The largest Australian and global asset managers are reporting their results for last year, and they are useful benchmarks for all retail and institutional investors. While everyone has different goals and strategies, there is some reassurance for the novice investor that even the most sophisticated managers are struggling in the current market.

This article looks at the results from CalPERS released this week, Warren Buffett’s Berkshire Hathaway in 2015, and Australia’s superannuation funds in the past financial year.

California Public Employees’ Retirement System (CalPERS)

CalPERS is the largest defined-benefit public pension scheme in the United States, managing over US$300 billion on behalf of millions of Californian school and public service members.

This week it reported an annual return of 0.61% net of fees for the year to 30 June 2016. Far from being embarrassed about the result, Chief Investment Officer Ted Eliopoulos said, “Positive performance in a year of turbulent financial markets is an accomplishment we are proud of.”

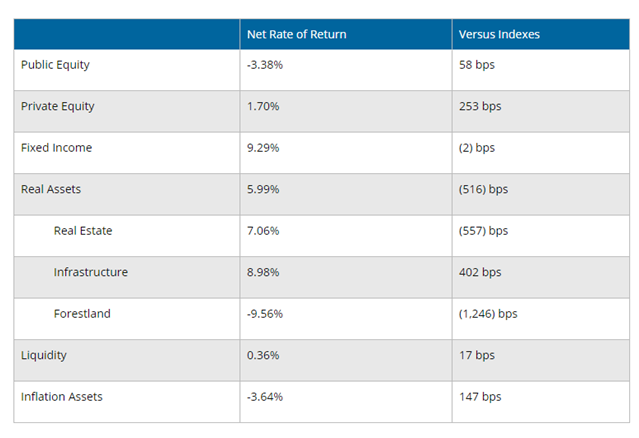

CalPERS splits its performance into asset classes as shown in Table 1.

Table 1: Asset class performance by CalPERS in year to 30 June 2016

Returns are heavily dependent on the performance of listed companies, since half their portfolio is in equities, but they point to the merit of diversification. The poor equity result was offset by strong fixed income, real estate and infrastructure returns, largely driven by declining interest rates. Unfortunately, these rate gains will be difficult to repeat.

As expected from such a massive fund, its processes are supported by a detailed Asset Liability Management system, described here. It covers asset allocation, demographic change, actuarial assumptions and estimates of the overall soundness of their defined-benefit plans. The assumptions were last reviewed in 2014. This might explain why they continue to assume strong rates of return, as shown by their statement on common misconceptions:

“Myth: CalPERS 7.5% assumed annual rate of investment return is too high and cannot be achieved: CalPERS investments have earned an average 7.6% annual return over the past 20 years and 9.4% over the past 30 years. CalPERS investments earned 13.2% in Fiscal Year 2012-13. CalPERS assumed rate of investment return is a long-term [20 years or more] average. Any given year is likely to be higher or lower than the assumed rate.”

Not only are they quoting returns from another world in 2012/2013, but their more recent commentary talks about the current challenging conditions. Eliopoulos will struggle to explain in his next review of assumptions how he can average 7.5% in the coming decade.

Berkshire Hathaway

Warren Buffett’s annual letter to shareholders contains the usual gems, and he dispels the negative ‘drumbeat’ about his country’s problems:

“The babies born in America today are the luckiest crop in history ... For 240 years it’s been a terrible mistake to bet against America, and now is no time to start. America’s golden goose of commerce and innovation will continue to lay more and larger eggs. America’s social security promises will be honoured and perhaps made more generous. And, yes, America’s kids will live far better than their parents did.”

(As an aside, the millions of babies and kids whose parents earn the minimum wage of US$7.25 an hour will struggle to appreciate how lucky they are unless someone funds their college education).

Buffett reports his performance in many ways, including per-share book value (up 6.4% in 2015 versus a long-term average since 1965 of 19.2% pa) and per-share market value (down 12.5% in 2015 versus up 20.8% pa since 1965). He discusses intrinsic value at length, including earnings from Berkshire’s businesses increasing by 2.1% in 2015 versus 23.7% pa since 1970. In 2015, the S&P500 rose by only 1.4% including dividends.

So while Buffett continues to demonstrate outstanding investment acumen and long-term optimism, the recent performance is a far cry from historical levels, any way the results are measured. There are many reasons for this, not least the fact that his company is now valued at about US$330 billion. Small investments do not move the needle.

Obviously his short-term performance is affected by market forces, but he considers the major risks for his companies are:

- The railroad business is certain to lose significant coal volume over the next decade.

- At some point in the future, his insurance and auto dealership companies may shrink because of driverless cars.

- Circulation of his print newspapers will continue to fall.

- Renewables have previously helped his utility operations but this could change, particularly if storage capabilities for electricity materially improve.

- Online retailing threatens the business model of his retailers and certain consumer brands.

But he is not concerned about year-to-year vagaries of the stock exchange:

“These potentialities are just a few of the negative possibilities facing us – but even the most casual follower of business news has long been aware of them. None of these problems, however, is crucial to Berkshire’s long-term well-being.”

If only all company executives and investors could think with such a long-term horizon.

Australian superannuation industry funds

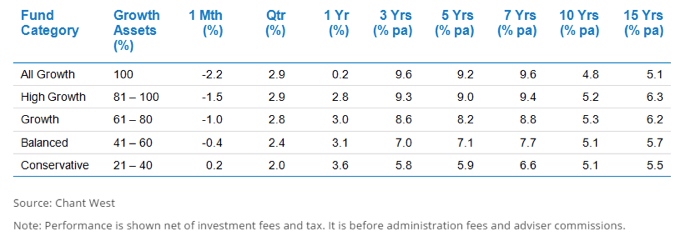

The median industry superannuation fund returned 3% in the year to 30 June 2016, the lowest annual level in four years, according to superannuation researcher Chant West. The median returned 6.2% pa over the past 15 years. These numbers apply for the Growth category (see Table 2 below) used by the majority of Australians, where 61% to 80% of investments are allocated to 'growth' assets.

Table 2: Diversified fund performance (results to 30 June 2016)

Warren Chant described the benefits of diversification enjoyed by the best performers (the top fund was up 7.6%), as Australian equities returned less than 1%. Strong returns came from listed property (up 24.6%), unlisted infrastructure (up 17.9%), global fixed interest (up 9.3%) and domestic fixed interest (up 7%).

“While this year’s return is significantly lower than the previous three years (15.6% in 2012/13, 12.8% in 2013/14 and 9.8% in 2014/15), members shouldn't be too disappointed with the result given that super funds are faced with a very uncertain global political and economic environment. They’ve had a particularly good run since the end of the GFC.”

The major lessons from experienced investors

Three messages from professional investors are: think long term, accept lower returns in the current market, and diversify exposure.

The biggest challenge facing all investors, and especially the less-experienced, is to focus on a long-term strategy and not blink every time the market has a correction. Buffett has such faith in the long-term robustness of his businesses that he sees market falls as buying opportunities (during the GFC, he bought options expiring in 2021 with the right to acquire 700 million Bank of America shares for US$5 billion which are now worth US$12 billion). CalPERS may be optimistic in expecting a 7.6% return in coming years but they remain unfazed by a poor year.

Where Australian industry super funds have gained an edge is holding a decent allocation, around 20%, in unlisted assets such as private equity, infrastructure and property. These ‘alternative’ assets are available to most retail investors, either through unlisted syndicates, listed investment companies, exchange traded funds or managed funds.

Notwithstanding the benefits of diversification supported by recent experience, it is difficult to see the strong performance of fixed interest being repeated in coming years, and it could be negative as rates rise. Equities are fully valued and property has had a stellar run. While 'lower for longer' has become the common cliche, the last year has shown there are market opportunities for those who are canny at asset allocation.

Graham Hand is Editor of Cuffelinks. This article is general information and does not consider the needs of any individual.