Before the conflict’s commencement, the financial market’s main worry was the rise of AI tools and the potential implications for software companies, with substantial declines in their equity valuations being a painful experience for many investors. In being large lenders to the software space, US private credit funds have also been caught up in the turbulence, with fears of spiking defaults and lower returns impacting investor confidence.

Outflows from US private credit funds reached a crescendo last week, with famed lender Blue Owl (OWL) announcing investor redemption requests for 1Q26 totalled $US5.4 billion from two of its funds with significant software exposure. Investors in OWL’s Credit Income and Technology Income funds asked for an incredible 22% and 41% of their capital to be returned. For both funds, redemptions are now effectively gated, limited to 5% per quarter in accordance with the funds’ Business Development Company (BDC) structures, resulting in a frustrated queue of investors wanting liquidity.

OWL’s share price is now down two-thirds from its peak in early 2025. By contrast, OWL’s Credit Income Fund $A bonds, which are effectively secured against the fund’s underlying assets, are less impacted and continue to hold their value (refer Chart 1). These bonds are protected by a significant equity cushion, with fund leverage at just ~0.7x, redemptions gated and a BDC mandated leverage covenant limit in place of 2x.

While we don’t have the software concentrations, Australian private credit is significantly more exposed to the riskier side of real estate lending, especially higher yielding commercial and residential development. In many ways, private credit’s exponential growth since the GFC was a meeting of minds, with local investors understanding Australian real estate and its resilience through multiple cycles; comfortable loan-to-value completion ratios have acted as a powerful magnet for yield hungry investors.

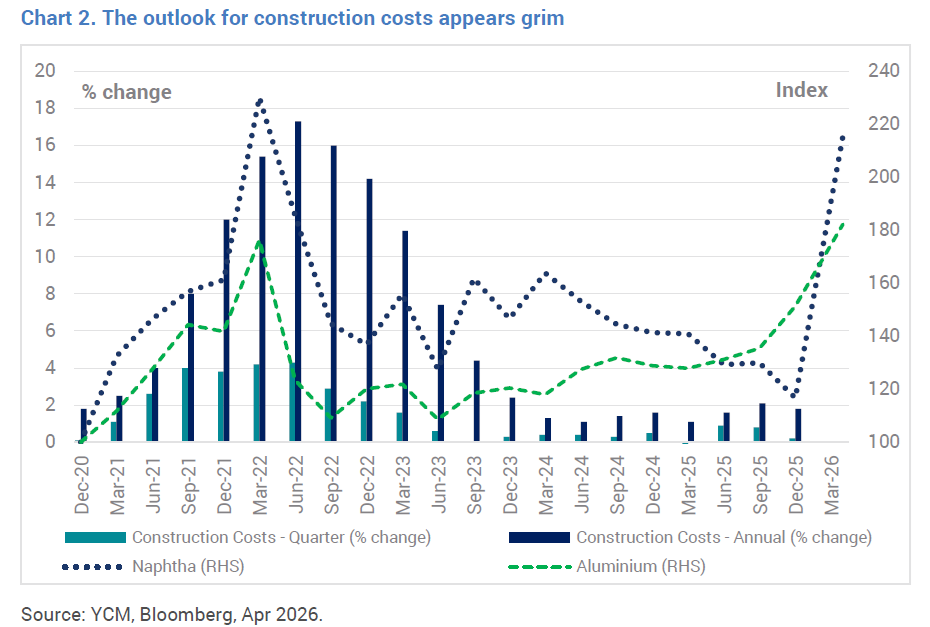

This brings us back to the current Iran conflict and the impact of inevitable cost escalations and higher interest rates on construction sites across Australia. Already weakened through the 2022/23 period of higher interest rates and cost escalations, property development/construction is enduring another round of higher costs (refer Chart 2) and constrained demand. For instance, since the commencement of hostilities, naphtha and aluminium prices – key components in plastic and metal building products – have increased by 85% and 20% respectively. Moreover, in being highly correlated (i.e. increased costs impact all developments similarly), a diversity of development exposures might offer only limited protection from credit losses given the systemic risk profile.

This confluence of events, if sustained, is likely to fuel similar redemption pressures in Australia, with more pure play private credit funds likely to close their liquidity gates in the months ahead. While actual losses will most likely be lower than feared, being unable to meet redemption requests for funds that have been marketed with a ‘promise’ of ungated monthly or quarterly liquidity will be damaging to the private credit landscape.

Phil Strano is Head of Australian Credit Research at Yarra Capital Management, a sponsor of Firstlinks. This article contains general financial information only. It has been prepared without taking into account your personal objectives, financial situation or particular needs. Both the Yarra Enhanced Income and Higher Income Funds are zero leverage funds, providing attractive yields.

For more articles and papers from Yarra Capital, please click here.