The economic impacts of the war in Iran continue to dominate headlines. Investors are following their typical playbook and rushing into the ‘obvious’ winners of the turmoil in the Middle East.

For instance, there are higher oil prices. Over the previous month the following energy companies have performed well:

- Exxon Mobil is up 12.44%

- Chevron is up 12.82%

- Shell is up 15.42%

- Santos is up 17.75%

- Woodside is up 18.51%

Yet investors viewing the market through the prism of the current challenges and opportunities arising from the geo-political mess we find ourselves are being short-sighted.

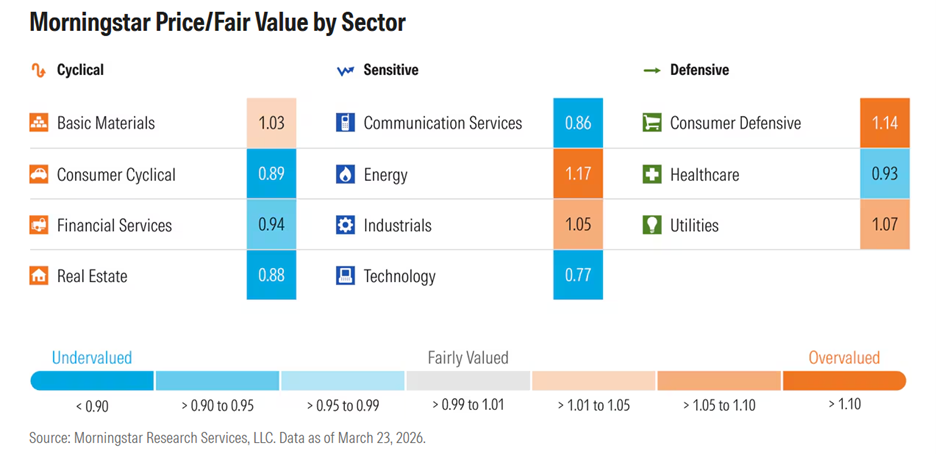

Long-term returns are driven by a mismatch between valuation and prices. The following chart shows the price to fair value on the US market according to our analysts.

The cheapest sectors are the ones most maligned in our current environment. The Technology and Communications sectors are being hit by fears about the impact of AI. Inflation concerns are driving weak performance in the Consumer Cyclical sector.

Those cheap valuations don’t mean there aren’t legitimate problems. AI is disrupting the previously strong moats of many leading companies in the software space. The longer the war goes on the greater supply chains are being impacted. As COVID demonstrated this can drive inflation which is difficult to reign back in.

Prevailing narratives may be true. But investors historically have overreacted to narratives on both the upside and downside. The constant drumbeat of headlines reinforces this tendency.

It is easy to invest using first order thinking – for example, oil is more expensive which is good for oil shares and bad for consumer spending. It is much harder to stay multiple steps ahead of our current situation.

What to do right now

Successful investors will focus on where the world will be in 10 years. That isn’t easy but it beats trying to interpret each tweet out of the White House.

Remember that when investors are anxious and there is volatility they tend to make poor decisions. Much of the advice coming from the more sober commentators is to ‘not panic.’ This is well meaning and meant to be helpful.

But people generally don’t panic. Instead, people rationalise their way into decisions that hurt their long-term interests. We describe investors as capitulating. Yet nobody would describe their own actions as capitulation. And that disconnect between how people see their actions and how they describe the actions of others matters.

Investor returns are influenced by the timing of buy and sell decisions. The gap between investment and investor returns is an indication of how poor we are at making decisions. Each poor decision is a point of failure. The cumulative impact was a 1.10% gap between investment returns and investor returns over the previous decade in Morningstar’s latest Mind the Gap study. Collectively investors are not up to the challenge in the best of times.

Given this is an annual study, the size of the gap will fluctuate each time we run a new set of data. Over time we’ve noticed several patterns. The gap widens if there is more volatility. This is evident when different types of investments have different levels of volatility—say share ETFs and bond ETFs. The investor gap is bigger for share ETFs than bond ETFs. It is also evident when different periods of time have different levels of volatility.

For instance, in 2019 the gap was around 1%. In 2020 with turbulent markets in response to COVID the gap widened to close to 2%.

You are far more likely to make a mistake in times like this. Slow down your thinking and scruitinise each decision more than you normally would. It might just pay off in the long-run.

Mark LaMonica

Also in this week's edition...

From 1 July 2026, major superannuation caps will increase due to indexation. Julie Steed outlines the rates and thresholds that are changing and those that aren’t.

Inflation continues to worry investors and policy makers. Michael Collins explores how central banks are reconsidering inflation targets.

As data mining capabilities have increased and AI has advanced, investors have sought to identify factors that led to alpha or outperformance. Larry Swedore examines a study suggesting a new mindset is needed for investors looking to generate superior returns.

Many investors believe a ‘balanced’ portfolio is the best of all possible worlds. But Werner du Preez believes hidden concentration risk may be lurking under the surface.

Investors are fleeing bonds given projections of higher inflation and a hawkish response by the RBA. Phil Strano sees some benefits for investors willing lock in attractive rates of income.

The only thing that matters is the return that ends up in your pocket. Emma Davidson looks at after-tax returns on LICs and the opportunity for LIC providers to provide more return transparency for investors.

Jow Wiggins explores the impact on decision making from an “availability cascade” as investors lose sight of the long-term while their attention is focused on each successive short-term risk.

This week's white paper from the World Gold Council looks at the role of gold in 2026 for Australian investors.

Curated by Mark LaMonica and Leisa Bell

***

Weekend market update

Two article from Morningstar this week. I took a look at the considerations for asset allocation for retirees as they attempt to acheive several goals. My colleague Sim looked at the top rated ASX pick from our analysts for every sector.

From My Bui, AMP

Financial markets were taken on a roller coaster ride this week as we started and ended the week with promises of TACOs (Trump Always Chickens Out), though it turned out that we were fed NACHOs instead (Not Actually Changing Hormuz Opening)! The previous extension of the deadline to attack Iranian energy assets to April 6th did little to calm markets heading into Monday, as the Houthis became involved in the conflict and Hormuz remained effectively shut. However, optimism has since grown as President Trump indicated he might withdraw even if the Strait stayed closed, while Iran's President also showed willingness for a ceasefire. Hopes for an end to the war reached a fever pitch by Thursday with the S&P 500 recovering all of its losses since March 26th, up 3.2% since last week and the Euro Stoxx 50 also rose 4.1%. But in the end, Trump’s much-anticipated national primetime address disappointed as it contained nothing new: Core US goals are “nearing completion”, the US will hit Iran’s electric plans if there is no deal, and in fact the speech skewed to higher escalation risks as Trump threatened to hit Iran “extremely hard” over the next 2-3 weeks. Aussie and Asian shares have now fallen again, with the ASX 200 down 6.7% from before the war and Japanese shares still down more than 10% from February.

Unsurprisingly, Brent oil prices have also been on the same rollercoaster, coming down from a peak of $118/bbl last week to below $100 intraday mid-week, before spiking again after Trump’s disappointing speech to around $107 at the moment.

Economic game theory suggests that war is very difficult to end, because while the rational choice is peace, both sides prefer to stay in the game as they fear that the other won’t stop. So, we will see a lot more noise and rhetoric around the war coming up, and it is well conceivable that we can see a 15% peak to trough fall in shares this year (which likely will force Trump to back down more meaningfully). In the meantime, the only number that matters is the count of vessels passing through the Strait of Hormuz. Over the last week, 11 ships have gone through which is a big improvement from zero back in mid-March, but most of them are not oil tankers and it is estimated that oil supply remains around 5-10% below the pre-war levels.

Now that Hormuz Strait has been closed for more than a month, even an end to the war today will see supply disruption in many sectors over the coming months. The International Energy Agency has estimated that even after the waterway fully opens, shuts in upstream production could take weeks to months to return to precrisis levels. And while the first-round impact from fuel supply is already well known at the bowser, we are yet to see higher food prices (from a shortage of fertilisers) as well as inflation in other manufactured goods (with supply issues in plastics, aluminium, or helium). In addition, similar to most cycles in history, services inflation will follow goods, especially at a time when businesses are already starting to pass all the costs to consumers through “fuel surcharges”. Furthermore, the longer the conflict goes on, the higher inflation expectations become unanchored, which forces central banks to turn more hawkish than otherwise. Reflecting these trends, we have now revised up our headline inflation forecasts for Australia to 5%yoy for the June quarter, while trimmed mean inflation is expected to peak to 4%yoy before returning to the RBA’s 2.5% target at the end of 2027.

As a result, most global central banks are now expected to hike rates with the exception of the US Federal Reserve. Earlier this week, Fed Chair Powell tempered some market expectations, indicating that the Fed would look through supply-driven oil price spikes “for now” as inflation expectations remained anchored in the US and labour market indicators continued to soften slightly. In Australia however, we now expect two more hikes in May and August. The recently released RBA minutes showed that while there was a split between board members for the hike in March, all voters agreed that the cash rate would “probably need to be increased further at some point”. Despite the repeated references to uncertainty in the minutes, we think that the risks to Australia’s inflation now tilt to the upside. External supply disruptions are pushing up headline inflation as mentioned above, but structural issues around housing inflation will persist as rents growth are now accelerating and vacancies remain around record lows. In addition, domestic services inflation (especially in essential services), largely driven by wages growth, is potentially gaining some momentum in the upcoming quarters.

Latest updates

PDF version of Firstlinks Newsletter

Monthly Investment Podcast by UniSuper

ASX Listed Bond and Hybrid rate sheet from NAB/nabtrade

Listed Investment Company (LIC) Indicative NTA Report from Bell Potter

Plus updates and announcements on the Sponsor Noticeboard on our website