Campbell (Inquiry 1979), Wallis (Inquiry 1996) and Murray (Inquiry 2014) may all be splendid Scottish names but they will be forever etched in the history of Australian financial markets. Campbell opened our markets and Wallis gave us much of the regulatory structure, but David Murray has cast his net wider into both micro and macro issues in his 320 page (not 500 as I wrote in the newsletter) report.

This note is my initial reactions focussing on impacts for wealth management, including retirement, financial advice and superannuation. As Joe Hockey told the lock-up, you need to "read it and read it and read it" to capture all the content. So it is acknowledged that this is not a comprehensive review of the entire Report.

Joe Hockey issued the final Terms of Reference on 20 December 2013, and David Murray and his Inquiry have delivered the goods in under a year. The Final Report is available here.

Some highlights of the Report

It contains 44 recommendations, based on a test of meeting the public interest. It says the financial system has performed well since Wallis but has some weaknesses. It aims to make the system more efficient, resilient and fair, but still responsive to market forces.

Superannuation

Superannuation funds are now big businesses. The amount in superannuation surpasses the market capitalisation of all companies on the ASX and Australia's annual GDP. The Report notes super assets will probably exceed the banking system within 20 years.

The major recommendations are:

* seek broad political agreement for the overall objectives of superannuation. The Report says super does not have a consistent set of policies.

* the Government should restore the general prohibition on direct borrowings by super funds (page 86). This is a setback for the industry that has sprung up promoting borrowing to buy residential property under LRBAs. It will apply where the borrowing is used to purchase assets directly, so the broad range of managed funds and ETFs which internally gear their funds will not be affected. It will still be possible to gear a super fund but not directly.

* a formal competitive process may be needed to allocate new default fund members to MySuper products. This draws on a Grattan Institute study showing excessive superannuation fees and quoting the Chilean system where the right to manage 'default' funds is auctioned to the cheapest supplier. Another perspective on the Chilean system was provide in David Bell's article, and these problems will need to be addressed. The Report acknowledges much more work is required until a formal review by 2020 if Stronger Super is not working well.

* To assist longevity, trustees of super funds could select a comprehensive income product for retirement (CIPR) for their members, effectively pooling risk to ensure income throughout retirement. It would deliver an enduring income stream to give retirees more confidence that they can spend in retirement.

* Super funds should provide retirement income projections for members to improve engagement.

Financial advice

Although there has been enormous media and public focus on the quality of financial advice and especially the problems caused by vertically-integrated businesses (including the oft-quoted statistic that the four major banks plus AMP control 80% of Australian planners), the subject did not receive much attention in the Interim Report. However, it did contain this warning:

" There has been a tension between providing financial advice for the benefit of consumers and the product distribution role played by advisers ... The Inquiry considers the principle of consumers being able to access advice that helps them meet their financial needs is undermined by the existence of conflicted remuneration structures in financial advice."

The most significant proposal that affects the vertical integration financial advice model is to rename 'general advice' with a more appropriate, consumer-tested term. Advisers will also be required to disclose ownership structures.

The other main recommendations are:

- introduce a targeted and principles-based product design and distribution obligation. Page 198 of the Report is worth reading in full, as it describes this obligation, including identifying the target market and recognising the product's intended risk and return characteristics in the design phase. There needs to be an agreement with distributors on how the product will be distributed. Breaches would incur significant penalties.

- ASIC should have a 'product intervention power', which would allow products to be banned or materially changed.

- remove impediments to product disclosure and improve fee and risk communication with consumers.

- better align interests of financial firms with those of consumers, including remuneration structures and ensuring life insurance and stockbroking businesses do not affect the quality of advice.

- raise the competency of financial advisers including an enhanced register of advisers.

Post-retirement income

The Report has a heavy focus on post-retirement income. The Interim Report had said:

"If superannuation benefits are not transformed into retirement income streams effectively, taxpayers ultimately carry significant risk in the form of higher Age Pension costs."

The Report argues superannuation assets are not being converted to efficient post-retirement outcomes, and the development of a CIPR as mentioned above receives high profile (see page 117).

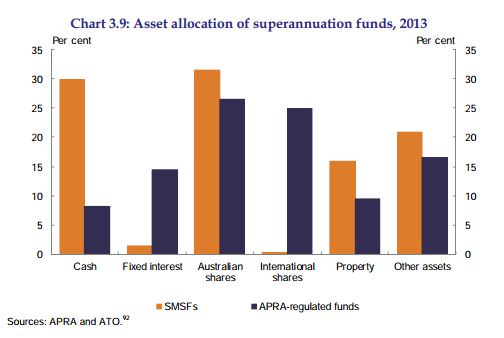

Self Managed Super Funds (SMSFs)

SMSFs now hold about $600 billion of Australia's $1.8 trillion in superannuation with one million trustees. However, on my first read, the sector does not receive significant attention. Although SMSF borrowings are estimated at only about 1% of assets, the Report recommends removal of the ability for all super funds to borrow, including SMSFs. The argument goes that investors have many other ways outside super to lever their investments, and superannuation savings should not be put at risk by more leverage.

This is a controversial recommendation opposed by many SMSF specialists, but I support the approach. Some people need to be protected from themselves, and property spruikers will take advantage of too may people if borrowing is allowed. See my arguments here and here and my submission to the FSI here.

There are significant differences in asset allocation between SMSFs and large APRA-regulated funds. In particular, SMSFs hold little foreign securities but about 30% in cash. However, on first read, I could not see any recommendations on ways to address this.

Fees

Murray believes there is little evidence of strong fee-based competition in the superannuation sector, and operating costs and fees appear high by international standards. This indicates there is scope for greater efficiencies in the superannuation system.

The formal competitive process described above is designed to improve competition and efficiency in super, to be introduced by 2020 if Stronger Super is not effective (see page 101). The Report says 50% of MySuper products have fees ranging from 84bp to 117bp, and it believes there is much scope for this to fall further. If APRA-regulated funds could reduce fees by 30bp, the savings for investors would be $3.5 billion per annum.

Governance of superannuation funds

The Report also recommends a majority of independent directors on the boards of the trustees of public offer superannuation funds including an independent chair, and a strengthening of the conflict of interest requirements.

This information is general in nature and takes no account of any investor's personal financial circumstances. Investors should consider taking professional advice on their investments. There are many other aspects of the Report which will be covered in later editions of Cuffelinks.