The Weekend Edition includes a market update plus Morningstar adds links to two of its most popular stock pick articles from the week.

Weekend market update

AAP Netdesk: On Friday, iron ore miners plunged with Fortescue Metals the chief victim, down 11% after the price of the steel-making material fell as low as $US107 per tonne. Rio Tinto lost more than 4% and BHP shed over 3%. UBS analysts said a weak Chinese property market was lessening the need for more steel. Elsewhere on the Australian market, shares in energy and utilities had notable falls and the benchmark S&P/ASX200 index closed lower by 57 points, or 0.8%, to 7,404. After 11 consecutive months of gains, the ASX200 is down 1.7% in September so far.

Among the big four banks on Friday, NAB had the steepest loss and shed 1.1% to $27.89. The Commonwealth was little changed at $102.88. Technology was the best performing category and higher by more than 2%.

Shane Oliver, AMP Capital: Global shares mostly fell over the last week on growth concerns. US shares fell -0.6% (mainly due to Friday when both the S&P500 and NASDAQ lost 0.9%), Eurozone shares lost -0.9% and Chinese shares fell -3.1% with concerns about the Evergrande Group also weighing.

How worried should Australia be about the 50% plunge in iron ore prices (Australia’s largest export)? Basically, alert but not alarmed. Bear in mind that the iron ore price has fallen from levels no one ever thought it would get to and is still very high and well above cost. This will dent Australia’s national income and current account surplus and add a new blow out in the Federal Budget deficit (which along with lockdown support payments may end up closer to $150 billion this year than the $107 billion in the May Budget). But against this most other commodity prices are surging, including coal and gas (our second and fourth largest exports), aluminium and copper. In fact, there is good reason to believe a new commodity super cycle (ex iron ore) has begun, which should benefit Australia.

***

If you were on the board of a major bank and asked to write a wishlist of things the government or central bank could fix to help your business, almost everything you could dream up has been delivered. For many years, I was Head of Balance Sheet Management at a large bank and we thought we were responsible for solving our problems and managing our own risks.

Here's a brief list of aids handed to the banks, their executives and their shareholders in the last year:

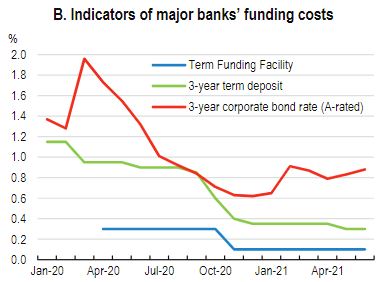

* Provide a three-year Term Funding Facility (TFF) for $200 billion at a cost of only 0.1%.

* Reduce the cash rate to 0.1% to create massive demand for our largest asset class, home lending, and push up prices to make our security more valuable.

* Purchase hundreds of billions of bonds and securities to ensure plentiful liquidity and allow us to hold higher-yielding securities.

* Give some of our customers access to their superannuation since we are no longer focussed on that troublesome business.

* Pay $90 billion in JobKeeper to businesses with no check required on whether the policy retained jobs or company turnover actually fell.

* Introduce an SME Guarantee Scheme to improve access to business credit and a Boosting Cash Flow for Employers Scheme.

* Adopt a HomeBuilder programme of $25,000 grants to first-home buyers even if the money ends up in the hands of land developers.

* Allow business tax relief and full expensing of eligible assets.

* Relaxation of the responsible lending laws, contrary to the findings of the Financial Services Royal Commission.

Yes, spending was required in a pandemic but billions of dollars found their way into small and large businesses which did not need support, funded by government debt. And now banks can reward their shareholders with healthy dividends and strong balance sheets and Australia is left with structural budget deficits for decades and a trillion dollars of net debt.

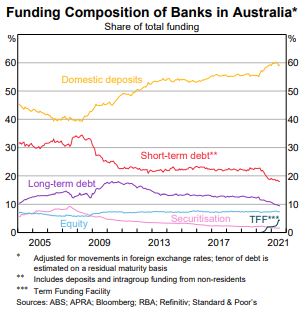

The TFF is not discussed as much as other programmes but for someone who spent years raising term debt to manage the asset/liability mix, it is a ripper. Combined with a surge in domestic deposits, now contributing 60% of bank funding, the banks have their smallest reliance ever on their most vulnerable source, short-term wholesale debt, as shown below.

The table below from the OECD shows how cheap the TFF is compared with alternative term funding sources.

Source: OECD Economic Survey, Australia, September 2021.

Source: OECD Economic Survey, Australia, September 2021.

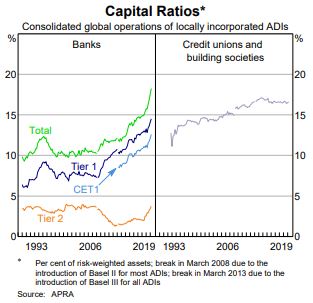

To complete the rosy balance sheet picture, the strong capital ratios make our banks rock solid. Hybrids, anyone?

The TFF allowed the banks to compete aggressively for mortgages, especially with the introduction of attractive fixed rates. The big banks in particular benefitted with CBA drawing $51 billion, NAB $32 billion, Westpac $30 billion, ANZ $20 billion and Macquarie $11 billion.

CBA! The best-funded bank in Australia eagerly accepting $51 billion for three years at 0.1%. In my day as Head of New Issues at CBA, we toured the world looking for term funding. No wonder CBA's net interest margins have improved, and Macquarie Equities estimates CBA's revenue benefit at $384 million from the TFF alone. And contrary to the intentions of the TFF to help to fund SMEs, the vast majority of the money went into residential mortgages.

In a week when the Reserve Bank Governor, Philip Lowe, said surging house prices are not on his agenda but to look more at factors such as the social security system, and the OECD called out Australia for policies favouring home investing, we focus on the age pension asset test. The OECD said:

"the prolonged boom in house prices have inflated the wealth of many pensioners without impacting their pension eligibility ... the distribution of age pension expenditures is much less skewed to lower wealth quintiles than other payments."

Has the time come to address paying age pensions to owners with homes valued above a high threshold point, in the interests of equity and fiscal responsibility? We value your feedback in our survey after checking the argument. We have already had a terrific 1,300 responses and hundreds of comments and we will leave the survey open until late Monday then full results next week.

We interview Sean Fenton of Sage Capital, recently nominated for the Rising Star fund manager award by Zenith, on how he balances the need for income and capital growth, the investment themes he likes and shorting in a rising market among other portfolio solutions.

Welcome back Chris Cuffe, co-founder of this publication nine years ago, with a warning from him that the new Design and Distribution Obligations (DDO) coming on 5 October will lead to fund closures and changes in the way banks sell securities, and direct more business directed towards listed offers.

Then David Wilson identifies the FY21 company winners and losers including stocks in his portfolio that he is especially pleased with ... and a few less so.

Warren Bird checks the latest 'Down Down' at Coles and it's not the status quo we learned to hate. What was once the domain of fund managers is now coming into companies, but is it genuine or spin?

And with Managed Account balancing surging through $100 billion, matching the higher-profile growth of ETFs, Toby Potter explains why they are growing quickly and changing how financial advisers work.

In the latest Wealth of Experience podcast with Peter Warnes, he checks Stockland, Scentre, Qantas and Flight Centre, we discuss what 12-month highs and lows reveal, asset allocations, a couple of grumps plus the full interview with Sean Fenton.

Two bonus articles from Morningstar for the weekend as selected by Editorial Manager Emma Rapaport.

Nathan Zaia continues Morningstar's reporting season roundup with his take on the big four banks, eye-popping payouts and sector-wide margin pressure. And Emma asks, what are the best global equity ETFs on the ASX?

This week's White Paper from Spheria Asset Management (part of the Pinnacle group, a new Firstlinks sponsor) looks at opportunities in global small caps and why they can offer diversity not available in Australia.

Finally, our Comment of the Week comes from Stephen:

"What we are doing as a country is loading up the next generation with a huge debt, and not caring about it. The next generation don't even care about it themselves, maybe because nobody has pointed it out to them. It is all about fiscal responsibility. Financial planners are acutely aware of fiscal responsibility and planning for the future. It is our job every day. Unfortunately when it comes to public finances it seems there is no such thing."

Graham Hand, Managing Editor

Latest updates

PDF version of Firstlinks Newsletter

IAM Capital Markets' Weekly Market Insight

ASX Listed Bond and Hybrid rate sheet from NAB/nabtrade

Indicative Listed Investment Company (LIC) NTA Report from Bell Potter

Monthly Funds Report from Chi-X

Plus updates and announcements on the Sponsor Noticeboard on our website