As investors, we all like to snap up a bargain, but cheaply-priced stocks tend to provide short-term, temporary pleasures. Meanwhile, a genuine quality gem is the gift that keeps on giving, and giving, and giving.

Investors need not look any further to find evidence of that statement than the recent interim financial report release by IT services provider TechnologyOne [ASX:TNE].

While the numbers and metrics were once again of the superb kind, building on a remarkable track record and legacy spanning close to two decades and counting, most analysts and market observers would not describe the shares as ‘cheaply priced’.

Trading on a forward multiple of 48x market consensus forecast for FY24 EPS (54x for FY23), it should be no surprise there is to our knowledge only one Buy rating left, from a mesmerised Wilsons, alongside an upgraded price target/valuation of $18.12.

Most targets and valuations congregate around $15-$16 while the share price since the H1 release has risen from $15.50 to $16.30 this week. Management at the company has stuck with its guidance for EPS growth between 10-15% but just about everyone, including management itself, believes this will prove conservative when final FY23 numbers will be released later in the year.

Already speculation is growing over how much sooner the longer-term target of achieving $500 million in annual recurring revenue (ARR) - still set for FY26 - will be achieved. And by how much can the ARR number exceed the target by then? Some believe $700 million by FY26 is not impossible, which implies there's more upside in the share price, irrespective of today's metrics and share price gains already booked.

Herein lays the first major challenge when dealing with a perennially outperformer such as is TechnologyOne: what kind of ‘valuation’ is appropriate?

True quality 'values' differently

If you're a religious disciple of Benjamin Graham's The Intelligent Investor, shares in TechnologyOne have probably never been on your radar.

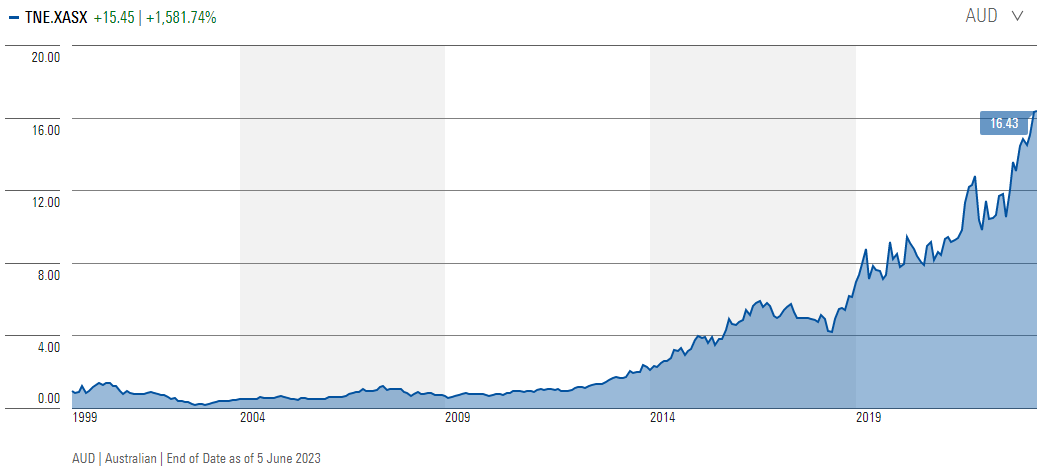

Sure, they must have been ‘cheap’ at some stage, the years immediately following the Nasdaq meltdown in March 2000 come to mind, but it's only fair to say the company back then was nowhere near the Quality offering we are discussing today.

Having said all of that, the returns for shareholders have been nothing short of exceptional over the past 20 years. Let's ignore for the time being that shares could have been snapped up as low as 7 cents a piece during the post-2000 bear market.

By early 2008, shares were trading above $1. Five years on, they reached $1.50. Five years after that, we're in 2018 now, the shares approached $5. One year ago, on the 31 May 2022, the shares closed at $10.50.

Source: Morningstar

With the assistance of Harry Hindsight, there's one conclusion that stands above any form of debate: when shares in TechnologyOne sell off, you buy. This long-term growth story is still nowhere near ending. If anything, both analysts and investors laud the underlying acceleration that is taking place through customers migrating towards the Software-as-a-Service (SaaS) offering.

SaaS literally creates a win-win for both sides of the ledger. For customers, migrating to the cloud brings increased flexibility and significantly lower costs (reportedly up to -30%), while for TechnologyOne those same benefits accrue into rising margins. Current forecasts are for a gradual increase towards a profit margin of 35%-36% from 30% a few years ago.

Contracts typically allow for price rises in line with inflation which, this time around, is providing an extra-kicker for growth. Equally typical for a rare Quality corporate wealth generator, management at the firm is using this year's additional windfall to spend more on R&D and new product development.

Plenty of companies would be discussing a higher dividend, or a share buyback, or both, but genuine Quality thinks longer term, and realises tomorrow's growth is built on the seeds planted today. Back in 2008, TechnologyOne's offering consisted of 11 products. Today, the product suite tally stands at 16, with over 400 modules.

How to be 'special'

Officially, TechnologyOne is an IT services provider, conveniently lobbed in the same Software & Services basket with dozens of other ASX-listed ‘peers’. In practice, the company delivers mission-critical products and services, often specifically tailored for corporate clients in targeted sectors of financial services, utilities, government, education, and health.

Clients have proven extremely sticky with annual churn remaining below 1% throughout most of the past two decades. Recently, the percentage of client losses has increased with management indicating it'll probably end up around 1.60% for the running financial year as smaller businesses shy away from migrating to the cloud while clients of UK acquisition Scientia are proving less loyal.

Acquiring Scientia has provided TechnologyOne with the opportunity to sell its enterprise resource planning (ERP) solutions to circa 100 Scientia customers in the UK. At the time of the purchase, Scientia was not yet profitable. It is marginally profitable today and contributing positively through a 20% rise in ARR in the UK.

As one would expect, TechnologyOne is highly cash generative, virtually debt-free, and it pays out a steadily growing dividend, though its high valuation means the stock never features for your typical yield/income investor. Financial metrics are persistently among the better performers in the market. Last financial year's Return on Equity (RoE) was above 41%, with Return on Invested Capital (RoIC) above 36%.

.png)

Maybe one of the biggest surprises is, after all these years of market-beating performances, the company's market capitalisation only recently surpassed the $5 billion as shares responded favourably to the recent financial result. In other words: despite all the accolades, TechnologyOne still is a relatively small fish in a big ocean where multi-national competitors such as ServiceNow, Workday, SAP, Salesforce and Oracle roam around like big whales.

Management usually flags double-digit growth ahead, say between 10%-15%, and rarely disappoints. In fact, so consistent has performance been, it attracted a report from a foreign based short seller in 2020 whose attack was mainly based around the premise that no company is ever able to perform as consistently over such a long period of time.

Waiting for a cheap entry point is a lost opportunity

Becoming a true Quality stalwart, and receiving market recognition, takes time.

Investors will be wasting their time if the strategy consists of only buying stocks on a below-market average valuation. Stocks like TechnologyOne don't trade on low double-digit multiples, let alone single digits, unless a meteor hits their headquarters or something extraordinary destroys the business case.

I believe markets have become smarter in distinguishing companies with valuable quality characteristics, as experiences and performances accumulate, and there's more sophistication, and appreciation, for companies supported by a long runway of growth - for as long as the market believes that runway remains intact.

As things are lined up post FY23 interim result, the odds remain in favour of TechnologyOne continuing its pathway of growing at 10%-15% for longer, with FY23 expected to outperform. Most analysts assume EPS growth for FY23 will beat the top of that range and come in at 17% or 18% instead.

The current forecast, expressed with confidence, is that today's business will be double its current size in five years' time.

The conundrum for today's investor is the shares are now trading at a sizable premium versus the broader market, as also illustrated by the fact upgraded price targets and valuations remain below today's share price, with one exception (Wilsons, $18.12).

But if in five years' time the size of the company will be 100% higher, including the profits accompanied by continuously rising dividends, then the share price will reflect this too. TechnologyOne management is confident economic recession in Europe, the UK or the US will not have a significant impact on the current growth trajectory, which adds yet another reason as to why the shares are unlikely to sell off anytime soon (unlike so many others).

TechnologyOne might be ‘special’, it is truly difficult arguing it is not, the company is by no means unique. Research by W.P Carey School of Business Professor Hendrik Bessembinder already established there is a select group of companies worldwide that is able to provide sustainable shareholder rewards over long periods of time.

If ever Bessembinder focuses his research on the Australian share market, there should be no doubt TechnologyOne will feature in his local selection, alongside the likes of CSL (CSL) and REA Group (REA); larger cap stocks that tend to create similar dilemmas and end outcomes for investors.

In all cases, ‘value’ will always be in the eyes of the beholder rather than in a simple multiple of next year's forecast earnings per share. The question for investors is merely whether they'd like to get on board, and at what price, assuming the market offers them that opportunity.

Those already on board can simply take regular volatility for what it is with the understanding that true Quality beats a cheap price in the long run, plus it also acts as a safe haven when conditions get really, really rough.

Rudi Filapek-Vandyck is Editor at the FNArena newsletter, see www.fnarena.com. This article has been prepared for educational purposes and is not meant to be a substitute for tailored financial advice.