When superannuation rules change, it’s difficult to know how investors will react, as everyone’s personal circumstances are different. While some see the changes as a call to action, others throw their hands up in frustration.

The Reader Survey from last week is now closed, but please add further feedback after the article, including commenting on what others did if appropriate.

The most revealing part of any survey is often the comments, and many of these are reproduced below to show the actions of hundreds of our readers.

The full survey results and all comments are linked here, but some highlights include:

Q1. Did the new 1 July 2017 super rules affect your investing decisions?

Yes 58%, No 42%

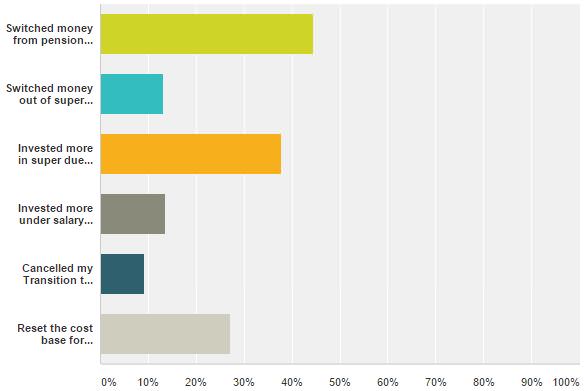

Q2. If ‘Yes’ to Q1, in what way did your investing or actions change (multiple answers allowed)?

The two highest categories were 44% of respondents switched money from pension to accumulation due to the new caps, and 39% invested more now due to reduction in the non-concessional caps next year. An additional 14% added to super due to the changing concessional caps. A solid 27% reset their CGT base on pension assets, but only 9% cancelled TTR arrangements.

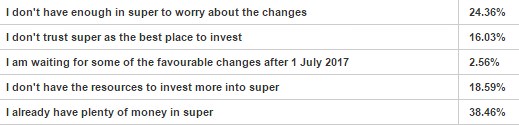

Q3. If 'No' to Q1, why did your super investing not change?

Q4. If you invested more, how did you decide the amount?

A high 57% based their additional investments on using up the existing caps, 31% based on the amount they had available outside super and 11% based on the amount they want in super.

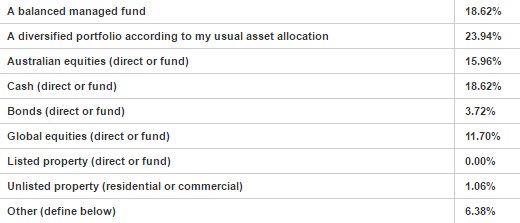

Q5. If you invested more, into which type of asset did you mainly invest?

The most popular types of investment were balanced funds and the usual diversified asset allocations, with strong support for cash, perhaps parking money to wait for other opportunities. Global equities were not far behind domestic equities, which is different from the usual weighting towards Australia, and surprisingly little in the property allocation.

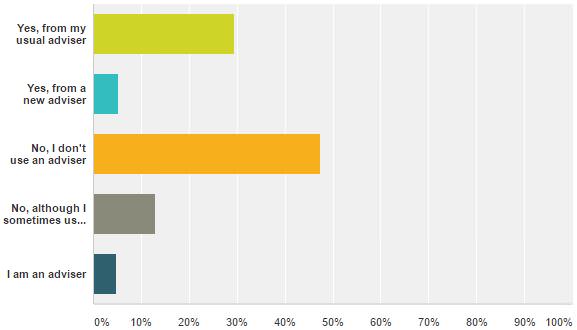

Q6. Did you seek financial advice on the changes?

As reported in previous surveys, almost half Cuffelinks’ readers are self-directed. The new super rules are complex so perhaps this was time when more people should have at least checked understanding or calculations with a professional. A relatively high and unexpected 13% use a financial adviser but did not in this instance.

Q7. Will you invest less in superannuation after 1 July 2017 due to the caps?

A high 57% said they will invest less in super in future, showing the industry has had a one-off boost and the top will be taken off future flows.

Please see the full survey results for more details.

Thanks to all who participated for their insights.

Here are some specific actions taken by our readers:

- Shut down my SMSF and transferred into an existing industry fund to put all super in one place.

- Totally restructured my super. Moved everything from a bank-based super fund into my SMSF, using a recontribution strategy and building up my wife's super as non concessional contributions.

- Paid maximum pension to myself, paid minimum pension to my spouse and then recontributed money to get my wife up to the $1.6 million limit.

- Wanted to commence TTR after reaching preservation age and commence working part time. Decided against this and am now living more frugally rather than commencing TTR.

- Chose to withdraw and recontribute my modest pension account. Even though I didn't use the full limit, transitional bring forward rules leave a higher limit for the next two years.

- 16 times rule on defined benefits meant I had to divest some of my main pension. I decided to re-invest that money directly in shares in my own name rather than switch to acculation phase.

- While the financial-return relativities of $ inside-super vs outside-super are still broadly in favour of inside-super (depending on marginal tax rates etc), the ongoing issue of legislative risk re: super continues to impact considerations at the margin. So - decided to keep a bit more outside super, for flexibility.

- Unable to introduce money into super due to the 1.6 million limit.

- Will decide on CGT tax relief later, doesn't have to be done until closer to tax submission time.

- In pension phase so sold shares with large non-realized cap gains & build Cash balance for start of accumulation

- Wife was convinced she met work test, hence the additional funds were to take advantage of that, and to recontribute to her accumulation from my above cap pension

- Made major withdraw and re-contribution due to abolition of anti-detriment payments

- Sold most shares bought before 9 November 2016 plus sold some shares bought since then with nice profits where suspected that share price likely to fall soon. Also withdrew and recontributed to take final advantage of 3-year carry forward rule to turn taxable amounts into non-taxable amounts.

- diverted new contribution money from super into insurance bonds

- I have sold down all assets carrying notional capital gains while the fund was wholly tax free. The resetting rules are complicated and will be a headache, especially for complicated assets such as instalment warrants. I have held back notional losses until the new year so they can shelter gains when the fund is taxable. My investments will rely far less on income investments and will take advantage of growth assets now that not all assets need to fund the 4% minimum income stream..

- 2 member fund. both in pension mode (1 a TRIS). Previously segregated assets. Then unsegregated as all in pension mode. Now need to stop TRIS. Has mucked up the accounting of the fund re segregation.

- Moved $700K out of non super into super for the caps

- This has entailed moving from the normal asset allocation to liquidate some holdings to fund the transfer. After the transfer has been done, the asset allocation in the super fund will significantly vary from normal long-term asset allocations.

- Keep changing goal posts. So now have portfolio outside super.

- I rolled my pension components out of SMSF to an Industry fund and now have SMSF in accumulation only

- suddenly we are taxpayers again. vis. ST vs LT gains, Gains vs yields, massive increases in accountant charges

- Increasing assets allocation to overseas low-yielding stocks as future pension payments will be less.

- Changed from TTR to pension as reached 60 and working as my mood dictates

- I will reduce using super as a saving tool as dont trust the government to keep their hands off it in the future

- Balanced super funds between spouse and myself so that we could both achieve a maximum of $1.6m in pension accounts

- Took funds from spouse in retirement and contributed to spouse who is in accumulation mode

- Changed nothing this year but will likely make changes in the coming years (mortgage payments were more appealing despite the low interest rate)

- Decided not to sell an investment property as proceeds can no longer go into super due to the TBC

- CC cap reduction means have to reduce our salary sacrifice contribs by $10K each and considering directing this to an investment property.

- Withdrew funds from my name and re-invested in wife's name both to equalize non-concessional and also to be under $1.6.

And here are some general comments:

- The cap was a long overdue partial re-introduction of RBLs foolishly removed years ago.

- I'll be paying much more tax !

- Broadly agree with the intent to limit complete tax-free status of an unlimited amount in the pension account. That was never the intent and far too generous an outcome to a small group of wealthy Australians

- In principle I do agree that super should not be an estate planning platform for wealth transfer to the next generation. Nevertheless it must remain attractive and rewarding to fund ones own retirement.

- WHEN ARE THEY GOING TO STOP MAKING CHANGES

- I think the changes were necessary as wealthy people were using it as a tool to pass on wealth to their children

- A $1.6mn per person pension account cap is highly inadequate for those wishing to be self funded retirees. We are living longer and a $3mn+ cap would have been more realistic. Again political shortism has got in the way of good economic management, as government pensions will grow significantly in the coming years. And it is disingenuous of Fed Govt on one hand placing further restrictions on those responsible Australian who have tried to provide for their retirement, whilst on the other hand those in Federal Parliament and bureaucracy have a separate and superior superannuation, fully funded by the taxpayer via the Future Fund.

- The current tax free status on superfunds can not be sustainable, some incentive is sensible but a 15% tax on earnings would be ok.

- I have lost faith in core super because of the uncertainty especially with changing Governments and Treasurers.

- Whilst the recent changes effectively revisit the old reasonable benefit concepts, I believe the simple super changes made by Howard/Costello were too generous and were bound to be reversed.

- I still support the government imposing caps to limit the generous treatment of superannuation at the upper end of the wealth spectrum

- I believe Super policy will never be safe from any incumbent government

- Sadly, these changes are not going to be the last, especially if labor wins at the next election.

- Inequity of no grandfathering provisions for funds in pension phase, particularly effect of non taxable lifetime pension income on account based component.

- Keep money invested outside super as well. Who can trust a government.

- A lot of noise is being made although there are relatively few affected by the 1.6M$ cap.

- I believe the super changes were fair despite the fact that they result in me paying more tax on the payments I receive from my employer super and personal super. Super tax benefits are now more focussed on providing for retirement, not just wealth accumulation.

- I reached the maximum 3 year contribution level prior to the announcement.

- changes should have been grandfathered have caused much stress,time and inconvenience and cost

- I may have to draw a minimal amount. I am 82 and am more interested in spending!!!

- The lack if clarity back in March on how the cap was to be practically implemented increased my fear of going over the cap on 1 July (and being penalised). Didn't help that my super balance is continually changing with market conditions so pre-"guessing" my balance (based on 2 super accounts) for 1 July was a nightmare. I also fear this "pull back" on super is just the start of more stringent rules to come.

- Glad I took professional advice.

- The changes are irritating after 25 years planning and saving. The inability to move money from the accumulation account to top up outgoings from superannuation pensions are highly irritating.

- It would be better if there wasn't so much complication in the rules re super

- I stopped salary sacrificing this year. Next year I will sell some shares and place this amount in super and claim a tax deduction up to the limit. I will do this in June 2018, once I know how much I have available in the new 25k limit.

- No action possible or required.

- Will be drawing less in pension so may make changes over time to asset allocations. Also will be changing non super investing strategies

- 1.6 mill cap generous but politically realistic, but the fine print is horrendously complex.

- We don't have $1.6m each but when one of us dies the remaining member will have in excess of $1.6 and a restructure will have to take place. Given our ages we don't need anymore in Super. We continue to work and have 11 months until 75.

- Retrospective government action is very disappointing.

- I have just semi-retired so the TRIS changes will not impact . I also remain just under the $1.6m cap. Btwn my wife & I we should have sufficient in super to meet our aims. We will sell two investment properties later this year & may put another $300k into super.

- Death, taxes, & changes to super rules

- I can see no merit or justification to the decision not to remove the work test for those over 65 and retired wishing to make future concessional contributions

- My accumulation fund will grow by 25K plus income earned after tax. Pension will stay around $1.6m after compulsory income taken due to investement income. Major change is not being able to add to my accumualtion fund. However this money will likely be tax free in my hands as $18.2k is the tax fee threshold.

- Will significant affect our investment strategy as we will now have super income and capital gain that is taxed and will have increasing funds for investment outside super as we can no longer make non-concessional contributions. The CGT Relief and opportunity to lock in any losses on individual parcels of shares will also affect individual investments.

- The ongoing stuffing around with the superannuation rules by both major sides of politics constitutes significant legislative risk, and with the budget still no closer to being in surplus (again, the fault of politicians across the spectrum), does anyone REALLY believe they can invest in super for the long term (let alone the short term), without considering legislative risk, without the government of the day considering sticking their greedy itchy fingers into the super pot? Retrospective changes have become a habit and will only get worse.

- Cap should have been higher given low growth environment which could go on for a long time .we have already lost a decade of opportunity due to gfc and lack of spend by federal,government to stimulate. It's obvious and has been for some time that companies don't want to spend and don't want to pay much to employees so where will growth come from when people don't have money to spend

- I have no trust in Polies anymore thay are liars and totally untrustworthy.I will do my own thing to invest and can only blame myself if i fail and not let these no hopers do it for me.A totally disgruntled Liberal.

- A shameful bastardisation of the principles of Super by our Federal government and equally damaging and spiteful implementation by the ATO.

- Please correct me if I am wrong about not being ineligible to make further Super contributions upto $25000 per annum if a "worker"is over 65 & already has in excess of $1.6 million inSuper on 1/7/17

- Ideological changes pushed by pampered, cynical Treasury bots who have taxpayer funded pensions and don't know how the real world works.

- politicians and superannuation need separating

- Super much less attractive now due to legislative risk and the death tax no one talks about for any taxable component going to adult children. I'm winding super back in favour of personal negatively geared investments. The party is over and you can't trust politicians where there's a big pot of money.

- I feel the same frustration as many others at the caps that have been legislated. The Govt seems to be at the mercy of Treasury "modelling". Surely allowing people to live off their super by enabling them to invest more funds into their schemes will save on Govt pension outlays. Yes, I know there is some lost revenue for the Govt but people also feel better supporting themselves.

- The Transfer Balance Cap is an obviously a temporary measure designed to last approximately 5-7 years (i.e. at least two elections) as part of the process of a having a flat taxation rate across superannuation, that is, having the retirement phase taxed at the same rate as the accumulation phase.

- govt needs to stop constantly changing the rules

- I think it is pertinent to have good investments outside super as well. You can't trust governments!!

- Trust in superannuation for the future has been destroyed by constant government milking, to avoid hard tax decisions now.

- Still attempting to recover from the GFC . However this now appears unlikely unless take on extreme risk and as now in pension mode reluctant to go to that stage.

- The cap needs to be lifted to allow more people to increase their balance to are level that will sustain a good standard of living.

Graham Hand is Managing Editor of Cuffelinks.