Oh no, landlords will sell their dwellings. This is terrible news for renters!

If I hear this nonsense one more time…

A housing math lesson

There are about 10.8 million dwellings in Australia and we add about 160,000 new dwellings to the stock each year.

Of those 10.8 million homes, about 3.6 million are owned by landlords and rented in the private market. The rest are owned by homeowners or are public housing.

If landlords never sell, there will always be at least 3.6 million private rental homes, even if the stock of homes increases over time.

The most extreme way to increase homeownership without landlords selling is if only first-home buyers bought all the new homes. You could even call this approach an ‘investor ban on new housing’, which is something that people think is very bad.

Let’s go through this scenario. In ten years, if the recent level of new housing construction continues, there will be about 12.4 million dwellings in Australia. But there will always still be those same 3.6 million dwellings owned by landlords that exist today.

So the best we can do is go from 66% to 72% homeownership over a decade, assuming an investor ban on new homes has no effect on how many new homes are built.

It is rarely noted that landlords not buying new homes, or landlords selling existing homes, both have the same effect of shifting the pattern of ownership. They are equivalent ways to shift the composition of ownership of the housing stock.

This would be much more obvious if we lived in a world where one person owned all the dwellings — the way to increase homeownership in this world is for this one owner to sell some of their dwellings to renters. But the maths doesn’t change because there are millions of landlords.

To boost homeownership back to its 71% peak level that Australia saw in the early 1970s would require over 500,000 landlord sales in net terms — whether that is landlords not buying new homes or selling their existing homes.

That’s about a year’s worth of normal turnover (sales) in the housing market. It would take nearly a million of these landlord sales to get us to 75% homeownership.

The private rental sector constantly changes

It is also worth remembering that property owners buy and sell rental dwellings all the time. Dwellings often change from owner-occupied to rental, or vice-versa, even without a sale, when homeowners move in and out of a property they own.

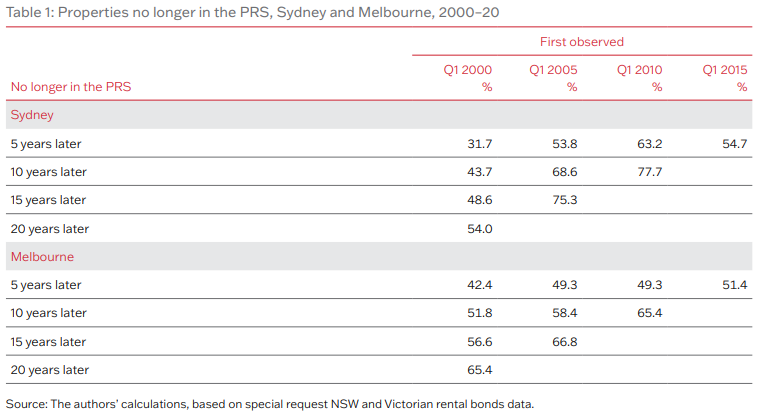

Only about half of the dwellings in the private rental sector (PRS) are still being rented five years later, as the below table from this report shows. The rest have been sold to owner-occupiers, or their owners have moved in, or they have been redeveloped and not rented.

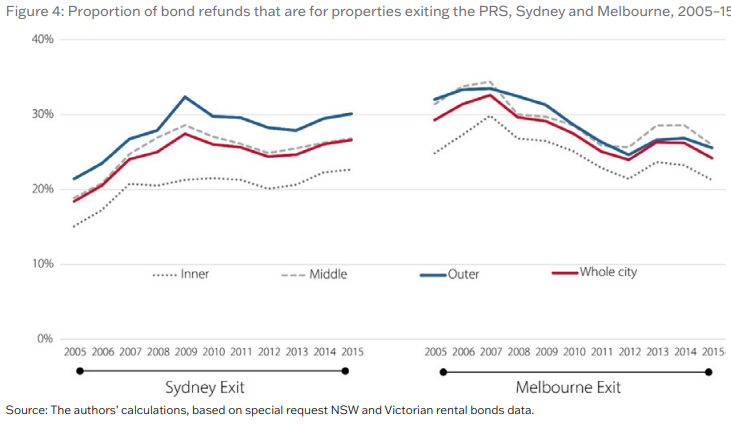

In fact, about a quarter of rental dwellings are removed from the rental stock when a tenant leaves, as the below charts show.

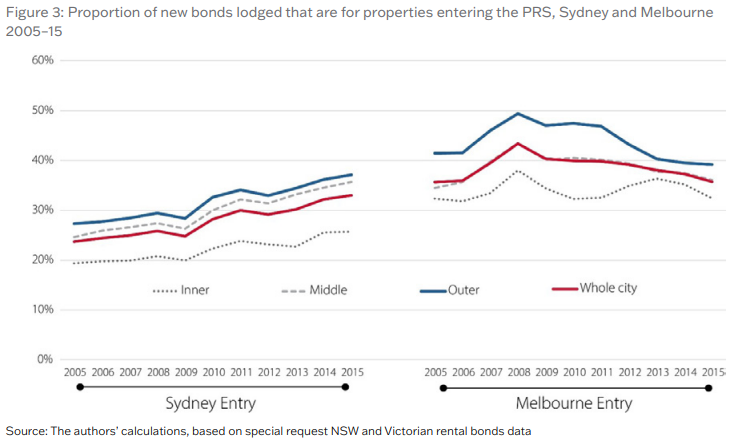

Every year, a huge number of homes also enter the rental market. The below charts show that in Sydney, the share of new rental bonds for dwellings that have never been rented before has been rising from about 25% of total new tenancies to 35%, while for Melbourne the churn into the rental market has been consistently higher than that.

But what about renters?

None of this ownership churn affects the supply, or stock, of dwellings. This is because a former renter who buys a home is now also no longer a renter — it’s a minus one from the supply and a minus one from the demand for rental housing, as the below diagram describes.

Even if a first home buyer creates a newly formed household, coming from previous homeowning households and not directly from the rental sector (like young adults moving out of a family home), this still removes the demand for housing from those people, regardless of where they would have alternatively been housed.

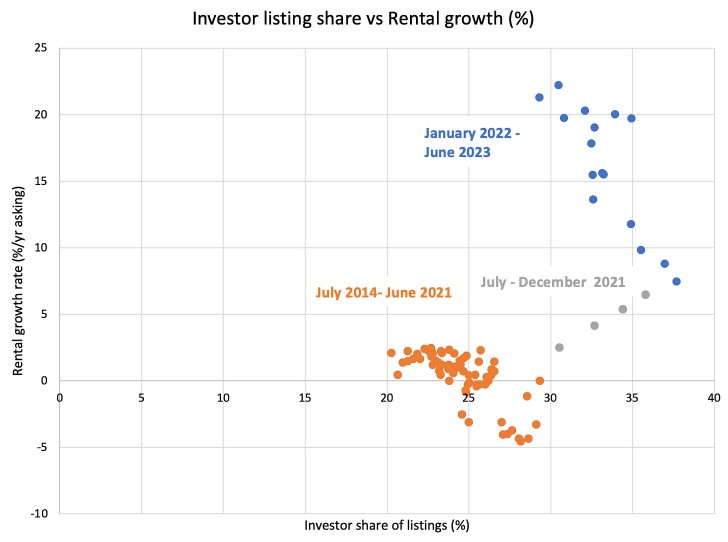

If you don’t believe this housing math, we can directly check whether landlord sales as a share of all sales is predictive of rental increases using the chart below, where I have matched CoreLogic data on landlords (investors) as a share of new sale listings and SQM Research data on asking rents for Australia’s capital cities.

Until mid-2021, the relationship was negative — a higher proportion of landlord sales was related to lower rental growth. Perhaps that’s because investors sell more when rents are falling.

After a clear cyclical change in the second half of 2021, the same negative relationship is there in the last two years of data.

Overall, this data doesn’t provide any evidence for the idea that more landlords selling is related to higher rents. Which is exactly what we would expect based on the simple housing math I discussed above.

It should be a puzzle that so many people can’t do this simple math and seem to want both more homeownership and more landlords and rental housing. Sure, build more homes. But increasing the ratio of homeownership to rental out of the stock of homes means changing ownership patterns, and that means landlords selling on balance.

Dr Cameron Murray is an Economist and co-author of the Book Game of Mates. Subscribe to his written work at Fresheconomicthinking.substack.com. This article is general information.