The Weekend Edition includes a market update plus Morningstar adds links to two additional articles.

Recent earnings results from the US tech giants were eye-opening. Alphabet and Microsoft reported net profits of US$24 billion and US$22 billion respectively for the March quarter alone. That dwarfs what our largest stock, BHP, earns in a whole year (US$14 billion).

Though the ‘Magnificent Seven’ tech stocks have somewhat given concerns about the pace of Fed rate cuts, their aggregate market capitalization of close to US$13 trillion is still larger than the world’s third, fourth and fifth economies (Germany, Japan, and India) combined.

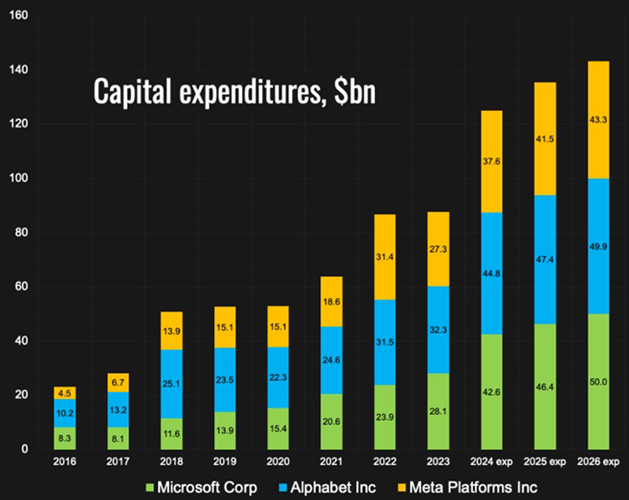

Here’s another statistic for you: Microsoft, Alphabet, and Meta, will spend more on capital expenditure (capex) than the entire private sector in Australia. Those tech giants are forecast to spend a total of US$115 billion in capex, compared to our private sector’s US$114.6 billion.

Source: LSEG

BHP is looking to spend US$10 billion in capex this financial year, while the ASX’s second largest stock, CSL, is forecasting US$800 million.

The capex figures do make me wonder whether the dividend fetish of Australian companies and investors may be good for shareholders but bad for the country. That is, increased investment could drive greater economic growth and productivity.

And our focus on dividends may not even be positive for shareholders. As Roger Montgomery argued in Firstlinks late last year, the ASX 200 has essentially gone nowhere over the past 16 years, while the US market has boomed. And he puts the blame on high dividend payout ratios aided by Australia’s favourable dividend imputation system.

Granted, comparing Australia to the US isn’t an apples-to-apples comparison. The ASX relies on banks and miners, the former a mature and the latter a highly cyclical one. Investment in these sectors can’t be expected to keep up with the likes of tech.

Though the issue warrants greater debate.

***

You’ve got to hand it to the $223 billion Future Fund – it’s nailed several calls of late. In September 2021, 18 months into the pandemic, it wrote a paper suggesting that a new world investment order was emerging. It detailed 10 paradigm shifts including deglobalization, increased populism, higher inflation, and bonds providing less downside protection in an inflationary world.

In December 2022, it followed up with another paper asking whether we were witnessing the death of traditional portfolio construction - that is, whether the paradigm shifts it detailed previously were making long-held approaches redundant. It noted how its portfolio had changed to reflect these shifts, including adding more private equity to increase potential returns, greater exposure to inflation hedges such as commodities, including gold, and infrastructure, and holding a broader basket of currencies due to growing risks from deglobalization and geopolitics.

Fast forward to today, and higher than expected inflation is again rearing its head, leading to potential rate cuts in Australia and other developed markets being pushed back. Bonds have been smashed this year again, making it the longest bear market ever for the asset. Meanwhile, gold has proved a useful inflation hedge, as have other commodities such as oil and copper.

The portfolio changes have allowed the Future Fund to deliver decent recent returns. In the first three months of this year, assets grew by $11.5 billion, for a 5.4% return. And the fund is on track for an annual return for the 2024 financial year of 8.3%. The fund has 37% of its assets in listed equities, 33% in debt securities, cash and alternative investments, and 30% in real estate, private equity, and infrastructure.

In its latest update, the fund highlighted that it still sees sticky inflation ahead. It also pointed to credit investments as attractively priced in a world of persistently higher rates.

***

The most significant, yet underappreciated, story in global markets over the past few weeks has been the sharp fall in the Japanese Yen. Briefly, the Yen weakened to 160 against the US dollar for the first time since 1990. About 2.5 hours after that milestone was reached, the Yen quickly cratered 2.5% - a seismic move in currency terms. There was unconfirmed speculation of government intervention to prop up the currency.

As for what caused the initial decline in the Yen, there’s little doubt that higher than expected US inflation and reduced expectations for rates cuts there have helped the US dollar and pressured other currencies.

Source: Trading Economics

Japan is a unique case because of its tenuous economy and government finances. Clime’s John Abernethy recently wrote of how Japan’s net government debt of 250% of GDP makes it the king of debt in a highly indebted world. He said:

“The experience of Japan is incisive because it shows that money printing (QE) does not necessarily cause either inflation, severe devaluation or economic calamity. Indeed, it suggests that QE is a viable (but not yet well-understood) economic tool.”

I don’t agree with John here as the unintended consequences of Japan’s unconventional policies may be ahead, rather than behind us. The debate makes the Yen’s latest moves a fascinating watch.

What the Yen’s decline also does though is put enormous pressure on other major exporters such as China and South Korea. A large fall in the Yen, as has just happened, makes Japan’s exports much more attractive vis-à-vis its neighbours.

China is already dealing with a property hangover that’s curtailing economic growth. Now, its biggest rival threatens to take market share in goods exported to consumers in a booming US economy.

As Martin Dropkin, Fidelity’s Head of Equities, Asia Pacific, suggested in a recent media briefing in Sydney, the question is whether China will weaken or devalue the Yuan to make its exporters more competitive. It would be a huge move that would anger the US, and risk escalating trade wars.

***

In my article this week, I look at how growth investors are using Buffett and Munger to justify buying blue chip stocks, at almost any price. It’s a recipe for potential disaster, as investors in market darlings like CBA and Cochlear may be about to find out.

James Gruber

Also in this week's edition...

Australia's population is not only growing fast, but our cities are becoming denser. Surprisingly, Melbourne and Adelaide top Sydney in terms of density for capital cities. This and other trends are analysed by Tim Lawless, and he also explores the implications for the housing market.

Liam Shorte returns with another definitive guide for SMSFs and other super funds for end of financial year matters. He provides a 24 point checklist of the most important issues to address.

Nvidia has taken the world by storm over the past year, yet there are a lucky few who've been invested in the stock for a long time. One of them is Alex Pollak from Loftus Peak, who first bought Nvidia shares back in 2016. He details his original investment case eight years ago, how it's evolved, and what he foresees for the company in the coming years.

In an era where growth companies dominate and the likes of Nvidia grab all of the attention, dividend paying stocks are flying under the radar. However, Eric Marais from Orbis says some of these stocks are now worth a look as they offer compelling potential returns.

Australia may be a rich country, yet like a lot of developed countries, measures of happiness among its people are flat or going backwards. Some economists think that we need to focus less on GDP and more on broader measures of well being. AMP's Shane Oliver delves into these issues and whether change is needed.

After more than a decade of pitiful yields, bonds are back offering better prospects for income investors. What are the best ways to take advantage of the market inefficiencies in Australian fixed income? Western Asset Management's Jonathan Costello has some ideas for you.

Two extra articles from Morningstar for the weekend. Joseph Taylor identifies two undervalued ASX stocks in a beaten down sector, while Seth Goldstein gives his latest take on Tesla.

Finally, in this week's whitepaper, Anthony Doyle from Firetrail, a Pinnacle affiliate, analyses why demand for electric vehicles has stalled.

***

Weekend market update

On Friday in the US, a softer-than-expected April payrolls report spurred a bull stampede, as the S&P 500 jumped 1.25% to edge back into positive territory for the week, while the VIX settled below 14 for the first time since late March. Treasurys were likewise bid as 2- and 30-year yields each dropped six basis points on the day to 4.81% and 4.66%, respectively, WTI crude slipped to US$78 a barrel and gold remained at just over US$2,300 per ounce.

From AAP Netdesk:

The local share market on Friday finished higher for the fourth time this week, with every sector in the green as traders continued to parse the tea leaves from a Federal Reserve meeting. The benchmark S&P/ASX200 index on Friday finished 42 points, or 0.55%, higher at 7,629.0, while the broader All Ordinaries rose 48.1 points, or 0.61%, to 7,897.5. For the week, the ASX200 rose 0.7%, its second week of gains.

The consumer discretionary sector was the biggest gainer on Friday, closing up 2%, with Wesfarmers rising 2.8% to $68.31 as investors pondered presentations from the conglomerate's strategy day sessions on Thursday.

Elsewhere in the sector, Temple & Webster rose 5%, Star Entertainment Group rebounded by 6.1% and Lovisa added 2.7%.

In the heavyweight mining sector, goldminers were well in the red as the precious metal dipped. Evolution fell 5.6%, Bellevue Gold slipped 3.2% and Resolute Mining dropped 4.6%.

Elsewhere in the sector, BHP and Rio Tinto both edged 0.1% higher, at $42.41 and $129.24, respectively, while Fortescue rose 0.4% to $25.66.

All of the Big Four banks finished higher, with Westpac rising 1.5% to $26.42, ANZ adding 0.9% to $28.48, NAB growing 0.4% to $34.40 and CBA finishing up 0.2% at $115.23. But Macquarie dropped 2.2% to $183.83 after announcing its full-year net profit had dropped by nearly a third to $3.5 billion.

Looking forward, the Reserve Bank is expected to leave interest rates on hold at 4.35% when it meets on Tuesday.

From Shane Oliver, AMP:

- Fed confirms that rates will stay high for longer, but it was less hawkish than feared. There was nothing really new in the Fed and Chair Powell indicating that recent data has shown a “lack of further progress” in getting inflation down and that it will take “longer than expected” for the Fed to get confidence that inflation is on track for its 2% target in order to cut rates. But Powell also indicated a rate hike was unlikely, policy is restrictive, and he is seeing strong data in the context of improving supply enabling labour market tightness to continue to ease. So overall it remains a case of rate cuts delayed rather than anything more threatening. Our base case remains for the first Fed cut to come in September.

- Is the US heading into stagflation or just getting back on track? Expectations for imminent and big interest rate cuts earlier this year were dashed in the US as economic data and inflation surprised on the upside. This was initially seen as okay for share markets because stronger than expected growth and profits offset the downside from high for longer interest rates. It started to sour in the last month though as worries about overheating led to concern the Fed and maybe even the RBA will have to raise rates further. Data over the last few weeks though showing slowing US growth (weaker GDP, weaker business surveys, falls in consumer confidence and falling forward jobs indicators) at the same time that inflation indicators (CPI, core private final consumption deflator and employment cost index) have picked up have led to new a concern – that of stagflation which as the 1970s reminds us is bad for both shares and bonds. Our assessment though is that any stagflation is likely to be short lived and rather see the cooling in growth as a sign that inflation will soon start to slow again too. Inflation normally lags growth so there is often a brief part in the cycle where it looks like stagflation before inflation catches up to slower growth. In other words, the US economy is likely getting back on track for a cooling which will enable the Fed to ease latter this year. Australia is likely to follow the same path.

- In Australia, while there has been much talk of a resumption of rate hikes after the hot March quarter inflation data our view remains that the RBA will leave rates on hold on Tuesday ahead of a delayed start to cuts later this year. A resumption of soft retail sales after seasonal distortions and a temporary Swift lift indicate the consumer remains under pressure and that high rates are working to slow demand which will continue to take pressure off inflation.

- The 2024-25 Australian Budget (14 May) looks like its going to be mainly about getting “Future Made in Australia” protectionism underway. Key features are likely to be:

- A combination of subsidies, tax breaks, cheap loans and relaxed foreign investment rules to encourage investment in government chosen industries in a (“nostalgic”) return to post war protectionism and picking winners as part of the “Future Made in Australia” policy.

- Minimal cost of living measures for low to middle income workers, including an extension off energy bill relief.

- A renewed talking up of the benefits to low and middle income households from the rejigged Stage 3 tax (worth $1929pa for someone on $90,000pa).

- Possibly further measures to slow structural spending growth, to better allow for a slowdown in windfall revenue gains.

- Net immigration of 450,000 this financial year up from a MYEFO forecast of 375,000, falling to 250,000 in 2024-25.

- A budget surplus of around $10-15bn this financial year thanks to higher than forecast commodity prices and personal tax collections, but a return to a deficit of around $12bn in 2024-25. March budget data shows a financial year to date deficit of just $2bn which is $4bn better than projected in MYEFO. As its tracking better than the 2022-23 budget profile another $22bn plus deficit is possible. See the next chart.

- The 2023-24 GDP growth forecast may be revised back down to 1.5% from 1.75% with the growth forecast for 2024-25 remaining at 2.25%. Inflation forecasts are likely to remain at 3.75% for this financial year and 2.75% for next.

- The key is that with inflation proving sticky the Budget needs to take slightly more out of the economy than it puts back in so as to make the RBA’s job easier. Any spending associated cost of living relief, Future Made in Australia subsidies or other measures should be more than offset by savings elsewhere.

Curated by James Gruber and Leisa Bell

Latest updates

PDF version of Firstlinks Newsletter

VanEck Webinar: The extra scoop advantage in Australian equities, 9 May 2024

ASX Listed Bond and Hybrid rate sheet from NAB/nabtrade

Listed Investment Company (LIC) Indicative NTA Report from Bell Potter

Plus updates and announcements on the Sponsor Noticeboard on our website