The Weekend Edition includes a market update plus Morningstar adds links to two of its most popular articles from the week. We also cover the Sohn Conference where 13 prominent fund managers picked their highest-conviction stocks.

Weekend market update

From AAP Netdesk: Energy shares and the oil price had an end-of-week surge but the Omicron threat sent the Australian market down by 0.5% for its fourth consecutive week of decline. On Friday, Oil Search rose 2.6% and Santos gained 1.6%, while ANZ, NAB and Westpac each rose a little more than 1%. The benchmark S&P/ASX200 index closed up 16 points, or 0.2% to 7,241 points on the day. BHP shares were up 1.3% after the board decided to go ahead with unifying its corporate structure and shares across three stock exchanges. Among other miners, Rio Tinto improved 1.4% but Fortescue slipped 0.9%.

From Shane Oliver, AMP Capital: For the week, US shares fell 1.2%, Eurozone shares lost 0.5% and Japanese shares fell 2.5% but Chinese shares rose 0.8%. 10-year bond yields fell on safe haven buying and a concern the Fed may start to tighten too early. The $A fell to its lowest since November 2020 on global growth concerns and as the $US rose due to haven demand and expectations for a faster Fed taper.

It’s still too early to know how big a problem Omicron is. While it's more transmissible than Delta with a higher risk of reinfection, it's still not known if it results in severe infections or if it has an impact on vaccine effectiveness. Ultimately, this downside is likely to be limited and turned around as central banks and governments would yet again provide more support (prioritising growth over inflation concerns). We should get a better idea in the next week or two.

***

Two recent discussions with retirees demonstrated to me why policy change is difficult, and why meaningful action demands a politician who can tell a convincing story when faced with the inevitable opposition. It's not enough that a policy is good for the nation if voters cannot be persuaded, and these days there are unlimited public platforms for vested interests.

In the first instance, the organisers of a large group of retirees who gather each month with a guest speaker asked me to present on my proposal that the family home be included in the age pension assets test, subject to a threshold. I expected a hostile response but one question in particular illustrated the difficulties explaining the nuances. The question went something like:

"I strongly disagree with you. My mother has never had any money, she bought her house for $100,000 over 50 years ago and still lives there. She's not wealthy and you're suggesting her age pension should be taken away from her."

To which I responded: "How much is the house worth now and does she still have a loan?"

He replied, perhaps too pleased by how well his mother has done given the context of the point I was making. "About $4 million, no loan," he said.

Here's where the 'agree to disagree' kicked in. I responded:

"So I think someone with an asset worth $4 million and no debt is wealthy and welfare should be reserved for poor people. The amount she is paid in a pension should be claimed against the value of her estate when she dies. Instead of you inheriting $4 million, you will inherit only $3.8 million. I don't think anyone will feel sorry for you."

Which did not go down well, and that's how policy stalls. The debt would not be repaid by his mother, it would effectively be repaid by him (and other heirs). This policy has no chance of adoption for a long time.

In the second instance, a retiree was telling me about the amazing values of houses in her street. Her home was now worth over $3 million but it was too big and the garden was a pain to maintain. She wanted to move to a nearby $2 million townhouse which suited her circumstances while staying in her community. Then the party pooper (me) stepped in.

"Do you realise that if you're on an age pension and you sell your house for $3 million and spend $2 million on a new home and put $1 million in the bank, you will lose all your pension and the related entitlements?"

She looked shocked. She said she and her husband were on the full age pension and why should they lose it just because they moved to a house that better suited them? Then she said she would just give the cash to her children as the pension was plenty to live on. She was even more surprised when I explained the gifting rules and money she gives away (above $10,000 a year or $30,000 in any five-year period) would still be counted in the assets test ... not that I'm a financial adviser.

And so this large house which should be released for a next generation family will be held by the elderly couple who will struggle up and down the stairs, slip on the leaves covering their long driveway and ponder their empty rooms. That's two families living in inappropriate accommodation because no politician will touch this sacred cow.

Central banks, interest rates and housing

Last week threw several spanners in the works for investors who watch markets closely, and not only due to the unknowns of Omicron. US Federal Reserve Chair, Jay Powell, moved more to the dark side by suggesting inflation will not be transitory, implying less monetary policy accommodation. Given his new term in office, he will not want to see inflation run ahead of his actions for too long.

The Fed watches inflation using the Personal Consumption Expenditure Core Price Index closely, and as shown below, Powell is right to be refocussing.

It's a complex picture with a new virus on the scene, the very factor which led to immense central bank support in 2020. The RBA's Philip Lowe is steadfast in his resolve, saying on 2 November 2021:

"In our central scenario, underlying inflation reaches the midpoint of the 2 to 3% range only in late 2023. Having underlying inflation reach the midpoint of the target range for the first time in seven years does not, by itself, warrant an increase in the cash rate."

So while the housing market has seen a rapid increase in supply as sellers look for the top before the end of 2021, there is still plenty of demand, with auction clearance rates holding up.

This week's White Paper from Shane Oliver of AMP Capital supports his view that house prices are expected to slow to 5% growth in 2022 then fall 5-10% in 2023, mirroring Lowe's cash rate changes.

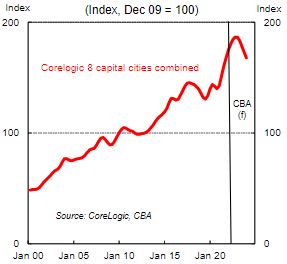

Gareth Aird of CBA expects cash rate changes earlier, and he says:

"Our expectation for the RBA to commence normalising the cash rate in November 2022 means that we expect national dwelling prices to peak in late 2022 around 7% higher than end 2021 levels. We expect an orderly correction in home prices of around 10% in 2023 as the RBA takes the cash rate to 1.25% by Q3 2023."

Australian dwelling prices and CBA forecasts

Prudential regulators allowed the market to run too strongly over late 2020 and this year with 2021 house prices up around 26% in Sydney, Brisbane and Canberra. Financial stability should not be a boom and bust which pushes thousands out of the housing market while making others even wealthier, and encouraging those who enter the market to take on vast amounts of debt and struggle to withstand rate rises.

In this week's packed edition ...

The Sohn Australia Conference brings together leading fund managers to chose their highest conviction stock in a 10-minute pitch. We list their 2021 selections plus Charlie Munger's wisdom as the star feature.

While many investors spend their time picking stocks, asset allocation in their overall portfolio makes a larger contribution to total returns than a few stock winners. In this interview, John Woods explains how he has tilted multi-asset portfolios to alternatives in the face of low interest rates, and why ethical investing is not simply about screening out of few bad apples.

Phil La Greca continues this theme by showing why the ATO asset allocations for SMSFs often quoted by the media and fund managers are nonsense, not only out-of-date, but wrong on major items such as cash and global equities. Don't take the ATO data as a guide to what SMSFs are doing. FWIW, balances reported for SMSFs at the end of the September quarter were $861 billion, a rise of a whopping $162 billion in a year. No signs of SMSFs slowing.

In the second report from our recent Reader Survey on advice for younger people, Leisa Bell selects a dozen highlights, but these do not do justice to the many other excellent ideas from our smart readers. So we also attach a PDF with all the responses.

Fund managers cannot be experts in everything, and James Tsinidis says they select 'Areas of Interest' where they expect the future payoffs according to their S-curve approach. Having backed technology plays such as smartphones and cloud computing, they are now putting more money into climate change, and he describes their four main themes in looking for the next big thing.

With Omicron adding to the market jitters already caused by macro factors and central bank dithering, Roger Montgomery puts the inflation cat back in the bag saying that even if it is high for much of 2021 and into 2022, the long-term trends pushing prices down are still in play and Fear, Uncertainty and Doubt (FUD) will create opportunities later.

John Julian then explains why infrastructure assets are not all alike, and there are many roads to recovery for these long-term assets to play a role in most portfolios.

There is so much data in financial markets every day that it's easy for investors to become distracted by the noise. Andrew Canobi and his colleagues pick out three prices worth following, if not daily or weekly but to at least understand where they are going over time.

Green hydrogen is all over the news, backed strongly by PM Scott Morrison and high-profile businessmen such as Andrew Forrest. But what is it, and why are they excited? Michael Collins finds the energy source may have a strong future but the technology is not simple to adopt.

And for the thousands of you who own investment properties, Tuan Duong explains tax deductions and depreciation allowances under Divisions 40 and 43, reminding us that the returns from investment properties rely heavily on making the right tax claims.

Two bonus articles from Morningstar for the weekend as selected by Editorial Manager Emma Rapaport.

Remember the FAANGs? Facebook (Meta), Apple, Amazon, Netflix and Google (Alphabet). It seems they've fallen out of favour, contributing 2.7% to US market returns in 2021, down from 24% in 2020, writes Tom Lauricella. And Lewis Jackson speaks to Lazard's Aaron Binsted about his three top picks for the energy transition.

Last Thursday was the final time Fran Kelly will host the Breakfast programme on ABC's Radio National. I have woken up to Fran for most of the last 17 years, when she often asked the questions I had in my head. I can only imagine the strain of rising in the middle of the night to prepare a programme to be at the top of her game by 6am. Well done, great effort. Here's the last word from Fran:

“My alarm goes off at 3.30am, so I would be lying if I did not say that I am looking forward to some sleep-ins. I am going to take a couple of months off and then reappear, energised and ready for some new projects.”

Graham Hand, Managing Editor

Latest updates

PDF version of Firstlinks Newsletter

IAM Capital Markets' Weekly Market Insight

ASX Listed Bond and Hybrid rate sheet from NAB/nabtrade

Indicative Listed Investment Company (LIC) NTA Report from Bell Potter

LIC Quarterly Report from Bell Potter

Plus updates and announcements on the Sponsor Noticeboard on our website