This is one of the most common investor questions I receive from advisers, and it is one of the easiest to answer. It’s fairly simple.

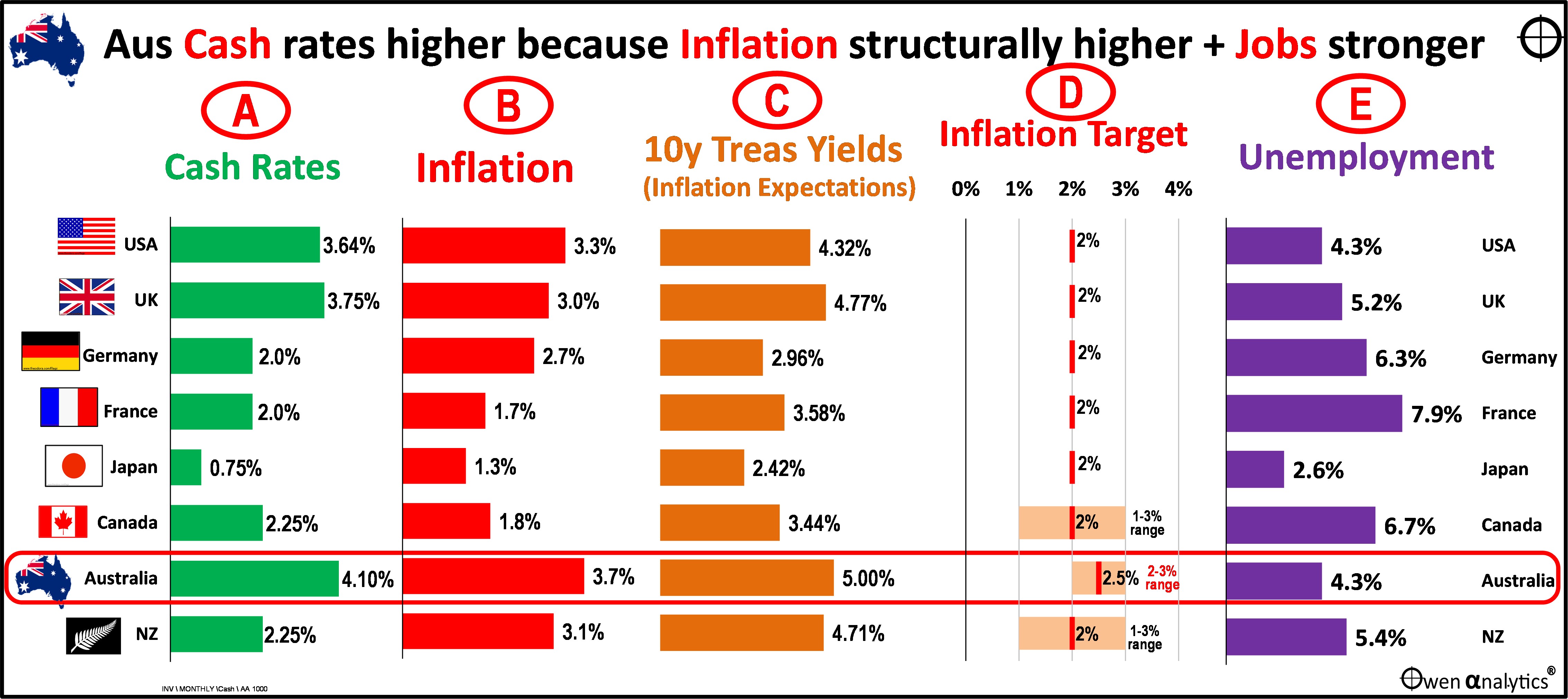

Australians suffer the highest cash rates amongst their rich country peers (chart A) because Australia has:

- The highest inflation rate (chart B),

- The highest medium-long-term inflation expectations ie highest treasury yields (C),

- The highest central bank inflation target (D) – for no good reason at all,

- The strongest jobs market eg lowest unemployment rate (E) (apart from Japan which has a declining population and workforce), and

- The loosest / most undisciplined monetary and fiscal policies during and since Covid.

Bottom line = locked-in structurally higher inflation.

Click to enlarge

Cash rates (A)

Australia’s 4.1% cash rate is much higher than in peer ‘rich world’ countries. (There are plenty of other countries with higher interest rates of course – including Venezuela with 58%, Turkey 37%, Zimbabwe 35%, Argentina 29%, Nigeria 26%, Brazil 14.75% and others, but they are not our ‘rich country’ peers.)

High cash rates are more important in Australia than in any other country because we have the highest proportion of variable/floating rate mortgages in the world. The rest of the world relies much more on fixed rate mortgages, which are far less sensitive to changes in short-term cash rates.

Accentuating the problem is the fact that we have the most indebted household sector.

Australia is the only country to have had to switch from rate CUTS to rate HIKES this year, after the RBA’s three unnecessary rate cuts in 2025 (February, May, August). Those 2025 rate cuts were unnecessary because inflation was running above target, the economy was running above capacity, and unemployment was low, fuelling inflationary wage claims. I warned of this at the time.

Inflation (B)

The latest inflation rates for Australia and other countries (chart B) are to February 2026 – ie BEFORE the impacts of the latest US-Iran war. The exception is USA, which recorded inflation to March running at 3.3% pa. This was a big increase from 2.4% US inflation to February. Most of the increase was due to surging fuel prices in March.

Australia’s CPI inflation of 3.7% to February is well above its peers, and will also be higher again in March, with the impact of higher fuel prices directly and indirectly flowing through to many other categories of spending.

Inflation expectations – bond yields (C)

Australia also has the highest medium- to long-term inflation expectations, expressed in yields on 10-year government bonds (and for all other maturities / terms for that matter).

This means current and future taxpayers pay more interest on government debt, as federal and state governments have to borrow to finance their wild spending deficits and also refinance the existing piles of debt.

Central Bank inflation target (D)

The Reserve Bank has always had the loosest / highest / laziest inflation target in the world. Why? There is no good reason or excuse for this.

There is no philosophical or ethical justification for a government to deliberately set ANY positive target for inflation – ie to deliberately engineer CONTINUALLY rising prices and continually debasing the value of its mandated monopoly currency in the hands of its citizens. Deliberate price inflation / currency debasement (even 1% per year) is nothing more than officially sanctioned theft of citizens’ wealth.

Governments love high inflation because it means high interest rates, so they can lure in lenders (bond holders) to finance their debts and then repay them in the distant future with debased currency worth a faction of its current purchasing power.

High structural inflation

The reason or excuse for Australia having the highest inflation target in the world – ie the most aggressive money debasement and theft of citizens’ wealth, probably has its roots in our Federation pact.

The formation of Australia at Federation in 1901 was based on three central features for the newly formed nation:

- high protection barriers to keep out cheaper foreign goods,

- restricted ‘White Australia’ immigration policy to keep out low-wage, non-white labour, and

- centralised wage fixing/indexation to redistribute the windfall profits from protected industries to the protected workforce.

Today both the White Australia immigration policy, and the industry protection barriers are (mostly) long gone, but for some unknown reason we still have the heavy-handed, centralised wage fixing and indexation system, which is a relic from the distant protected past, and now unique in the world.

An additional inflationary feature of Australia’s industry structure is that just about every domestic industry (eg banks, retailers, telcos, utilities, toll roads, airlines, ASX, ports, etc) is a monopoly / oligopoly where the dominant incumbents can simply pass on rising input costs to consumers in the form of higher prices, rather than being borne by shareholders.

In addition, Australia has had the highest population growth rate in the world (outside of Africa) since Federation and still has. It also has one of the best (youngest) demographics of any ‘rich’ country. See: Australia's remarkable population-led growth (31 Jan 2024)

These factors combine to result in Australia’s higher structural inflation, which is reflected and perpetuated in our higher central bank inflation target.

Low unemployment (E)

We also have the lowest unemployment rate in the rich world, aside from Japan which has a declining population and declining workforce.

An additional problem for Australia is the fact that the vast majority of hiring is for the government sector or ‘non-market’ (private sector but revenues/prices are set by government – eg all those private suppliers to government services like NDIS, Home Care packages, construction contracts on public works, etc).

Currently the US also has a 4.3% unemployment rate like Australia, but Australia has a higher workforce participation rate of 64%, compared to 61.9% in the US, so our jobs market is tighter.

Poor monetary and fiscal policies

The RBA and federal / state governments share the blame for the post-Covid inflation we are still suffering. However, true to form, both sides now conveniently divert the blame for rising energy prices to Russia’s 2022 invasion of Ukraine, and now the 2026 US-Iran war.

The fact is that the RBA woke up to the Covid stimulus inflation later than the rest of the world, then it hiked interest rates to attack inflation LATER, SLOWER, and LOWER than other central banks.

Then, for some unknown reason, the RBA CUT rates unnecessarily in 2025 when inflation was still running above target, when the economy was running at or above full capacity (inflationary), the unemployment rate was still low (also inflationary), and the government was backing double-digit wage claims.

Meanwhile, federal and state governments have squandered windfall revenue gains from raw material export booms, run war-time-like deficits on mad un-costed spending sprees, run up war-time-like debt piles, supported inflationary wage claims, and wound back four decades of productivity-enhancing industrial relations reforms.

The next time you (or your clients) wonder why Australians suffer the highest interest rates in the ‘rich’ world, you now have some answers!

Ashley Owen, CFA is Founder and Principal of OwenAnalytics. Ashley is a well-known Australian market commentator with over 40 years’ experience. This article is for general information purposes only and does not consider the circumstances of any individual. You can subscribe to OwenAnalytics Newsletter here.