In financial markets, 2018 was the year of the Royal Commission. Broadcast live, the hearings became compelling viewing for both market participants and the public, and the worst revelations dominated the news cycle. The Final Report is due on 2 February 2019, and the market awaits with great anticipation.

Banks and large wealth managers are big and ugly and fair game, but like the Westminster political system, they look bad until the alternatives are considered. Do we want to close the loan choices offered by mortgage brokers? Do we want banks to stop offering financial advice to their customers, and instead send them around the corner to an 'independent' adviser? Do we want the banks to reduce lending to small businesses, pushing activity to second-tier and shadow lenders with less regulation and capital. The Commission must note: Be Careful What You Wish For.

Consider what appears on the surface the worst of the behaviours: charging financial advice fees to dead people. How can a dead person receive advice? But financial advisers often have a lot of work to do handling matters for a client’s estate. Are they not supposed to be paid for that? Aren’t the very people in the legal profession who accuse banks of charging scurrilous fees also the people who act for dead clients and charge handsomely for their services? Do accountants turn off the meter when handling the final financial accounts for a dead person? Someone has to manage the affairs of the estate, and many service providers ‘charge fees to dead people’.

In the Cuffelinks editorials, we covered the Royal Commission throughout the year, and we have collected the major events into this summary, from most recent backwards in time.

7 December 2018

The Royal Commission's two defining moments

In his final summary after an exhausting 68 days of public hearings, 134 witnesses and 6,500 exhibits, Commissioner Kenneth Hayne identified one phrase, six words long - "Can I show you a document?" - that had entered the vocabulary over the course of the Commission. It was usually followed by Rowena Orr or Michael Hodge demonstrating an embarrassing mistake.

I consider the two most impactful words of the Commission were dissembling and criminal.

It was Michael Hodge who accused CBA's Marianne Perkovic of dissembling. In Marianne's defence, I thought she had a right to provide context, as most answers are not black or white. Dissembling means 'to conceal or disguise one's true beliefs'. Kenneth Hayne issued a warning:

"We will get along much more quickly and efficiently and if I may put it quite bluntly, it will be safer for you, if you attend to counsel's questions. If you need to stop and think about your answer, take your time."

Safer for you! What did he mean by that serious threat?

Michael Hodge said: "Is the reason why you are dissembling in the way you are dissembling because you are trying to pre-emptively explain why it took more than two years to notify ASIC of this breach?"

Kenneth Hayne later added: "Ms Perkovic, I do not regard that as answering counsel's question. Please ask the question again. I want you to listen to it and I want you to answer it as directly as you can."

Little wonder Marianne completed most of her subsequent evidence with one-word answers. This was in April 2018, near the start of the Commission, and it set the rules. It was a warning to everyone, and the QCs hired by banks stepped up their witness training intensity.

Giving evidence was probably the most intimidating experience in the careers of most of the witnesses. Put this to your 'inverted bucket list' of things you never want to face ...

Similarly, a collective shiver hit witnesses when Hayne asked Nicole Smith, the NULIS/MLC trustee, if she had ever contemplated that:

" ... taking money to which there was no entitlement raised a question of criminal law?"

It was one thing to give evidence that might result in a corporate fine, but Hayne was suggesting financial services staff might go to jail. The Royal Commission had become dangerous.

30 November 2018

Tomorrow is the final day of Royal Commission hearings. We have never seen anything like it before, and most senior bankers hope we never will again. Kenneth Hayne will produce 1,000 pages of censures and recommendations in February 2019 that will change the finance industry.

I misjudged what the Commission could achieve, mainly for three reasons. First, I thought it would be more like a court, where QCs defend their clients and produce contradictory arguments. In fact, we heard no defences from QCs after Kenneth Hayne slapped down NAB's counsel, Neil Young. Hayne wagged his finger at Young and shouted:

"You will not give her her answer, Mr Young. You will not. Do you understand me?"

After that, the bank QCs became almost irrelevant during formal proceedings, as demonstrated in the final round by Peter Collinson, QC for ASIC, who said meekly:

"Can I raise an objection, Commissioner. My friend has put this a number of times. I don't want to help the witness but it's not what the paragraph says."

Rowena Orr simply rephrased the question and continued without missing a beat.

Second, the ability to source internal documents and produce them in hearings without notice generated significant unease and incrimination for witnesses. Context in responses was not allowed. Imagine being accountable for every email or paper written for the last 10 years. There will be a lot more business carried on verbally in coffee shops in future.

Third, the public gallery, saturation media coverage and live television broadcasts placed witnesses in a harsh spotlight that no courtroom or ASIC interrogation could match.

23 November 2018

We tend to overlook the official name of the financial services inquiry. It begins with 'Royal Commission into Misconduct'. Kenneth Hayne and his team are delivering mightily, and although the current round is only meant to "... focus on policy questions from the first six rounds", the fireworks continue to fly.

This week, we heard how Matt Comyn, now CEO of CBA but Head of Retail Bank from 2012 to 2018, tried to convince Ian Narev that CBA should drop some poor insurance protection products. Narev refused, apparently supported by Head of Wealth, Annabel Spring, telling Comyn to "Temper your sense of justice." There's a phrase that will live long after the Commission reports. Comyn said he was frustrated over many years:

Rowena Orr, QC: How do you feel about that comment from the CEO at that time, Mr Comyn?

Matt Comyn: I suspect I was slightly irritated by it.

Consultants at Ernst & Young have since estimated that at least 40% of the 930,000 people who bought consumer credit insurance may deserve compensation.

Comyn admitted CBA often prioritised profit ahead of customer outcomes, and had become deeply complacent with incidents such as the Austrac money-laundering. Then this bombshell:

Rowena Orr: And do you feel that CBA has had the right leaders in the past?

Matt Comyn: No.

Amazingly, in 2016, the then Chief Risk Officer and now Deputy CEO David Cohen, recommended none of the senior executives have their short-term bonuses reduced, despite compliance with risk measures being a 'gate opener' to bonuses. Cohen said the risk criteria were 'fully met'. At the time, CBA was dealing with the CommInsure scandal, anti-money laundering, fees for no service and protection insurance. Narev took the recommendations to the Board, which gave the CEO 108% of his short-term bonus worth $2.9 million. The only executive who received a cut was Annabel Spring, due to the problems in Wealth. Her bonus was cut to 95% of the target.

Current Chair Catherine Livingstone said: "We've all reflected on these outcomes and would regard them as inadequate." She said the Board should have challenged Narev's recommendations and in many cases, given zero bonus. It was also revealed that the Board asked the previous Chair, David Turner, to return 40% of the Board fees from his final year, but he refused. Alan Kohler has calculated that Ian Narev received $44 million during his tenure as CEO.

It's not all serious at the Misconduct Royal Commission

Attending the Royal Commission in person is not like going to a AFL game, which is always better at the ground. It's more like a cricket test match, better experienced on television where the action is head on in full screen detail. From the public gallery, for example, you can't watch the expressions of Rowena Orr and Michael Hodge, and that's half the theatre. When Orr says "I see", pauses and glances down at her notes, witnesses visibly blanch.

I realise you need to be a finance geek to have fun at the Royal Commission, but there were moments of mirth during Comyn's evidence. Your reporter is caught having a laugh above (arrowed). Kenneth Hayne enjoys interjecting in a good verbal joust, such as:

Commissioner (KH): Are there any ongoing services supplied by a mortgage broker, Mr Comyn?

MC: I think they would be limited, Commissioner.

KH: Well, limited or none?

MC: Much closer to none.

KH: I'll take that as 'none'.

There was also a giggle when Livingstone justified hiring internal candidate Comyn by saying:

"To find an external person globally at that level who has not been involved in some regulatory event is almost impossible."

Comyn revealed CBA was about to move to flat fee commissions to mortgage brokers, but stepped back when they realised the other banks would not follow and brokers enjoying up front percentage fees and trails would stop sending business to CBA.

4 October 2018

Royal Commission fallout continues

A consequence of the Royal Commission is a profusion of litigation. On 27 September, law firm Slater and Gordon (S&G) announced that it had filed class action proceedings in the Federal Court against NAB and MLC on behalf of customers sold worthless credit card insurance. S&G is also running a class action against AMP, and investigating whether “CommInsure used obsolete medical definitions and even pressured doctors to change their opinions when assessing claims.”

The second volume of the Commission's Interim Report on detailed case studies is even bigger than the main volume's 115,000 words. Rich pickings for the No-Win No-Fee class action lawsuits, making it a great time to be a lawyer.

Meanwhile, ASIC told Kenneth Hayne that there is a high likelihood of both criminal and civil proceedings commencing soon against the banks over the No-Service Yes-Fees issue.

Two articles published last weekend examine the bank culture and incentives issues in the Interim Report.

14 September 2018

It's not well known that thousands of exhibits presented to the Commission, previously highly confidential internal documents, are now in the public domain. For a finance geek, it's a rich store of once-private material. For example, there's a 2011 Colonial First State document for 'Adviser Use Only' which defines best interests duty on product replacement advice. If only they had followed it. This week, adviser Alex Denham explains how she interprets best interests duty.

At the Commission, it's now the insurance companies being hauled over the coals, and again CBA was a target with CommInsure admitting it engaged in misconduct over medical definitions for life insurance. CBA CEO Matt Comyn will be pleased when these businesses are off his hands.

Sportsbet is accepting bets on 'Which of the Big4 parent bank owned superannuation funds will pay out the most compensation in 2019?'. The current betting for $1 outlay is: CBA $1.65, ANZ$4.00, Westpac $7.00, National $8.00. Not a race where you want to be favourite.

Clearview's Risk Officer, Greg Martin, explained life insurance is a 'grudge' purchase and:

"the life insurance sales process inevitably involves some level of customer disturbance to achieve engagement".

Unfortunately for Clearview, the Corporations Act includes anti-hawking provisions limiting such 'disturbance'. And just when it seemed it couldn't get worse, the Commission heard a tape of Freedom Insurance pressuring a young man with Down syndrome to buy insurance. Over $6 billion in commissions was paid to financial advisers by 10 life insurers in the last five years.

7 September 2018

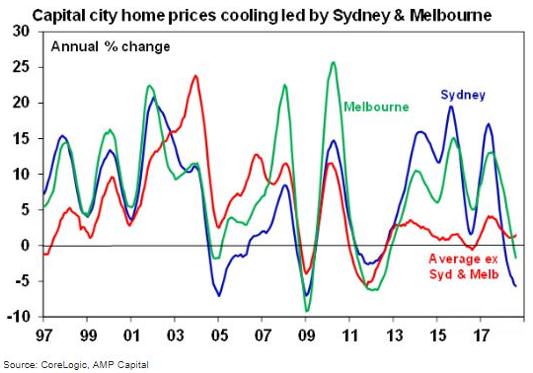

The Royal Commission has already had a profound impact on the residential property market, especially the stress testing on capacity to pay. A reader in our 'Have Your Say' section said his banker told him that 40% of applications that would previously have been approved are now "dead in the water".

It's a cautionary warning for anyone buying property to line up financing well in advance, especially when tests for older people are even stricter. The self-employed will need three years of tax returns, PAYG earners will have expenses examined like never before, and loan rates of 7% or more are assumed to check affordability.

CoreLogic reports Sydney and Melbourne comprise 60% of the Australian housing market by value, with Sydney down 5.6% and Melbourne down 1.7% in the last year. Top end homes are falling the most, with the bottom quarter by value still flat or rising.

31 August 2018

Royal Commission push back

The Commission has firmly placed the superannuation industry, especially retail funds, on the defensive, and the 200-page Closing Submission issued last Friday highlights potential criminal charges. But in a rare legal counter, Allens lawyers has issued some opposing opinions:

"When we went to law school, we were told that before someone could be found to breach a duty of care, the standard of care required had to be identified. In the case of superannuation trustees, it is the standard of a prudent superannuation trustee. The submissions do not say anything about what that standard means. They appear to be saying that whatever it means, the relevant trustees may not have satisfied it ... Contrary to what Counsel Assisting appear to be implying, the facts do not speak for themselves."

The Royal Commission and regulators will have a far-from-clear run through criminal proceedings. Furthermore, new Prime Minister Scott Morrison abolished the cabinet portfolio position of Revenue and Financial Services, rolling it into Treasury, but Josh Frydenberg will have more things to worry about than new superannuation regulations.

24 August 2018

Don Argus was Chief Executive of National Australia Bank from 1990 to 1999, a period of growth and rising share prices after the 1991 recession. In the Royal Commission's 10 days on superannuation, NAB was in the witness box an amazing five days. Banks such as Westpac and Macquarie did not appear at all. What did Argus tell The Australian about the evidence he had seen?

"There is a need for basic tenets of honesty, integrity and accountability. Regulations without a spirit of morality do not work ... Having a dense legalised disclosure statement for consumers to read, so organisations can protect themselves, is not the answer."

The worry is that Commissioner Hayne and regulators will stifle business and innovation in response to the poor behaviour, especially when added to the plans to embed regulators within major institutions. There is no doubt the Royal Commission will sharpen up some lazy boards and better principles of governance will be introduced, but regulation is not the only response needed.

Graeme Samuel was President of the National Competition Council in 2000, and he said:

"I defy the best legal minds to produce a set of rules that will compensate for negligence, ignorance, apathy or the many characteristics that will render a board of directors dysfunctional. No process of box ticking will overcome fundamental dysfunctionality of a board of directors."

We have collected examples from two weeks on superannuation at the Royal Commission using dialogue from the witness box to allow readers to consider the evidence.

17 August 2018

There's no doubt the Royal Commission has decided that super fund trustees are "hopelessly conflicted" when they are also executives of the entity running the fund. The Commission's Senior Counsel Assisting, Michael Hodge, has asked the same question on member best interests a hundred different ways.

To NAB's Nicole Smith: "Do you agree that if a member is not paying a commission, the member is in a better position than if the member is paying a commission?" To ANZ's Victoria Weekes: "Would it be possible for the board to approve the successor fund transfer [to IOOF] without being satisfied ... the members' best interests would be served?" To Colonial First State's Linda Elkins: "How was it in the interests of the members of the fund to grandfather commissions when going from superannuation to pension?"

Ms Elkins was Executive General Manager of Colonial First State and a Director of the trustee company at the same time, and she was meeting Treasury officials on grandfathering commissions. She replied to Hodge: "In hindsight, I would agree that it's not and we, you know, shouldn't have been lobbying for that."

At least she didn't circumlocute like other witnesses. Such an intractable conflict may lead to a banning of the commissions retained from pre-FOFA and a requirement for independent trustees. Many advisers and super funds simply will not switch clients to better products while they retain commissions on old, lower quality funds. As Michael Hodge said of the sale of ANZ's wealth assets: "The view seems to be that if commissions are not grandfathered then the adviser network will not support the super fund or the sale."

It has also been fascinating how often the excuse 'super is a scale business' is used to justify actions, from maintaining commissions to keep funds viable, to paying $2 million to support an online newspaper, to corporate entertaining and football sponsorship.

This week, Bernard Kellerman describes the conflicts of interest in the $1 billion sale of OnePath to IOOF, and Carden Calder and Gigi Shaw look at how executives have responded to the Royal Commission with complexity and opacity and they suggest ways out of the darkness.

Commissioner Kenneth Hayne has much more to examine on superannuation after almost two weeks focussing mainly on trustee duties, and he's likely to ask for an extension in September. We will provide a summary of Round 5 in next week's edition.

10 August 2018

Okay, we get it, please move on. The Royal Commission is doing great work uncovering poor practices in financial services, but after nearly three days on superannuation, it had interviewed only one company. The witness list has 16 entities on it. We already know from Round 2 in April that there is a systematic problem with advice fees. I have listened to a dozen hours of the Commission this week and we have run around in circles with two MLC/NAB witnesses, and one has returned for more questions today on Day 4.

It started well. Counsel Assisting, Michael Hodge QC, summarised the trustee problem in his opening address:

"Trustees are surrounded by temptation, to preference the interests of the sponsoring organisations, to act in the interests of other parts of the corporate group, to choose profits over the interests of members, to establish structures that consign to others the responsibility for the fund and thereby relieve the trustee of visibility of anything that might be troubling. Their duties require them to resist all of these temptations ... What happens when we leave these trustees alone in the dark with our money? Can they be trusted to do the right thing?"

The Royal Commission will issue an Interim Report by 30 September, only six weeks from now. There's so much else it should address: performance reporting, fee calculations, rates paid on cash, valuations of unlisted assets, definition of 'defensive' assets (credit, property, alternatives), performance fees, active managers hugging the index, risk versus return, bid/offer prices, etc. And what about the dubious banking practices which have changed little in the 20 years since I wrote Naked Among Cannibals?

These issues will have more long-term impact on the vast majority of customer returns than charging fees for no advice or to dead people. I hope the Commission does not run out of time.

15 June 2018

Two significant events last week show the fallout from the Financial Services Royal Commission will go far beyond the banks and big companies like AMP.

The closure of financial planning firm Dover Financial means at least 30,000 clients are without an adviser during the most critical few weeks of the financial year. A friend who provided services to Dover says most of the 450 advisers are quality operators who now cannot give new advice. ASIC has warned licensees to do extra checks and obtain audit reports and references before hiring ex-Dover advisers.

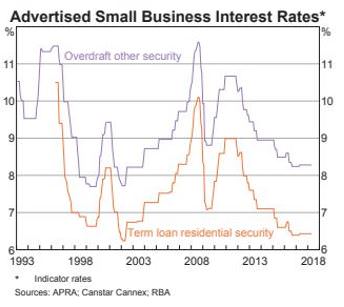

Prospa is the type of fintech that is supposed to prosper from tighter bank lending conditions to SMEs, but the company canned its IPO at the last minute. ASIC is demanding all lenders review their Unfair Contract Terms, and deep inside Prospa's now defunct prospectus is this:

Page 44, footnote 11 on their Annual Percentage Rate (APR): "We use a factor rate in our pricing discussions with customers because we believe the total interest dollar cost and the total payback of the loan is (sic) the most relevant to our customers ... At 31 December 2017, the weighted average APR (on a gross loan basis) of our portfolio was 41.3%." That's not a typo, it says 41.3%.

Page 123, in the Business Risks section: "Prospa may change the way it explains the cost of its financing products due to regulatory changes ... This may include being required to disclose the Annual Percentage Rate or a similar standardised rate. Such changes in Prospa's loan contracts or other documentation may have a materially adverse effect on the perception of distributors or borrowers of the cost of Prospa's products relative to other financial products which may have a material adverse effect on Prospa's business, financial condition, operating and financial performance and/or growth."

So disclosing the APR may have a materially adverse effect on the business. Indeed, it would be cheaper to borrow using a credit card. Prospa was 15 minutes away from floating with a market value of $576.3 million. Here's what the RBA says are the average advertised SME indicator rates.

4 May 2018

Just when AMP was taking the brunt of the Royal Commission's criticisms and the banks were welcoming a scapegoat, APRA's Prudential Inquiry issued a stinging assessment of the Commonwealth Bank. If the new CEO, Matt Comyn, wanted a catalyst for change, he now has it in spades. The Treasurer, Scott Morrison, jumped on it:

"The Report, I think, is required reading not only for every institution in the country but, frankly, it should be the next item on the agenda of every single board meeting in this country regardless of whether you're a bank or not."

The Report said CBA's financial success had dulled its senses to a deterioration in the risk profile, especially non-financial risks:

"These risks were neither clearly understood nor owned, the frameworks for managing them were cumbersome and incomplete, and senior leadership was slow to recognise, and address, emerging threats to CBA's reputation." (page 3)

A strange feature of the APRA Report is the repeated identification of executives as 'previous', 'former' and 'new' without naming them. Current staff are generally not blamed for the systemic failures. For example, the Report says:

"There was some evidence at the BRC [Board Risk Committee] that the reputation of the previous Chair of the BRC and CRO as industry experts with a 'scholarly gravitas' stifled the level of challenge at Committee meetings." (page 18)

The previous Chair of the BRC was Harrison Young (who left the Board in November 2017 at the same time as Laura Inman) and previous Chief Risk Officer was Alden Toevs, who left CBA in 2016. Chief Financial Officer David Craig retired in 2017.

APRA's Report is an indictment on the culture created under former CEO, Ian Narev, and former Chair, David Turner. In the Culture and Leadership section, it says:

"Executive Committee members commonly described the 'socratic' questioning style set by the previous CEO leading to some 'decisions being driven by the best debater rather than the person with the most robust position.'" (page 88)

Indeed, how many times have we all seen that? The King is dead, long live the King.

Many more Royal Commission seasons to come

The daily broadcast of the Royal Commission is taking a break, and it feels like the end of the football season or completion of binge-watching a series of Fargo. Bring on Season 3. We've seen the removal of villains (taking their booty with them), fainting and ambulances, gold medal performers and shredding of reputations. It's rare to hear a CEO called out in public for lying, as Mark Costello did to Dover's Terry McMaster:

"That's a lie, isn't it? I put it to you it is Orwellian to describe this as a Client Protection Policy. The entire intention of this document is to minimise Dover's liability for the work of its authorised representatives."

And soon after, Terry McMaster collapsed, topping two weeks of high drama.

There has also been much focus on AMP amending the so-called independent report by Clayton Utz. Consultants or regulators commonly offer an opportunity to comment on a draft report, but this is now likely to change. The main issue here is not so much the amending of the report, but passing it off as an independent third party assessment.

The Royal Commission may also be causing a further tightening of mortgage lending conditions. The latest CoreLogic Home Value Index shows combined capital city values had the first annual decline since 2012, although Hobart continue to shine.

20 April 2018

Mea culpa, it's worse than I expected. In August 2016, I wrote 10 reasons why a Financial Services Royal Commission was not necessary, but Kenneth Hayne and his team have taken discovery of malfeasance to a new level. Among other factors, I thought actions by ASIC and various reviews would uncover wrongdoings and lead to change, but a sledgehammer was required to break through to the facts. The consequences will be far-reaching for wealth management.

The Royal Commission is gripping viewing. I'm watching hours of it each day, not knowing whether to laugh or cry. The commercial channels should bid for the broadcasting rights over winter. It has everything: the forensic analysis and youthful confidence of bright QCs assisting the grumpy Commissioner; the hapless and bemused witnesses left out to dry by their superiors; and a script worthy of John le Carre with lies, deceit and incompetence.

So many lowlights. AMP giving 20 misleading statements to its regulator. The head of the financial advice business saying he had not "turned my mind" to thinking about adviser commissions. Charging financial advice fees but not meeting the client, with the Commission calling CBA the "Gold Medallist" in fee-for-no-service. An external "independent" board report for ASIC revised by AMP management through 25 drafts, including redacting the CEO's name. An executive unable to identify what he was apologising for. Using the ACCC acronym for the Advice, Culture & Compliance Committee. Counsel accusing a CBA witness of "dissembling" and "misleading". Really, you couldn't invent this stuff, and what a setback for vertical integration and financial advice!

The transcripts of witness interviews are here. Your comments on the Royal Commission are welcome on our website.

16 March 2018

Watching the Royal Commission live is as painfully engrossing as a slow motion train wreck. Banks breaching responsible lending rules was a common theme this week, with a failure to check borrower details, fraudulent conduct, reliance on false documents, ineffective monitoring, conflicts of interest, bribery, even paying gymnasiums and tailors to introduce loans. Remediation for bad consumer lending has reached $700 million.

The Commission revealed about 56% of mortgage loans originate through brokers, and therefore the banks have outsourced many checks and processes on their largest asset type (in the case of CBA, 64% of total lending). An unbelievable 90% of car purchases are financed with loans, often through the dealership. People are buying a depreciating asset with useless add-on insurance at high interest rates, and many will never pay off their debts for the sake of owning a fancy car.

The case studies show the Royal Commission will be a public relations disaster for the banks. It's hard to listen to the Commission and not expect the bank behaviour to be punished by the market, but it's easy to see why the legal fees will exceed $1 billion.

Graham Hand is Managing Editor of Cuffelinks.