The Weekend Edition includes a market update plus Morningstar adds links to two additional articles.

Though it dithered for a long time, the Federal Government has delivered its final response to the Quality of Advice Review (QAR). The Government proposes to implement most of the QAR’s recommendations, though not all of them.

Noone is completely happy with the measures, barring some super funds, yet the Government needs to be given credit for trying to fix the financial advice system. Something needed to be done to wind back some of the reforms of the Hayne Royal Commission that’s decimated the advice industry and left millions of Australians without the advice they desperately need. Whether Labor’s policies will provide all the answers will depend on upcoming consultation and the draft legislation tabled next year.

New research shows why change has to happen

That Labor has pulled the trigger on reforms is testament to the urgency of the problems.

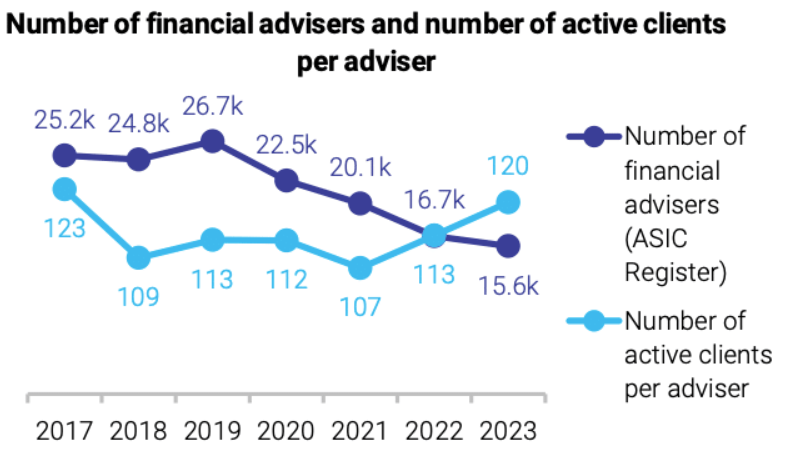

Financial advice has become incredibly expensive because the industry is chronically undersupplied. Since the Hayne Royal Commission, around 11,000 financial advisers have left the industry. Causes for this include greater administrative red tape and increased educational requirements. All the while, demand for advice has exploded.

Source: Investment Trends

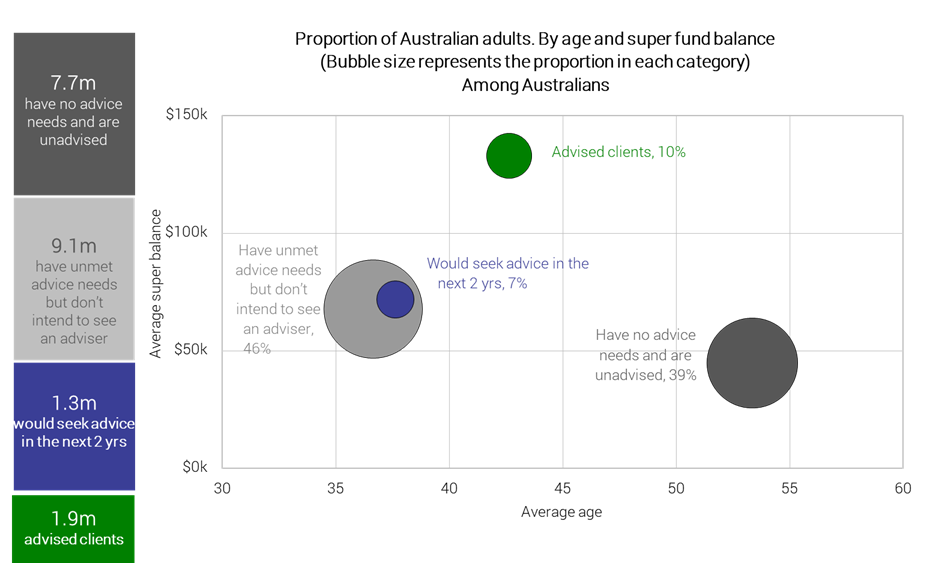

Yet not nearly enough of that demand is being met. New research from Investment Trends suggests 11.8 million Australians have unmet advice needs. Breaking that down further, 9.1 million people have unmet needs but don’t intend to see an adviser. 1.3 million want to seek advice in the next two year. And, out of the 1.9 million advised clients, 1.4 million of them have unmet needs of some kind.

Source: Investment Trends

The research suggests that the barriers to seeking advice include high (41%) or unclear (30%) costs. And that the top three areas where people would like to get financial advice, but currently aren’t, include:

- Investment strategy (41%)

- Longevity risk (33%)

- Growing their superannuation (30%)

The research also shows that Australians receiving advice feel better off financially and are significantly more prepared for retirement than the unadvised. Around 61% of those who have an adviser feel more confident in their financial wellbeing. And 57% of advised people feel more confident in preparing for retirement.

Finally, Investment Trends says 44% of unadvised Australians are likely to turn to their super fund for their unmet advice needs.

The demand for advice is expected to significantly increase with around 3.6 million Australians retiring during the next decade. That means the supply of advice needs to ramp up quickly to meet that need.

What the Government intends to do about it

In its final response to the QAR, the Government proposes to do the following:

1. Introduce a ‘best interests’ duty that will apply to all providers of personal advice.

This new duty will remove the so-called ‘safe harbour’ steps. It will also keep the existing obligations to act in the best interests of clients and prioritise the interests of clients in the case of a conflict. Yet it will give clearer legislation for scaled or limited scope advice.

The Government chose not to go with a ‘good advice’ duty as recommended in the QAR. Financial Services Minister Stephen Jones says this is because, ‘Australians deserve the best, not just good’.

But Mr Jones says that advisers will have greater flexibility to provide limited advice on specific subjects, provided it’s appropriate in the circumstances.

Clearly, the measure aims to allow more personal advice to be given to more people and to reduce the complexity of current obligations. How this works in practice will depend on how it’s legislated.

2. Introduce a new class of financial advice provider called ‘qualified advisers’.

The Government says this is intended to increase the availability and affordability of simple financial advice.

A qualified adviser will be able to give personal advice on less complex matters. They won’t be able to charge a fee or commission for their services and therefore will likely work for a licensed financial institution. And they’ll be required to have minimum educational standards, most likely a diploma.

A qualified adviser will be subject to the best interests duty described above. This advice model will be available to all financial institutions including banks, super funds, and insurance companies.

The Government’s proposal provides stricter minimum education standards than that recommended by the QAR. But how the new class of ‘qualified advisers’ fits in with the current batch of advisers is an open question. Also, the different classes of advisers have the potential to confuse the end-consumer of financial advice.

In saying that, the measure could allow for more simple advice for those at key stages, both before and after retirement. And it might pave the way for greater use of digital advice.

3. Replace Statements of Advice with a ‘principles-based’ advice record

The administrative burden of Statements of Advice has been a source of irritation for advisers for some time. This is probably the one measure that’s been universally welcomed.

4. Expand superannuation advice

The Government proposes to:

- Legislate a list of topics that can be charged to a super fund member’s account. The topics will include advice on retirement incomes and investment decisions.

- Give certainty to funds to give members ‘personalized nudges’, such as switching super into a pension account at the appropriate time.

- Allow funds to consider a greater range of a member’s circumstances such as spousal income, debt, and age pension liability.

This measure aims to ease super fund fears about providing advice to its members. Whether there are enough protections for consumers is a matter of debate.

Reactions to the Government’s proposals

Reactions to the Government’s reforms has been decidedly mixed. QAR Chair Michelle Levy says:

“There is enough here to make a big difference – it will go a long way to making advice more accessible and more affordable.”

Most of the super funds are happy, suggesting the changes including the new class of advisers and removal of red tape will increase access to advice to lower and middle-income Australians.

The Financial Services Council, which represents larger financial companies, says its research suggests that removing the safe harbour provision and simplifying disclosure could cut advice costs by 40%.

Consumer groups also cautiously welcomed the Government’s measures. Acting Director of Super Consumers Australia, Gerard Brody, says it’s positive that the Government will introduce a best interests’ duty for personal advice, rather than the weaker ‘good advice’ duty recommended by the QAR. Though it’s wary of potential conflicts of interest in advice provided by banks, insurers, and super funds.

However, The Financial Advice Association isn’t so happy. CEO Sarah Abood fears that it winds back the clock for the industry and invalidates the hard work of advisers to improve standards since the Hayne Royal Commission. She’s especially concerned about the new class of ‘qualified advisers’, who won’t have the same qualifications as current advisers. Ms Abood thinks the different classes of advisers will confuse current and potential advice customers.

Ms Abood’s concerns have merit though some of them should be clarified before the legislation is finalised.

Where to from here?

After a consultation period in coming months, draft legislation should be tabled later next year. Hopefully, the ambiguities in the current proposals can be resolved so the advice industry can help more people with their financial needs.

***

Most assets classes have bounced back this year after a horrid 2022. But where are the best opportunities for 2024? In my article this week, I compare valuations for cash, bonds, residential property, and stocks, and reveal what's cheap and what's not.

James Gruber

Also In this week's edition...

Kaye Fallick says retirement is the new black and super funds are seemingly expected to do all things for all retirees. She asks wehther we need to better apportion the different responsibilities to create a world class retirement income system.

Meanwhile, Andrew Gale and Stephen Hubbert agree that our retirement system needs change. They think greater work flexibility and access to equity in their homes would allow people to better plan their futures and fund their lifestyles.

It's great to welcome back Don Stammer to Firstlinks. For each of the past 42 years, he's selected the X-factor - the largely unexpected influence that wasn’t thought about when the year began but came from left field to have powerful effects on investment returns. Today, Don announces this year's winner.

In recent years, investors have loaded up on bank hybrids, and some are getting nervous by an APRA review into the securities. Professor Kevin Davis says they are right to be nervous as hybrids don't work for the purpose that they are designed, and their continued use must be questioned.

Investors have crowded into cash this year. Capital Group's Winnie Kwan warns that cash typically underperforms when interest rates peak. She suggests equities are a better bet, and likes companies flying under the radar, including ones benefitting from integrating artificial intelligence into their operations.

In the Wealth of Experience podcast this week, Brandywine Global's Richard Rauch warns of US and global recession risks, Vanguard's Duncan Burns looks at the best way to build a simple, effective investment portfolio, and Peter Warnes gives his Australian market outlook for 2024.

Two extra articles from Morningstar for the weekend. Shane Ponraj examines Sigma's acquistion of Chemist Warehouse, while Shani Jayamnne looks at an A-REIT that's 33% undervalued.

Finally, in this week's whitepaper, Cromwell Property Group's Colin Mackay has a case study on the flight to quality in office property.

***

Weekend market update

On Friday in the US, new highs in the Nasdaq 100 headlined the day after the tech-heavy index advanced 50 basis points to extend year-to-date gains to 53.3%, though the S&P 500 skipped today’s party with a slightly red finish. The long bond settled at 4% from 4.03% a day ago for its best finish since July, as the short end took a break from the recent euphoria, bouncing seven basis points to 4.44%. WTI crude held just below $72 a barrel, gold slipped to $2,019 per ounce and the VIX stayed below 13.

From AAP Netdesk:

The Santa rally appears to be coming early this year, with the local bourse rising on Friday for a sixth straight day in its second-best week of the year. The S&P/ASX200 index on Friday finished up 64.8 points, or 0.88%, to 7,442.7, while the broader All Ordinaries rose 62.5 points, or 0.82%, to 7,661.9. For the week, the ASX200 gained 3.44%, its best weekly performance since a 3.7% gain in mid-July.

Eight of the ASX's 11 sectors finished higher on Friday, with energy and mining the biggest gainers, rising 1.9%. BHP rose 2.4% to an 11-month high of $49.41, Fortescue climbed 1.4% to an all-time high of $27.85 and Rio Tinto added 2.2% to a two and a half year high of $132.86.

In the energy sector, Santos advanced 3.2% to a six-week high of $7.75, Woodside added 1.4% to a week and a half high of $30.58 and Whitehaven Coal rose 0.8% to $7.19.

All of the Big Four banks finished higher, with ANZ adding 1.2% to $25.54, Westpac rising 0.9% to $22.49, NAB climbing 0.8% to $30.18 and CBA finishing 0.5% higher at $110.07.

Both Healius and Australian Clinical Labs finished 0.7% lower after the latter withdrew its takeover bid for the former in what would have been a tie-up between the No. 3 and No. 2 pathology chains in Australia. The competition regulator on Friday moved to block the proposed acquisition but ACL said its change of heart was motivated by a deterioration in Healius' trading performance and its recent $187 million capital raising.

Adbri rose 8.6% to $2.27 after the cement manufacturer moderately raised its full-year guidance, saying it had experienced strong demand for its products in the second half. Adbri also advised that a roughly $400 million project to upgrade its cement plant in Kwinana, Western Australia, was on track to be completed by the second quarter of next year.

From Shane Oliver, AMP:

- More good news on interest rates, with key central banks leaving rates on hold and the Fed pivoting towards interest rate cuts. The past week saw a raft of central banks – the Fed, the ECB, the BoE along with central banks in Switzerland, the Philippines and Taiwan – all leave interest rates on hold. The Norwegian central bank surprisingly raised rates but signalled that rates are now likely on hold. And the Brazilian central bank cut rates. It’s now looking almost certain that rates have peaked in major central banks and they are moving towards rate cuts. This is all being driven by the ongoing fall in inflation, with US CPI inflation falling again in the last week and a bigger than expected fall in producer price inflation. Of course, some central banks are moving faster than others.

- The Fed is the most dovish arguably reflecting the fact that its inflation rate peaked in June 2022 which was several months ahead of other countries (October 2022 for the Eurozone and UK and December 2022 in Australia) and so its seen a longer period of slowing. It held rates at 5.25-5.5% as expected but has become dovish in noting that growth and inflation have slowed, is now referring to what will determine “any” additional tightening, has started to discuss rate cuts and its dot plot of Fed officials’ interest rate forecasts is now allowing for three rate cuts next year. We expect the Fed to start cutting interest rates in the June quarter.

- The ECB held rates at 4.5% and moved to be a bit less hawkish with President Lagarde dropping guidance that it would not cut rates in the next two quarters but sounding more hawkish than expected and unlike the Fed is yet to discuss rate cuts. Quite clearly the ECB is a bit concerned that market expectations for rate cuts have moved too quickly and it wants to damp it down. That said, with the Eurozone in or close to a mild recession and inflation likely to fall further we see it starting to cut rates in April.

- The BoE held at 5.25% and was understandably a bit more hawkish given its higher inflation rate and wages growth above 7%yoy. However, with the economy weakening and inflation likely to slow further, it's likely to start cutting around mid-2024.

- The peaking in global interest rates and shift towards rate cuts led by the Fed is a good sign for the RBA. Just as Australian inflation and interest rates lagged the pickup in US/global inflation and interest rates by a few months its likely to also do the same on the way down. So the fact that the US is moving towards rate cuts suggests that the RBA will likely do the same with a lag. While there is still a high risk of another RBA rate hike early next year, its likely to be headed off by weaker inflation for December and the pivot towards rate cuts globally. Our base case remains that the cash rate has peaked and that the RBA will start cutting rates mid next year taking the cash rate down to 3.6% by end 2024 (which is below market expectations for a fall in the cash rate to 3.8% by end 2024).

PDF version of Firstlinks Newsletter