Earlier this week Morningstar analysts took the unusual step of downgrading the Morningstar Moat Rating on seven US listed and four Australian listed software shares. The moat rating signifies the ability of a company to hold competitors at bay through a sustainable competitive advantage. The reason for the downgrades – the threat of AI.

Technological advancements are the great unknown and throughout history they’ve upended long established competitive environments. The rapid pace of AI advancement has made the future for software companies less clear and this opacity has led our analysts to reassess their view on the continued dominance of long-established industry leaders.

A murky future and the resulting uncertainty has investors on edge and the impact is likely to persist far after the current concerns about the war against Iran are resolved.

AI's impact will be bigger than the personal computer

I graduated from university in 2001 and the computer and the internet have always been part of my work experience. It is hard for me to imagine work or a world without a computer and the internet.

Yet according to Joseph Davis, the global chief economist at Vanguard, the impact of AI will be far more profound than the personal computer and the internet. Davis acknowledges that isn’t the consensus view but believes most economists are being too conservate about the impact of AI.

“Our findings suggest that the continuation of the status quo, the basic expectation of most economists, is actually the least likely outcome,” Davis says. “We project that AI will have an even greater effect on productivity than the personal computer did. And we project that a scenario where AI transforms the economy is far more likely than one where AI disappoints.”

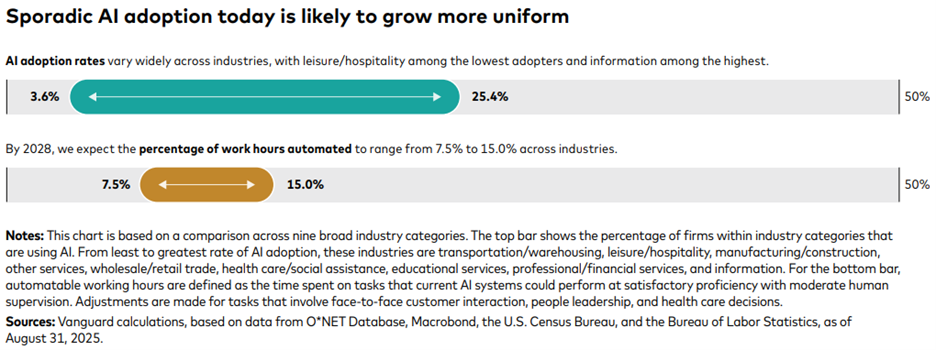

For all the attention that has been paid to AI since ChatGPT emerged in late 2022 Davis and the team and Vanguard believe AI is still early in the adoption and investment lifecycle. Vanguard believes that many industries are still ignoring AI and the percentage of work hours available for automation will double by 2028.

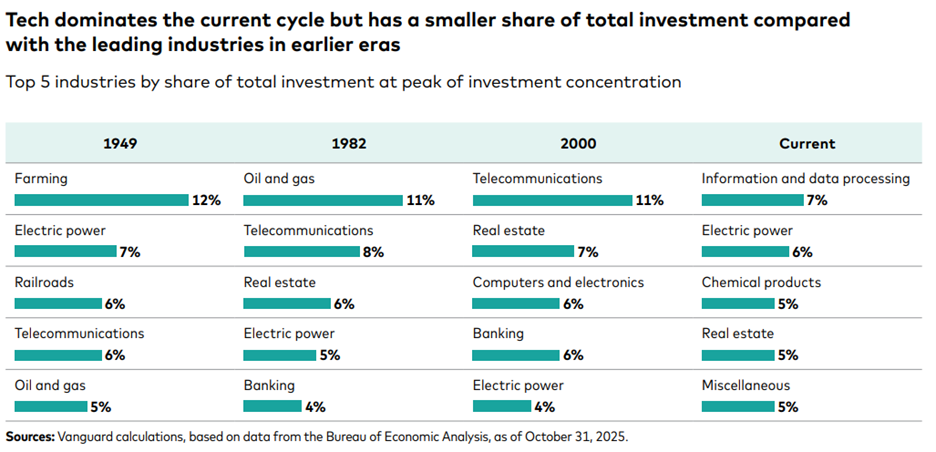

The increased adoption will be driven by continued investment. While the headline spend on the AI buildout is shocking, Vanguard provides historical context. Davis’ team compared the current share of total investment with other eras in the United States and found that there is more room to run for AI infrastructure spend.

What does this mean for investors?

For all the self-congratulatory chatter about changing the world, much of the innovation coming out of Silicon Valley lately didn’t meaningfully contribute to overall economic productivity. Social media, Uber and Netflix may have made our lives easier and made a lot of money for shareholders but that doesn’t mean the technology was economically transformative.

AI could be a very different story. Vanguard has deemed it a general-purpose technology. General purpose technologies like electricity or the railroads transform the entire economy – often with a significant amount of disruption to existing businesses and workforces. The disruption has gotten a good deal of press with proclamations of a ‘white-collar job apocalypse.’

What hasn’t gotten a lot of attention is the potential for widespread productivity improvements as AI adoption increases. The tech giants need this to happen to justify their spending and there will be continued debate about the extent of AI monetisation.

But if this general-purpose technology improves productivity maybe the real winners will be the boring companies who use AI to drive down costs. The beneficiary from the heavy spending on building out railroad networks was not the railroads themselves – it was the shippers. Same with electricity and fibre optic networks.

If the rate of adoption continues to expand, Vanguard believes many of the winners will be in more value-oriented sectors where efficiency gains will lead to higher earnings. These sectors include industrials, financials and select consumer segments.

Final thoughts

Once an emerging trend becomes universally accepted investors typically stick to linear thinking. It takes little intellectual horsepower, and it works as investors salivate at the prospects of limitless growth. Many of these investors – especially the ones that get in late – get burned.

Some investors will be able to pick out the winners in tech. By luck or skill, they will identify which of the mega-tech firms’ AI investments will pay off. They will pluck through the carnage of the software shares and find the companies who will withstand the competitive turbulence and continue to thrive. More power to them.

Given my situation I’m content to keep owning companies unlikely to be disrupted, but sure to benefit, from widespread AI adoption. I’m willing to trade lower upside for more safety. You may make a different decision. That is the crux of investing – a series of trade-offs that each of us has to make given our goals and circumstances.

For those interested in the full Vanguard report you can find it here.

Mark LaMonica

In this week's edition...

John Abernethy takes a sobering look at where Australia went wrong and what to do about it.

Noel Whittaker knows retirement planning is about far more than dollars and cents. He explains why the key to happiness in retirement is figuring out where you live.

Dark premonitions of mass white collar job losses fill the media. Nick Maggiulli has some suggestions to stand-out in the age of commoditized knowledge.

In honour of International Women’s Day, Annika Bradley has a simple solution to a set of challenges disproportionately facing women but also prevalent in the population as a whole – more financial advice.

Tony Dillon is back with a topic slightly less fun than the AFL. As inflation continues to creep higher and more economists forecast rate increases, Tony takes a look at the role energy policy plays on productivity and inflation.

The story has been the same for markets for years – US outperformance. Before Iran, a rotation was already underway as tech pulled back and other opportunities emerged. Franciso de Juan makes a compelling case for European small-caps.

One positive development for investors is the widespread acknowledgement that behavioural drivers impact decision making. Joe Wiggins explores at how individual behavioural drivers interact to create powerful feedback loops.

This week's white paper comes from Capital Group on China shifting its attention towards humanoid robotics as the next frontier for technological leadership.

Curated by Mark Lamonica and Leisa Bell

***

Weekend market update

Two articles from Morningstar this week. I took look at the rotation going on in global markets and considered if a strategy targeting 'boring' shares was an antidote to overvalued markets. My colleague Sim looked at the ramifications if property prices fall.

From Shane Oliver, AMP:

Global markets had a volatile week as the War with Iran continued with the Strait of Hormuz remaining effectively closed. Consequently, oil prices rose further, despite comments from President Trump earlier in the week that the war would soon be over. This in turn pushed bond yields up sharply on expectations for higher inflation and kept share markets under downwards pressure. For the week US shares fell 1.6%, Eurozone shares fell 0.1% and Japanese shares fell 3.2%, but Chinese shares rose 0.2%. Reflecting the worries about a boost to inflation and a hit to growth, ie stagflation, along with increased expectations for another RBA rate hike in the week ahead, the Australian share market fell another 2.6% with energy shares up but all other sectors down led by IT, health, property and materials. From this year’s highs US shares are down 5%, Eurozone shares are down 7%, Japanese shares are down 8.5% and Australian shares are down 6%.

Gold fell slightly further over the last week – which is odd given the surge in geopolitical and inflation risk but could be a case of buy on the rumour and sell on the fact as a lot had already been factored into its price as it roughly doubled over the 12 months to its January high. By contrast Bitcoin continued to rise. Iron ore prices rose but metal prices fell. The $A fell slightly as the $US rose but it remains relatively resilient reflecting ongoing expectations for the RBA to hike rates this year and the Fed to cut, and it has remained strong on a trade weighted basis.

The past week highlighted the limits to TACO as the war with Iran continues and the Strait of Hormuz remains effectively closed. When markets started to panic on Monday with oil surging to $US119 a barrel and shares plunging Trump panicked too (surely, he must have expected the oil surge!) and declared that the War could be over “very soon” and that oil prices would plunge when it was. So, oil prices plunged and shares rebounded thinking a TACO (ie Trump chickening out) was here or near and that the crisis would soon be over. Unfortunately, oil has headed back up again and shares remain under pressure as its clear that the War has a way to go yet with Iran remaining defiant, attacking more energy infrastructure and ships in the Persian Gulf and Strait of Hormuz and warning of oil going to $US200 a barrel. So, Trump has no easy off ramp.

The bottom line is that TACO can work well when Trump has full control – like he did in relation to the tariffs last year. But that’s not the case right now with Iran refusing to play ball. In fact, it wants to see Trump pay a big economic and political cost and the best way to do this is to keep the Strait of Hormuz effectively closed to shipping. That is taking out around 15 million barrels a day of global oil supplies (which is around 15% and its similar or more for gas). And the longer the Strait stays effectively closed the more oil prices will trend up as inventories run down. Don’t forget the second oil crisis in 1979 on the back of the Iranian revolution saw a threefold rise in world oil prices but that only involved a hit to 5% of global oil supplies.

In the absence of securing the Strait of Hormuz most policy options to stop oil prices rising are band aid solutions. The release 400 million barrels of oil by IEA member countries, of which 172 million will come from the US, is to be welcomed. But it will only be released gradually and if its anything like the US release over 120 days it will at best only amount to 3.3 million barrels a day which will only cover 20% or so of the 15 million barrels a day of lost supply from the Persian Gulf. Easing sanctions on Russia would help but that might provide only another 1.5 million barrels a day, and that comes with all sorts of issues given its war with Ukraine. Trump has indicated the US can provide insurance and naval escorts for ships through the Strait but that was over a week ago and both ideas have huge challenges. The US Energy Secretary said the US Navy could start escorting tankers by the end of March..but that is still a few weeks away and sounds very iffy (like his claim that it had already escorted a ship). So the bottom line is that regardless of what Trump says the War likely has a way to go yet.

That said, Trump is under big political pressure to keep the conflict short and avoid troops on the ground and Iran’s military capability is being rapidly degraded. And while Iran will want to keep the Strait closed for as long as possible its ability to do so will decline over time as a result of US actions to degrade its capabilities and as other countries combine to force it open possibly assisting the US militarily to do so. There are also signs that Iran is making exceptions for ships from China and India to pass through which may eventually allow some other countries to piggy back to some degree (by flagging their ships as Chinese). So, while it’s looking more shaky, our base case remains that the War is limited. Our two scenarios are:

- Limited war (55% probability, lowered from 60%) - our base case is that the War is still ultimately limited with Trump likely finding a way to declare victory and reopen the Strait sometime in the weeks ahead. This may still take us into April so oil prices could still go a lot higher to say $US150 (seeing further falls in shares, possibly taking us to the 15% correction we have been expecting this year), before they go lower (shares higher). Along with providing a “wag the dog” distraction from the Epstein files, its probable that Trump’s intervention in Venezuela and War on Iran is partly motivated by a desire to get the upper hand over China and so the US is probably aiming to have the War nearer to being wrapped up by the Trump-Xi meeting at the end of the month. However, with Iran digging in and it looking increasingly like Trump has miscalculated we have cut the probability of a limited war to 55%.

- Long war (45% probability, up from 40%) – however, while Trump may want to declare victory soon, Iran has an incentive to prolong the surge in oil prices and hence the cost to Trump and US consumers. Iran could also descend into chaos with various military groups continuing to threaten ships in the Strait of Hormuz even if Iran officially waves the white flag. This could necessitate a longer-term US involvement and mean a much longer disruption to oil supplies, conceivably resulting in oil prices going to $US200 & beyond driving a sharp sustained fall in global and Australian shares into a bear market. It would be a political disaster for Trump though and lead to a significant loss of confidence in the US – much as occurred in the 1970s!

The key things to watch for will be a sustained fall in missiles & drones coming from Iran, successful shipping through the Strait of Hormuz, indications Iran wants to negotiate and a 10% or more top to bottom fall in US shares which will up pressure on Trump to find a way out.

Longer term implications of the Iran war – more renewables and onshoring of supply chains. Like the pandemic, the Iran War and the impact on oil supplies will have longer term consequences including more pipelines to bypass the Strait of Hormuz, an accelerated push towards EVs, renewables and nuclear power, and even more pressure on countries to bring supply chains of strategic products back onshore. All of which is positive for metal demand. But the further hit to globalisation will potentially make the world even more inflation prone. Could the US and global economy face another inflation wave as the chart implies – reflecting deglobalisation, weakening Fed independence and higher energy prices? It’s a bit odd that Iran figured back then in the third inflation wave and is figuring again now.

Latest updates

PDF version of Firstlinks Newsletter

ASX Listed Bond and Hybrid rate sheet from NAB/nabtrade

Monthly Bond and Hybrid updates from ASX

Listed Investment Company (LIC) Indicative NTA Report from Bell Potter

Monthly Investment Products update from ASX

Plus updates and announcements on the Sponsor Noticeboard on our website