decades. He says there are similarities between the market set-up today and that of the early 2000s, after which small caps beat large caps handsomely over the next eight years.

Look up any reputable finance book and you're likely to see a statement about how bonds offer lower returns than stocks although with less risk. Andrew Mitchell of Ophir Asset Management takes issue with the latter. He says that while it may be true in the short term, it isn't over longer-time horizons, with important implications for asset allocation.

The charge towards net-zero emissions is a US$50 trillion global opportunity over the next 30 years, according to Munro Partners' James Tsinidis. James gives us three themes and one stock that should benefit from the climate transition.

Professional money managers have many advantages over individual investors: more information, greater access to company management, as well as staff to help them. Yet they also have some constraints, and it's here James Gruber suggests that individuals can potentially compete with the best in the business.

Two extra articles from Morningstar for the weekend. Joshua Peach reports on an ASX blue chip that is undervalued for the first time in almost three years, while Leslie Norton looks at Tesla's key-person risks.

And in this week's white paper, Orbis Investments seeks to debunk three oft-repeated myths about value investing with hard data and considered analysis.

***

Weekend market update

On Friday in the US, stocks finished marginally down to conclude another banner week for the bulls with 1.5% and 3.6% gains for the S&P 500 and Nasdaq 100 respectively. Treasurys traded weaker once more, with the policy-sensitive two-year yield rising to 4.28% from 4.24% yesterday and the long bond likewise increasing four basis points to 3.95%. Gold bounced to US$1,978 an ounce, WTI crude remained near US$72 a barrel, and the VIX edged higher towards 17.

From AAP Netdesk:

The local share market gained ground on Friday for a second straight day amid optimism over both the state of the global economy and talks to raise the US debt ceiling.

The benchmark S&P/ASX200 index closed Friday up 42.7 points, or 0.59%, at 7,279.5, in its highest close since May 5. The broader All Ordinaries gained 44.5 points, or 0.6%, at 7,471.5.

The ASX tech sector was the biggest gainer on Friday, climbing 2.2% after a strong session on the Nasdaq. Xero advanced another 5.4% to an over one-year high of $108 following Thursday's strong earnings report, while Wisetech Global rose 0.7% to $71.20.

Financials were the second-best performer, collectively climbing 1.5% as all of the Big Four retail banks had a solid day.

ANZ rose 1.4% to $23.97, Westpac climbed 1.3% to $21.23, CBA added 1.8% to $99.80, and NAB advanced 1.5% to $26.80.

Insurance companies performed even better, with IAG climbing 4.6% to $5.19 and Suncorp rising 1.9% to $12.62.

The heavyweight mining sector was mostly in the red, however, with losses for both iron ore miners and goldminers. BHP fell 0.2% to $44.16, Rio Tinto dropped 0.5% to $109.42, and Fortescue Metals was basically flat at $20.52, while in the gold sector Newcrest dropped 1% to $13.31 and Evolution fell 1.6% to $3.72.

Elsewhere, Austal had soared 25.1% to a five-month high of $1.995 after the Tasmanian shipbuilder's US subsidiary was awarded a new contract worth up to $3.2 billion to design and potentially build seven new surveillance ships for the US Navy.

From Shane Oliver, AMP:

Global share markets rose over the last week. Over the week Eurozone shares rose 1.3%, Japanese shares rose 4.8% to their highest since 1990, and Chinese shares rose 0.2%. Supported by the positive global lead Australian shares rose by 0.3% with gains in IT and resources shares offsetting weakness in retailers, health and property stocks. However, bond yields rose globally and in Australia, with the local money market now pricing in the RBA holding in June but a 64% probability of another 0.25% RBA rate hike by September. Oil and iron ore prices rose but metal prices were flat to down. The $A was little changed as the $US rose.

While shares could have a further tactical bounce if there is quick US debt ceiling deal, they continue to look vulnerable over the next few months. From their lows last year global and US shares are up 17% and Australian shares are up 13% as investors have been buoyed by evidence of peaking inflation, anticipation that central banks are near the top, and so far resilient growth and profits.

However, we remain of the view that global and Australian share markets are vulnerable to a rougher period ahead: share market gains so far have been narrowly based favouring defensive sectors than would be normal at this point in a recovery; US debt ceiling brinkmanship and eventual resolution could create volatility ahead; banking stress is continuing in fits and starts in the US resulting in additional monetary tightening; leading economic indicators continue to point to a high risk of recession in the US and Australia; China’s recovery is looking less robust; metal and energy prices have softened with oil down despite several OPEC supply cuts suggesting weakening demand; central banks are probably close to the top but risk doing more; and the period from May to September is often rough for shares.

We remain of the view that shares will do okay on a 12-month view as central banks ease up but the next few months are likely to be rough.

Curated by James Gruber and Leisa Bell

Latest updates

PDF version of Firstlinks Newsletter

ETF Quarterly Report from Vanguard

ASX Listed Bond and Hybrid rate sheet from NAB/nabtrade

Monthly Bond and Hybrid updates from ASX

Listed Investment Company (LIC) Indicative NTA Report from Bell Potter

LIC Quarterly Report from Bell Potter

Plus updates and announcements on the Sponsor Noticeboard on our website