Our September survey sought readers' views on how their own portfolios, investment decisions and outlook had changed from our earlier COVID survey in April. We compare the results from both surveys.

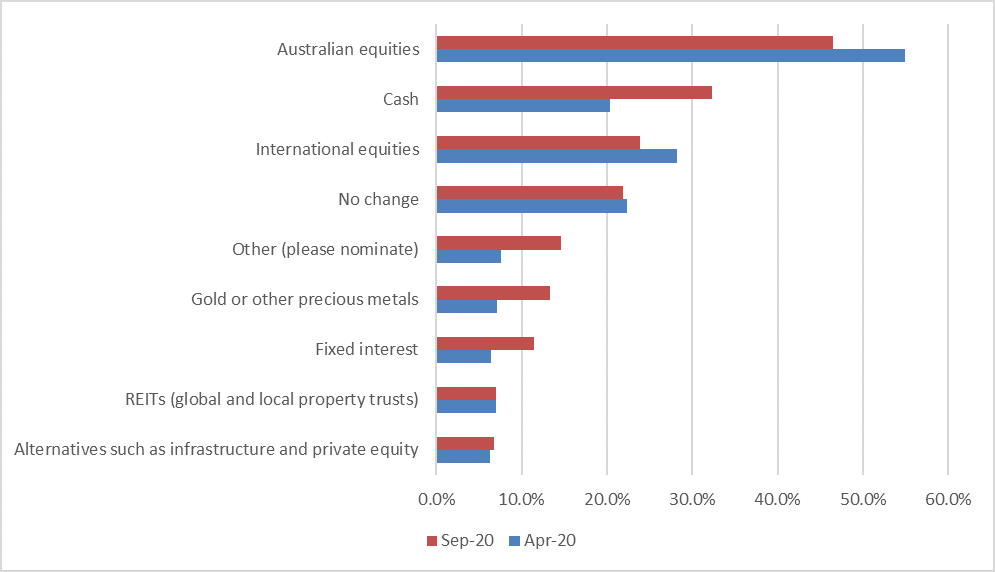

Into which asset class(es) have you invested more since COVID-19 started? (multiple responses allowed)

| |

Apr-20 |

Sep-20 |

| Australian equities |

54.9% |

46.5% |

| International equities |

28.3% |

23.8% |

| REITs (global and local property trusts) |

7.0% |

7.1% |

| Fixed interest |

6.4% |

11.4% |

| Alternatives such as infrastructure and private equity |

6.3% |

6.8% |

| Gold or other precious metals |

7.1% |

13.4% |

| Cash |

20.4% |

32.4% |

| No change |

22.4% |

21.9% |

| Other (please nominate) |

7.6% |

14.6% |

While Australian equities was still the top asset class being invested into in this latest survey, there has been some shift towards cash, fixed interest and gold since the April survey. The number of people making no change to their asset allocation remained fairly steady at 22%.

Additional comments, including details on 'other' responses, are included below.

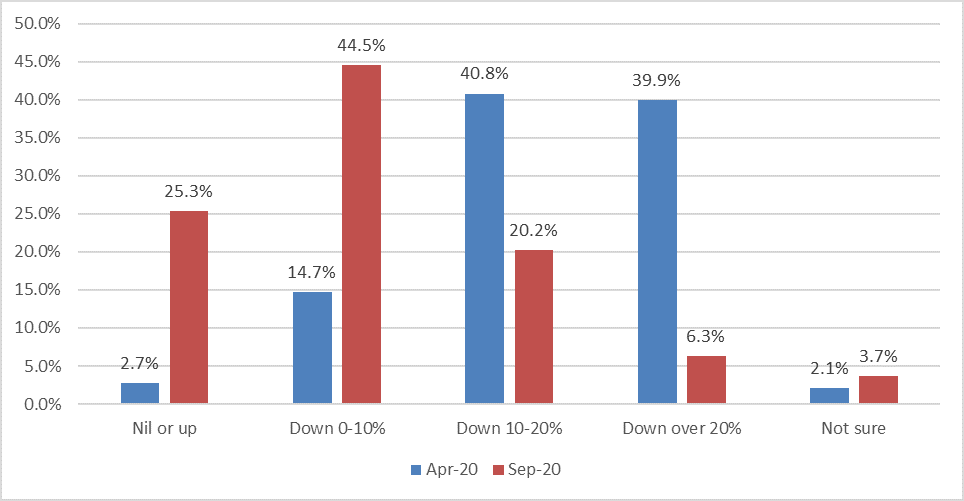

How much has the value of your investment portfolio changed since the end of January 2020? (approximately)

This comparison between April 2020 and September 2020 shows that investment portfolios are recovering from their initial Covid-19 shock. The earlier survey revealed over 80% of people reported portfolio values down more than 10% from the beginning of 2020 (40% saying values were down more than 20%). Now, most are seeing a depletion of less than 10%, with a quarter of people saying the value is flat or higher.

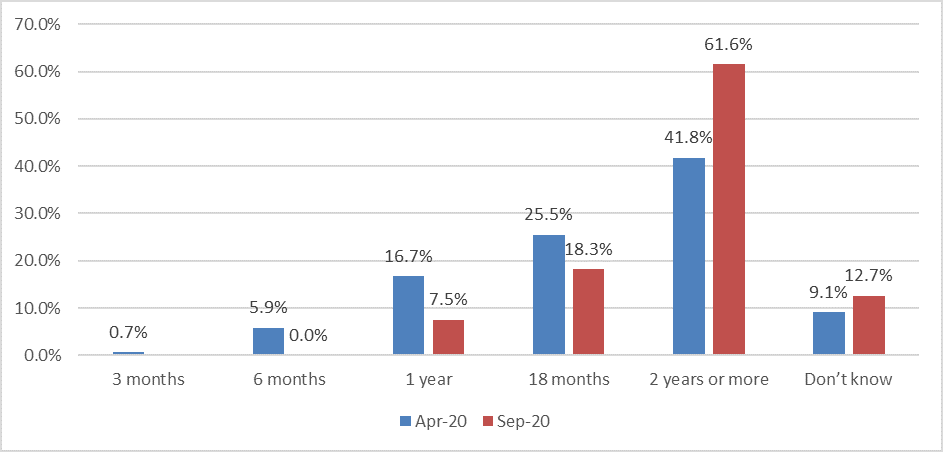

How long will it take for economic activity to restore to pre-COVID-19 levels?

The clear change from April to September is that economic recovery will take longer than first thought. Those saying '2 years or more' increased from 42% to 62%. The 'don't know' camp also increased.

We've included some of the comments below.

Comments on asset allocation

- ETFs

- Bank hybrids and LICs.

- Unlisted property trusts

- Cash will depreciate but PMs will at least create some insurance against it.

- Commodities

- My fund managers have reduced allocation to alternative assets by around 20% (they are still at a healthy 25% of the portfolio) and increased allocation to international equities by 13% (around 34% of the portfolio).

- Diversifying into international equities as the Australian printer is working overtime

- Technology, gold miners and bio-pharma

- You can't live off a cash return of 1%

- Actively managed, pure stock picking, index agnostic, managed funds or direct investing in selected investments across all asset classes (including private equity)

- Listed hybrid securities.

- Holding my investments but not adding to them

- Market too unstable to discern better investments

- Allocated share purchase plans only. Otherwise no change

- I’m a great fan of LICs in these uncertain times as they invest in a diverse range of shares and have greater market expertise than me.

- Become more conservative with my super options

- ETF for Robotics & Artificial Intelligence

- Initially cash, then back into equities

- shorts, commodities

- Sold shares to pay down property loans.

- But am now looking to reverse the moves made in March

- Waiting for the markets to tank

- I am not prepared to invest in shares until I can see where the country is going in terms of our disastrous financial position

- An allocation to contrary bear funds.

- I am largely invested in Australian small companies using about 10 rigorously selected active fund managers while maintaining a small reserve of cash and line of credit which should see us through downturns such as at present for perhaps 2-3 years. It has served us well so far ...

- Have not bought or sold essentially. funds are accumulating are being held in cash but will probably end up in bank capital notes or similar

- I am a long term buy and hold investor. This is another blip and I haven't really got too worried. With perfect hindsight I could have done really well but that is not my strategy.

- Listed hybrid securities

- No major change for me.

- ETTs - due primarily as to what stock will recover best and which ones will struggle.

- I moved 50% to cash this month, we’re getting nearer the fall.

- Trying to adjust for better returns

- Corporate Bonds

- Super fund, which invests in multiple asset classes.

- Have invested in some US technical ETF's.

- Property

- I feel that stock prices are quite vulnerable to bad news.

- now with industry fund instead of SMSF.....sleep better

- Corporate bonds, foreign and domestic

- Private investments

- On-line stocks. Health-related. Packaging. NT likely gas discoveries.

- To be precise, Australian equity ETFs and International equity ETFs

- GDX and AGD = gold and silver miners, I'm up 38% and 78%. Have 1/3rd of assets sitting in cash in case of crash and then opportunities

- Superannuation

- Property

- Sit on what we have got and hopefully ride it out. Historically it will eventually come good again. If one sells when it is down the loss is real.

- Preferences will change from gold to other growth companies and eventually back to a proportion of dividend paying companies.

- I set the strategy, review every 6 months, but generally just stick with what works

- International Equities funded from Cash and sold-off Australian equities in tourism, airports, dividend centric LIC's.

- Switching with bias to income and technology

- Government bonds and gold

- Small share purchases in April and July, saving up an emergency buffer in the bank which will be maintained long after COVID is gone.

Comments on economic recovery

- I believe further shocks are to come in the Australian equities market, probably when the full effects of the recession start to hit and government support measures start to reduced. The shock to businesses due to coronavirus and the recession are yet to hit the market.

- Depends on how much the government interferes in the marketplace.

- This is hostage to government actions, a vaccine and the US election outcome.

- being optimistic, I hope sooner rather than later. Many businesses havent been too much affected in other parts of the country where most are still open. Except in Melbourne where most business is closed!

- Victorian will be hurt hard - the lockdown will shut down business activity in ways that won't be fully apparent til JobKeeper has ended

- Much longer than 2 years

- Depending on a vaccine

- 5 to 10 year negative impact

- using the availability of a vaccine as the starting point

- With no effective vaccine soon it will be longer

- Politicians seem far too optimistic about an effective early vaccine.

- Much dependent on when overseas travel opens up. That will depend on a vaccine.

- This will be a slow, uneven 'recovery' with protracted low growth, large number of business failures, high unemployment, and widespread uncertainty prevailing among consumers and investors

- Lockdowns were necessary at first, but better treatment options are now available. We should be concentrating on treating people as soon as they are diagnosed with available & cheap medications such as Ivermectin, Hydroxychloroquine, Zinc, Vitamin C, Vitamin D. Steroids can also be used later in the course of the disease. Stopping all economic activity, while not addressing treatment options is counterproductive.

- How would you possibly know given all the variables, including the human behaviour element??

- Combined with China trade and other countries winding back global supply chains.

- The economy will be COVID normal which will be different from recovering to what was before.

- If you include flying, l think it will be even longer. I don’t think we are going to see those really cheap tickets again any time soon.

- This is difficult to estimate as the ongoing actions continue to change. Once all of Australia is undertaking standardised actions that the general populace understand and agree with, the economy should largely recover within six months or so. There will still be significant 'losers' after this time.

- In countries with herd immunity, high casualties, it will recover quicker

- 18 months for things to get back to a reasonable level - but longer to absorb the excess capacity in the economy

- This on presumption of vaccines available within 6-12 months.

- Victoria's position makes any prediction impossible from where I sit.

- Depends on 2 semi-dependent things 1. How well we learn to live with live-COVID pre vaccine and 2. When mass vaccine.

- Depends on how long the idiots who run VIC, QLD and WA keep undermining the economy.

- wait until people are released from dickhead dans house arrest and the we see the true damage over the next 6-12 months

- There will likely be more "waves" of infection in many countries before vaccines are available and provided to substantial numbers of the various populations. At least as important will be the increasing trade restrictions with China due to our inept government's political and non-diplomatic stance on several issues.

- subject to medication to control or eliminate the virus allowing significant easing in environmental controls globally.

- A long time seems the most appropriate answer.

- Tempted to say I don't know. We really need a vaccine to create any form of certainty but I think it is at least 2 years until we have some form of economic normal.

- I would like to think earlier but to either have a vaccine or the virus just fizzles out so we can resume where we left off in Jan 2020 will take at least two years

- So much depends on availability and adoption of an effective cheap vaccine and Government policies at all levels. Likely 5+ years for Australia.

- It will depend upon the border wars and effect on unemployment. Qld, WA and SA are too strident in their approach, one of the poor effects of a federation.

- Economic activity is one of the rewards for "controlling" COVID-19.

- The only significant contribution to domestic economic growth (other that inflated real estate) prior to COVID-19 was net immigration. No possibility of that returning within 12 months. No likelihood of inbound tourism or education (major export earners) in the same timeframe. Total absence of any government leadership other than the gas fired pipe dream.

- I think that it will be a long road back. We have done a lot of damage to our economy. Debt will increasingly drag us back.

- probably a lot longer in Victoria

- could be much longer. we dont know what we dont know

- China situation will make recovery more difficult

- Depends on how the covid trajectory runs, and this is clearly in the 'don't know' category. If vaccines work, things will bounce. If they don't (by say 12 months time) a big set-back might be on the cards.

- Depends on state and federal government decisions

- we saw real positive signs from April to June with economic activity returning until June when Victoria wave came and I see this as a positive, people are ready to act once some certainty is in place

- I am concerned that we have created an inter-generational economic deficit that will take many years for our economy to recover from

- Several years. More than 2.

- Assuming vaccine available

- It will take time to roll out a vaccine - there will be problems with the roll out. Many things (such as Office Real Estate) will never go back to "normal". Inflation may occur, and may be difficult to control with ongoing unemployment.

- But the strongest businesses will be beneficiaries from the collapse of the weaker businesses.

- We don't yet know how bad the effect will end up being on business and the economy.

- It really depends of the Feds. If they keep points scoring (as they are now doing with Victoria), it will take longer.

- It's going to take a long time for small business to get back on it's feet, and sadly there are a lot of small businesses which aren't going to make it.

- We were already in per capita decline; with reduced migration, that trend will not change. Morrison exudes hubris and arrogance. Scotty from Marketing, of all people, should know Proverbs 16:18, "Pride goeth before destruction, and a haughty spirit before a fall. ... Yea, all of you be subject one to another, and be clothed with humility: for God resisteth the proud, and giveth grace to the humble."

- The underlying damage that’s being done is unknown to me

- I believe it will take some years but difficult to say given the uncertainty of when Victoria a major component of the Australian economy will be able to get moving again.

- Depends on whether and when an effective, safe vaccine can be widely available.

- depends on vaccine

- Depends on whether APRA will allow bank shareholders dividends and how long I need to finance bank provisions for bad debts. Interesting I am supporting renters with rent relief and mortgage holders with provisions. Happy to support my fellow Australians!

- an effective vaccine will cause a dramatic turnaround in activity and give the lie to "recession", This has been caused by a left of field problem not directly relating to business/speculative activity. Note the over subscribing to Govt. bonds. Money desperately looking for activity. Note the nil effect caused by flu epidemics with a vaccine on tap.

- Full effect yet to be felt

- There is no likelihood of a vaccine for at least another year and a half. Therefore we are not likely to see a recovery back to pre-Covid days before two years

- Even if vaccine developed and successful, business will be slow for many reasons. Government intervention will be needed, but constructively and creatively.