Anthony Aboud is a Portfolio Manager for the Perpetual Industrial Share Fund, the SHARE-PLUS Long-Short Fund and the Perpetual Pure Equity Alpha Fund and has been at Perpetual for 10 years and an analyst for 22 years.

GH: You're a portfolio manager for the Industrial Share Fund. Do you sometimes feel there are sectors on the ASX, perhaps energy and resources, where you would like to invest as well?

AA: Resources can be feast or famine types of businesses and there may be times in the cycle when you want to be invested there and other times not. One of the rules of the Industrial Share Fund is that it is not allowed to invest in resources companies so yes, there are times when you would want to own certain stocks. This constraint has not really hurt the performance of the Fund over many decades as it has avoided some speculative booms. Industrials is the nature of the Fund and it has a good investment universe.

GH: You have a large exposure to banks which have done well over time but sold off recently. Do you think that the market is overreacting to some negative factors for banks such as the potential for rising defaults?

AA: There is talk of a recession on the back of higher energy prices, higher interest rates and potentially overstretched consumers. Australian banks were more expensive than their international peers and it has driven some underperformance in the short term, but over the last two years, banks have done well in absolute and relative terms. If we head to a recession and house prices fall materially, our banks will struggle to perform. However, they are extremely well provisioned, well capitalised and are yielding between 5-6% fully franked yields. Our big positions in the space are Suncorp and NAB.

GH: In your day-to-day thinking about risk in the portfolio, do you watch any leading indicators to guide how the mood of the market might change?

AA: There’s the market and there’s the economy. Two things I watch for the strength of the economy are inventory levels and mortgage applications. They are different but give good, leading information. For example, if there are a lot of inventories in the system, it suggests some weakness is coming as stock cannot be sold. Inventory needs to clear before new orders are made. In the US, big retailers such as Target and Walmart have experienced downgrades due to overstocking. Mortgage applications show if people plan to bid for a house, influencing clearance rates and house prices and ultimately construction. They turned negative in May in Australia so that’s a cautionary sign.

Generally on other indicators, I am a contrarian and I feel when everyone is negative about the economy, that may be a positive sign for the stockmarket. Which is why I say the market and the economy are different, as we need increasingly negative shocks for the market to continue to fall.

GH: You wrote a note in January 2021 when the market was going crazy for hot growth and tech companies, often without profits, saying, “When the market environment changes, the focus will swing back to companies with sustainable cash flow. When that happens, we will see a lot of these hyped-up tech names fall 90%.” Are you feeling vindicated?

AA: Absolutely. What we saw with zero interest rates for a long period of time was bubbles all over the place. With no cost of capital and people chasing long duration companies, all it took was a good narrative, a big-talking CEO and suddenly we had the next Amazon. I never believed it. I understand some businesses need to invest capital and be loss-leading for a while, but it’s a lot more difficult than many people think to go from a loss-making concept to becoming a sustainable cash-generating business. The market underestimated that.

GH: On your long/short fund, how do you go about stock selection and risk management with a short book in contrast with a long book?

AA: The main issue with a short book is that you can lose more than 100% of your position. If a short goes against you when prices rise, it becomes a bigger position in your portfolio. If a long position goes against you due to price falls, it becomes smaller. With a long, you might think you got the timing wrong, and you can leave it there for a while. You can’t do that with a short book. You really need good risk management, especially getting the size of the position correct. And you want to be clear at what price you stop out your position.

On identifying shorts, I think the company knows about its problems before the rest of the world does. So look for flags and analyse the behaviour of management and boards, such as accounting tricks or mistiming of acquisitions. The other reason for shorts is where we have a materially different view from the market on the downside potential. Some stocks just appear ridiculously expensive.

GH: So when you look at the ASX now, what sectors or companies look cheap or expensive?

AA: I think there’s some crowding into defensive stocks as investors are nervous about the market and the economy, and money has gone into defensive sectors such as supermarkets, consumer staples, even health care. I understand the reasons but all of a sudden, you're paying too much for something where margins could be squeezed. I also think sectors such as long duration infrastructure will face pressure from rising rates for some years.

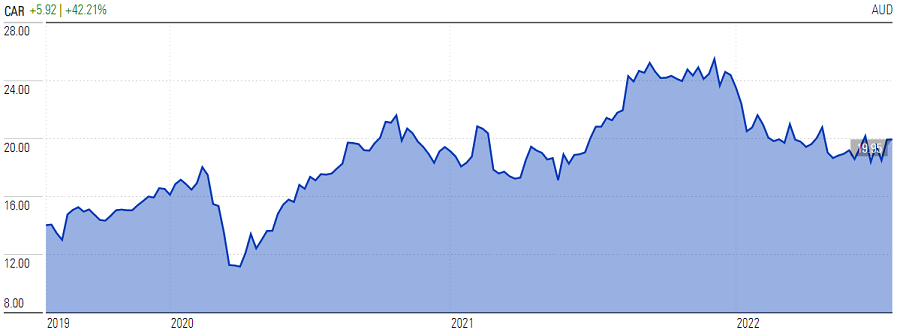

On the long side, first, some of the fallen angels are babies thrown out with the bathwater. They have been de-rated but are starting to look good. Carsales (ASX:CAR), for example, is off around 30% with a P/E in the low 20s for a very high quality business. Second, in energy, we’ve had 10 years of underinvestment, often due to decarbonisation, which is a good thing but we have this tricky period right now for the next five to 10 years where economies need new supplies to meet the demand for energy, such as from a company like Santos. And third, again being a bit contrarian, I like discretionary retail where the balance sheet and management team are strong. Premier Investments is the best in the retail space, and Harvey Norman is unique in the way it owns many of its properties. Harvey Norman is not trading much over its book value which is rare for a retailer.

Carsales.com Ltd, three-year price chart, source Morningstar

GH: Is there a particular stock on the ASX that you like if it can reach your price target?

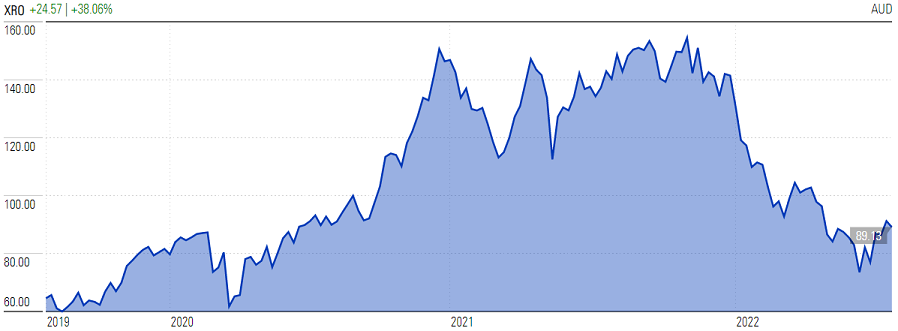

AA: Xero (ASX:XRO) is a very good business. It has great stickiness of customers, who are so positive about the product, especially relative to its competitors. It has upside in adding more features and there’s nothing more certain than the need for companies to maintain accounts and pay taxes. The complexity of taxes is not going away, and they have dominant market share in Australia and the UK with growing earnings. For me, it’s always been a matter of getting the valuation to stack up but it’s a company I constantly watch.

Xero, three-year price chart, source Morningstar

GH: Yes, once they set up their financial accounts, most can't be bothered moving even if the company puts up its subscription fees. Do you have a stock you've sold out of where the thesis didn't work out as you hoped, and it's made you think about your investment process and something you missed?

AA: An international example is Foxtons, a real estate agency in the UK. I liked it because it was generating a lot of cash, it paid a high dividend yield, and I felt I was getting exposure to London property when it was a bit on the nose, a few years ago. But I didn’t heed enough that it was an IPO out of private equity and some industries probably shouldn't be listed. It can be better to be small and nimble and on the ground than become a big company with all the corporate costs. But also it’s more about the people and the individuals in specific markets than the corporate name.

GH: We all love a Warren Buffett quote and he says his favorite holding period is forever. Do you think of a particular stock when you hear that?

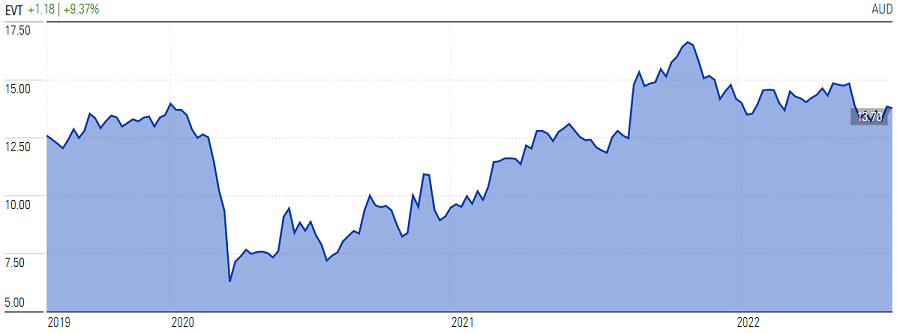

AA: This might surprise people but for me, it’s Event Hospitality (ASX:EVT). It’s like a founder-run business, it's got a strong balance sheet, they have continued to invest in technology and new revenue drivers putting them in a stronger position coming out of the pandemic. Event Hospitalities is one of the largest cinema operators in Australia, owns and operates hotel chains with Rydges and QT Hotels and they also own Thredbo Alpine Village. When the company and the board are making investment decisions with shareholder capital, I feel confident that they are allocating capital to generate long-term returns rather than trying to please the market in the short term.

Event Hospitality, three-year price chart, source Morningstar

GH: Is there a stock in your short book that you continually run over time that has done well for your fund?

AA: I don't like talking about current shorts but I’m happy to talk about a past one. One that was fantastic for us that went bankrupt was the vocational training company, Vocation (listed under ASX:VET in 2013, delisted in 2015). This was a merger of three business from three founders. There was large insider selling at IPO which is always a red flag, and we questioned the sustainability of the business. The company generated 90% of its revenue from subsidies from the Victorian government and these were subsequently cut. That was one of our best shorts.

GH: There’s an ongoing active versus passive debate and passive has attracted more flows recently. With such a spread of stock winners and losers in the last six months, is it a market for active managers?

AA: It should be a good time for active managers. Passive works best in a momentum market that goes up and up when interest rates were low. More money piles into the stocks that are rising in the index, but passive funds don’t work as well in choppier markets. Active managers also engage with companies more. It should be a stockpicker’s market and a chance for active managers to shine. But when fund managers appear in the media and say how good they are, that’s usually a time to sell them so I’m not going to criticise any other funds.

Graham Hand is Editor-At-Large for Firstlinks. Anthony Aboud is a Portfolio Manager at Perpetual Asset Management Australia, a sponsor of Firstlinks. This article contains general information only and is not intended to provide you with financial advice or take into account your objectives, financial situation or needs. Stock charts are provided by Morningstar.

For more articles and papers from Perpetual, please click here.