Weekend market update: The US market gave back a little on Friday with the S&P500 down 0.7% and NASDAQ 0.9%. This pushed the US lower by 1.5% for the week as markets weighed up the Biden stimulus package versus higher taxes. The Australian S&P/ASX200 benchmark was flat on Friday but down 0.6% for the week. A growing acceptance that BNPL is replacing credit cards pushed Afterpay beyond $135 at one stage ... remember the $8 less than a year ago? BHP also hit a record of $47.54 on iron ore prices but Tyro continued falling due to software problems.

***

Two major decisions by the Morrison Government confirm that anyone saving for retirement or a home must make plans in the face of great regulatory uncertainty. One change is already announced, the other is pending.

Almost everyone was taken by surprise in September 2020 when Treasurer Josh Frydenberg said the Government would abandon the responsible lending laws. They were a high profile issue in the Hayne Royal Commission (remember that?) recommendations, released in February 2019, following evidence that the banks had been lax in their lending practices. Insisting that banks conform with the law led to credit restrictions and a fall in property prices over 2019, but Kenneth Hayne had said in his Final Report:

"If this results in a ‘tightening’ of credit, it is the consequence of complying with the law ..."

In response, Josh Frydenberg proudly proclaimed that the Government would adopt all Hayne's recommendations. Bank behaviour in not conforming with the law was unacceptable and "From today, the sector must change, and change forever." Now, apparently, those laws are no longer required, which is little comfort to those who missed out on a home in early 2019.

Second, it is doubtful that the compulsory increases in superannuation to 12% (and perhaps even 10% on 1 July 2021) will go ahead. The debate about the trade-off between super and wages has powerful forces on both sides, with the added dimension of a possible 'homes first, super second' policy.

It has such broad political appeal beyond first-time buyers, as older people want their children to own a home. And now we hear the Government is considering a choice between pay and super, which sounds like a change in the concept of 'compulsory superannuation'. Minister Jane Hume (now in Cabinet) is firmly in the camp arguing super reduces present-day wages.

This new slogan has the same potential impact as the Coalition's 'retiree tax' campaign against Labor's franking credit policy. If it's true that Scott Morrison plans to call an election in 2021, expect this super trade-off to feature heavily.

Either way, the rules around saving for a house or retirement change regularly, requiring plans to remain flexible and not build in regulatory assumptions.

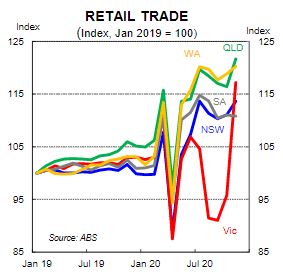

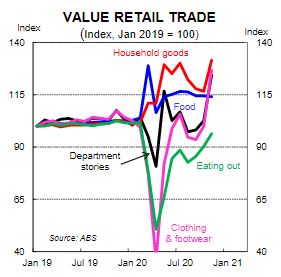

Making wealth accumulation even harder is the market uncertainty. On the one hand, retail sales are booming and people are clearly in the mood to spend, even in lockdown. As shown below in charts from CBA, the recovery from the pandemic has been extraordinary.

On the other hand, the number of leading global investors issuing dire warnings grows by the day, with Carl Icahn and Jeremy Grantham giving their most severe 'bubble' predictions. This week, we reproduce Grantham's paper in full, including:

“The one reality that you can never change is that a higher-priced asset will produce a lower return than a lower-priced asset. You can’t have your cake and eat it. You can enjoy it now, or you can enjoy it steadily in the distant future, but not both – and the price we pay for having this market go higher and higher is a lower 10-year return from the peak.”

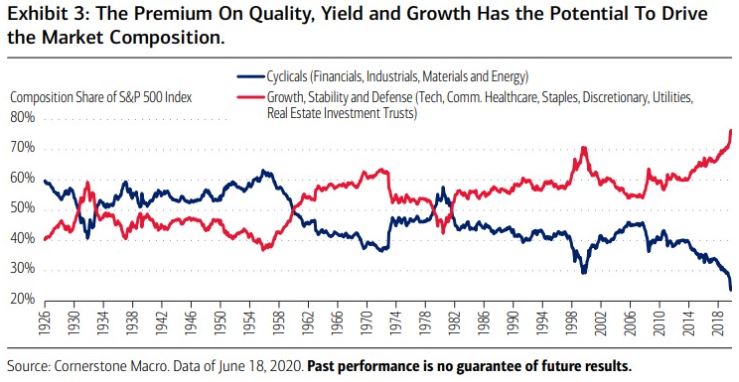

The complication is that today's market has the massive benefit of low interest rates, little inflation and a Fed injecting unlimited liquidity. Even the Biden Presidency now pleases the market, which is ignoring the prospect of higher taxes because they pay for greater stimulus. The reason some fund managers are producing great results and others are terrible is apparent in this chart of the S&P500 since 1929. The market share of cyclicals (financials, industrials, materials and energy) has never been smaller, and index funds buying according to price exacerbate these trends without analysing the investment merit.

Ashley Owen charts the sharemarket results for Australian and global companies over the last 12 months, and it's a great pointer to why your portfolio might not have done so well when there is so much talk of a bubble.

As these stock performances feed into managed fund results, some fundies delivered a wonderful 2020 while others suffered. It's a tough gig when you stick to your principles but they don't work. Emma Rapaport looks at the Morningstar database of 480 flagship Australia funds, and finds the top fund delivered +33% in 12 months while another struggled at -11%. Ouch! 44% is a lot in a retirement savings plan. The trick now is deciding whether to hang on or switch as the results could be the oppositive next year. There's a lot of luck involved.

Speaking of luck, do you own any collectibles? Who hasn't squirreled away a first-day cover, a mint coin, an Olympic pin or a 'collector's edition' of something in a bottom drawer? In a vague hope they will rise in value, they gather dust for decades. What do you do when it's time to clear up and nobody wants them?

Noel Whittaker has delivered financial advice to millions over his long career. He describes some advice given to a client 30 years ago, and how patience and compound interest has improved her retirement. Just invest and wait.

Leading universities in the US are known for their 'endowment' investing, finding assets which throw off regular income to meet the needs of running their activities. Rob Holder explains this style of investing and who it is suitable for.

Those of us for whom rising wealth and income inequality causes disquiet know there is little we can do about it. If the market delivers vast wealth to a few billionaires, if the Fed ramps up asset prices, if a bubble rewards risk, there is not much an individual can do but call out the injustice. However, Andrew Macken shows there are ways these movements affect all portfolios and investors can manage the implications of rising inequality.

And repeating, Jeremy Grantham's piece is reproduced in full. It's a long and sober read which one day will prove correct. Grantham has been a bear for many years, and there is always a timing problem with these predictions which ultimately look prescient.

Finally, NAB's decision to redeem its hybrid, NABHA, first issued in 1999, shows how these securities can deliver much higher returns than their margins suggest. Those in the know realised NAB would one day repay $100 for a hybrid which no longer qualified as Tier 1 regulatory capital (from 1 January 2022), and there have been plenty of chances to buy this at a big discount over the last five years, as we wrote in February 2020.

This week's White Paper from the Capital Group called 'The long view: investing through adversity' explains how staying invested through periods of volatility has rewarded long-term investors.

Graham Hand, Managing Editor

A full PDF version of this week’s newsletter articles will be loaded into this editorial on our website by midday.

Latest updates

PDF version of Firstlinks Newsletter

ASX Listed Bond and Hybrid rate sheet from NAB/nabtrade

Monthly market update on listed bonds and hybrids from ASX

Monthly Investment Products update from ASX

Plus updates and announcements on the Sponsor Noticeboard on our website.