Weekend market update: The S&P/ASX200 index had its best week in a month, rising 0.8%, the same amount as Friday's increase. Australia's small IT sector recovered well to be up 2.3% for the week. The broad US market was even stronger on the back of the US$1.9 trillion stimulus, with the week's rise of 2.6% to a record high. However, bond rates increased again and the tussle between bonds and equity valuations will be a major theme of 2021.

***

First up, two pieces featuring Julie Bishop, Australia's first female foreign minister. In her speech at the CFA conference to celebrate International Women's Day (IWD), she discussed leadership skills and her time in government. Then we add her interview with Leigh Sales on Monday night's 7.30 on ABC TV which was equally revealing.

A reminder we published additional articles for IWD including how women invest, the 'Witch' of Wall Street, and business culture.

On the markets and the bull v bear arguments ...

NASDAQ roared back 4.5% on Tuesday night, just when people were calling a major fall in tech prices. While markets always have differences of opinion, fund managers are further apart than I can ever recall at the moment. At one end is the 'bounce back' theory of strong consumer spending. At the other is the overvaluations during a pandemic with mutant virus threats.

Correction are not proceeded by someone waving a red flag a week before. Waiting for it to happen risks being on the wrong side of it. While the best strategy is to stay invested and not sell after a heavy fall, many people panic and turn to cash at the worst moment.

I'm reminded of a couple of famous lines in Ernest Hemingway’s first major novel, The Sun Also Rises.

“How did you go bankrupt?” Bill asked.

“Two ways,” Mike said. “Gradually, then suddenly.”

Seth Godin developed this idea in a 2014 note on his blog. He said,

"This is how companies die, how brands wither and, more cheerfully in the other direction, how careers are made. Gradually, because every day opportunities are missed, little bits of value are lost, customers become unentranced. We don't notice so much, because hey, there's a profit. Profit covers many sins. Of course, one day, once the foundation is rotted and the support is gone, so is the profit. Suddenly, apparently quite suddenly, it all falls apart. It didn't happen suddenly, you just noticed it suddenly."

It also happens in markets, and we currently have many signs of excess, of overvaluation, of hubris, of overconfidence. We know there's something weird when Bitcoin hits US$50,000, Tesla is worth more than all the other large car makers in the world combined, and governments borrow and spend unlimited amounts (US Government stimulus packages during COVID are now worth over US$7 trillion ... that's US$7,000,000,000,000). But we shrug our shoulders and go along with it, until a crisis comes gradually, then suddenly.

The strongest argument of the bulls is the rebound trade. Here's a new phrase you can use whenever anyone asks you to justify the current high valuations: 'revenge spending'. Some fund managers believe that when Americans and Europeans emerge from the pandemic and lockdowns, the burst of buying activity (or revenge spending) will lead to a massive economic rebound.

And maybe they're right. Jeff Schulze, Director at ClearBridge Investments made a strong pitch at the Portfolio Construction Forum last week. He has also written that growth conditions will be the best in 40 years in late 2021:

"There is going to be a powerful force that’s going to be unleashed on the US economy, which is consumer balance sheets and the excess savings that have been accumulated over the last year ... So, our core view has and continues to be that you’re going to have this deferred gratification or revenge spending in the middle part of the year."

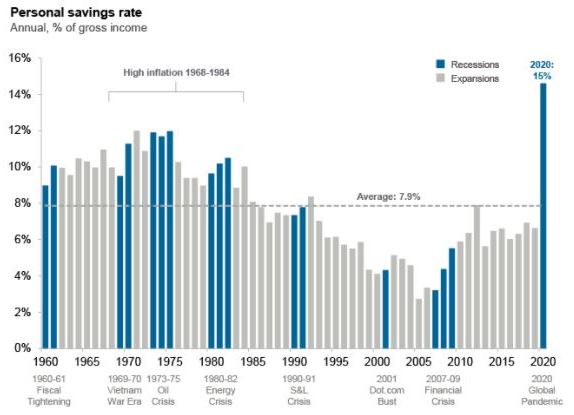

Here it is, in the middle of a pandemic and a rapid rise in unemployment, record personal savings in the US.

This week, The Economist leads with the same point, saying:

"The economic controls implemented during the second world war make today’s restrictions on restaurants and football stadiums look lax. In America the government rationed everything from coffee to shoes and forbade the production of fridges and bicycles. In 1943 its entire automobile industry sold only 139 cars. Two years later the war ended, and a consumer-led boom ensued. Americans put to use the personal savings they had accumulated in wartime. By 1950 carmakers were producing more than 8 million vehicles a year. The big question is whether or not the rich world can repeat the post-war trick, with pent-up savings powering a rapid bounce-back."

What about Australia? The latest ABS savings numbers released last week, see below, show a decline in the household saving ratio for December 2020 to 12.0% from 18.7% in September 2020 and 22% in June 2020. These are historically very high, suggesting Australia could also see revenge spending.

Australian Household Savings Ratio

Source: ABS National Accounts

We focus on this big question today.

While Andrew Mitchell does not believe the market as a whole is expensive, he identifies four bubble areas which show investors need to watch risk closely.

This week's White Paper is an article and video by Hamish Douglass, where he gives a detailed review of vaccine developments, with a sobering outlook for mutations. Hamish says he reads a couple of scientific papers a day, and he is at the cautious end of fund managers. He says risks are foreseeable and investors could have their "shirts ripped off" if something goes wrong, and he sees "clear speculative frenzies" in some assets.

“There is no margin for error in markets at the moment … At one point you want to have risk on because of the stimulus and the economic recovery holding up, but there are other warning signs that you could have your shirts ripped off if something goes against you ...

If it is the new inflation coming, the Federal Reserve at some point is going to have to change course and start lifting interest rates. That is a disaster for financial markets. The very long-term – is all this printing of money going to lead to a new paradigm and monetary induced inflation in the world? That is a great question that I do not know the answer to … it is very foggy out there.”

What about simple indexing to take advantage of the overall market rise? Shane Wodenthorp looks inside passive investing benchmarks to see how concentrated they have become, leaving even the index with heavy sector bets.

Then Harry Chemay examines whether all these attempts at forecasting have much merit. Ultimately, despite the expertise, they are educated guesses, leaving investors to decide for themselves.

And we draw on the ultimate investor, Warren Buffett, who has not been beyond criticism himself recently. Susan Dziubinski reviews his latest shareholder letter for three main features and the long-term consistency of how to make money.

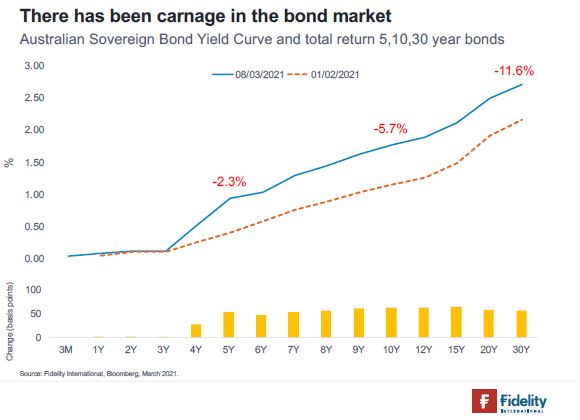

So where to invest? One possibility is to take on more risk in non-government bonds, and Adam Grotzinger describes the parts of the market where he sees value, especially when inflation threatens. To emphasise the point, see the chart below of capital losses on Australian Government bonds in six weeks between 1 February and 8 March 2021: a loss of 5.7% in the 10-year and 11.6% in the 30-year as rates rose at the long end. Such volatility is equity-like, leaving doubts about bond capital protection.

This rise in bond rates and uncertainty about inflation stems from government spending, debt, money printing and QE. It may not sound exciting but it's important and Tony Dillon gives as simple an explanation as possible on what is happening. Grab a coffee and concentrate (your mind, not your portfolio!).

Graham Hand, Managing Editor

A full PDF version of this week’s newsletter articles will be loaded into this editorial on our website by midday.

Latest updates

PDF version of Firstlinks Newsletter

ASX Listed Bond and Hybrid rate sheet from NAB/nabtrade

Monthly market update on listed bonds from ASX

Indicative Listed Investment Company (LIC) NTA Report from Bell Potter

Plus updates and announcements on the Sponsor Noticeboard on our website