Last week's article on the future returns to expect from a long-term savings plan was almost 2,500 words, which is a lot for many busy readers. This is a summary of the main research and messages.

In the iconic Australian film, The Castle, the family lawyer, Dennis Denuto, is struggling to make his case in court, bumbling around with a copy of the Australian Constitution. Finally, he sums up in a segment that has both entered Australian folklore and become required viewing for law students:

“It’s the vibe of it ... It’s the Constitution. It’s Mabo. It’s justice. It’s law. It’s the vibe and … ah, no, that’s it. It’s the vibe. I rest my case.”

The Constitution has little relevance to his case. It was simply the vibe of the thing. There’s a similarity now with the assumptions used in calculating future superannuation balances.

Retirement planning should start decades before the end of full-time work. In a wonderful world of returns well in excess of inflation rates, driven by compounding over long periods, bond and equity markets will provide the financial resources for a comfortable retirement far quicker than if returns struggle to beat inflation. But is all that in the past?

Superannuation balance calculators usually assume a nominal rate, then discount the future amount by an inflation factor, currently about 2.5%. In this discussion, 7.5% nominal and 5% real are considered approximately the same.

‘Two cents’ worth’ on super projections

The most popular website for starting to understand investing, including superannuation, for many Australians is ASIC's Moneysmart. It includes a superannuation calculator designed to determine how much super a member will have when they retire. The inputs include age, income, desired retirement age, super balance, employer contributions, personal contributions and fund fees.

The default investment return is set at 7.5% (before taxes, fees and inflation), updated as at 17 April 2020.

Similarly, every major superannuation fund provides its members with some type of online calculator. Over 90% of the members of AustralianSuper, Australia’s largest super fund, choose the ‘balanced’ option, with an objective of CPI plus 4% and an investment timeframe of 10 years. The return assumption is about 7% at the moment.

With Moneysmart at 7.5% and a leading industry fund at around 7% for the default option, the question must be asked: Are they dreaming?

The most obvious factor reducing future returns is the fall in interest rates. Global and Australian markets are at the tail end of a 30-year bull market in bond rates. Fixed income and to a lesser extent, cash, have been an attractive part of the asset allocation in the last few decades.

The extraordinary result is that between 1950 and 2019, the 20-year rolling returns (in nominal terms, not adjusted for inflation) for the S&P500 averages 17% per annum, while bonds delivered 12% and a 50/50 blend a wonderful 14% (Australian market returns would be marginally less).

That’s a retirement tailwind that should go straight to the pool room.

However, the starting point for future returns is a cash rate and bond rate of 0.25%. The Reserve Bank has signalled ultra-low bond rates for many years to come, driven by the imperative to recover in a post-coronavirus world.

But these were glorious investment conditions enjoyed by Pre-Boomers, Baby Boomers, and to some extent, Generation-X. Unfortunately Gen-Y (the Millennials) and Gen-Z are unlikely to have it so good.

All that matters now is the future

While there are as many forecasts in the world as there are economists, let’s draw on four forecasts to glimpse into the future.

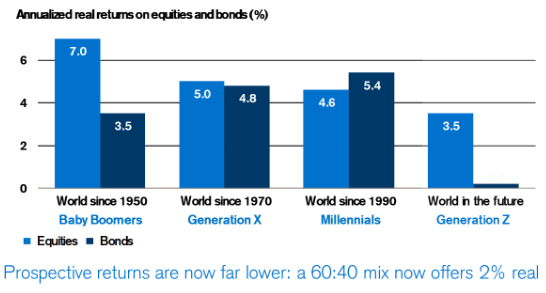

1. Elroy Dimson and the London Business School

The Global Investment Returns Yearbook is a global authority on long-run asset returns. Its current edition quotes the lead author, Professor Elroy Dimson forecasting lower future returns because:

“It’s real interest rates that provide the baseline for all risky assets, and when real interest rates are low, so are expected returns.”

Professor Dimson, together with his colleagues Professor Marsh and Dr Staunton, expect prospective real returns from equities to be somewhere in the region of 3.5%. However, in a typical 60/40 balanced portfolio used for the default option in most Australian super funds, 40% of the portfolio in fixed interest will probably contribute little.

This means the future balanced portfolio may deliver a real return of only about 2% a year.

Global Investment Returns Yearbook, 2020 edition, likely future returns

Reproduced with permission from The Global Investment Returns Yearbook, written by Elroy Dimson, Paul Marsh and Mike Staunton. Copyright © 2020. See acknowledgement at the end.

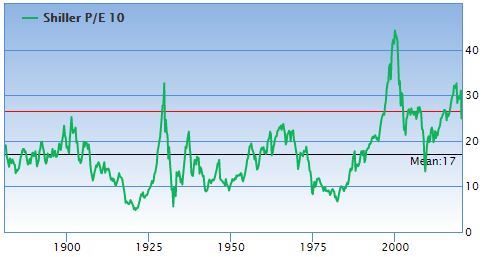

2. Robert Shiller's implied future market returns

Nobel Laureate, Professor Robert Shiller of Yale University, invented the Shiller Price/Earnings (P/E) Ratio and it has become a standard to measure the market's valuation. Further details are available here and his data base is here.

As at 4 May 2020, the current Shiller P/E of 27 was 57% higher (the red line above) than the historical mean of 17 (the black line above).

Based on current P/Es and reversion to the mean to calculate the future stock market return gives around 0.2% (real) a year. (For source and more information see Gurufocus).

The market is expensive and this will reduce future returns. However, Shiller places it in the context of the alternative of the extremely low rates on bonds. He wrote in The New York Times on 2 April 2020:

"On balance, I’d emphasize that the stock market is not as expensive as it was just a month ago. Based on history, we would expect to see it to be a reasonable long-term investment, attractive at a time when interest rates are low."

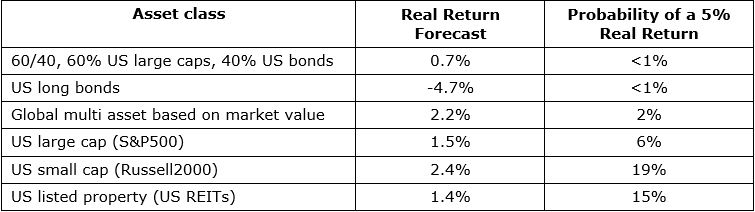

3. Research Affiliates' interactive forecasts

The work of Research Affiliates and its expected return models allows investors to check forecasts across a wide range of asset classes.

Research Affiliates’ Selected Returns for 10 years, as at 31 March 2020

These real returns offer little prospect of achieving the 4% to 5% assumed in superannuation calculations.

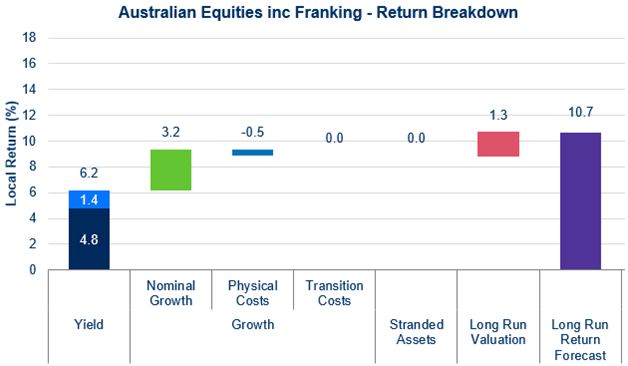

4. Schroders Australia

Schroders Australia gives a local perspective, and for Australian equities over the next 10 years, the forecast is 10.2% (nominal):

In other asset classes, forecasts are 4% for US equities, 6% for global equities, 7.5% for A-REITs and 1% for Australian Government Bonds. This means an allocation of 60/40 (say 30% global equities, 30% local equities and 40% bonds) is forecast to deliver about 5.25% nominal, or 2.75% real.

What should a superannuation member do?

For all the expert opinions, personal judgement of a realistic future return is the final arbiter. For extra security in retirement, instead of expecting 5% above inflation (or a vibe of 7% to 7.5% nominal), aim for closer to 2% to 2.5%.

Baby Boomers who have already built their retirement savings will need to watch drawdown levels, as spending 5% of a pension fund might erode capital quicker than expected. Millennials and Generation Z who are saving may need to put more into superannuation or work longer than their parents to achieve the same balances. The reality is that return for risk payoffs are now lower.

Here's some final words from Robert Shiller's April article:

"As a practical matter, my advice is to look at your portfolio to make sure that it is not so heavily weighted to stocks that further losses would be unbearable. Otherwise, I’d try not to worry too much about the stock market. Most likely, it will do moderately well in the coming years, even if there is a risk that you will need to be very patient."

If someone suggests a 7.5% future return assumption on a balanced fund, "Tell 'em they're dreamin'".

Graham Hand is Managing Editor of Firstlinks. This article is general information and does not consider the circumstances of any investors.

To obtain permission to reproduce the Yearbook chart, contact the authors at London Business School, Regents Park, London, NW1 4SA, United Kingdom. Copyright © 2020 Elroy Dimson, Paul Marsh and Mike Staunton.