When we think about the current volatility, we are reminded of a prescient quote from Russian revolutionary and president Vladmir Lenin:

“There are decades where nothing happens and there are weeks where decades happen.”

Time will tell whether the Iran war is indeed one of these periods where decades happened.

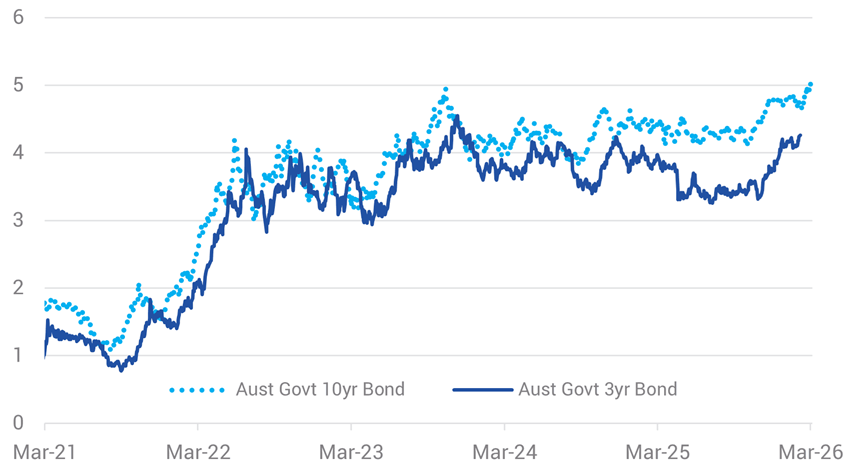

As for markets domestically, higher oil prices have collided with sticky headline inflation and a hawkish central bank. Australian government bonds have sold-off aggressively in March, with 3 and 10-year bond yields now at ~4.8% and 5% respectively (refer Chart 1). Moreover, despite the Reserve Bank of Australia (RBA) increasing the cash rate twice in February and March 2026 to 4.1%, interest rate markets as of 20 March were pricing in another ~70bps of tightening by the end of 2026 to 4.8% (i.e. close to another three 25bps increases in the RBA cash rate).

Chart 1: 3-year and 10-year Australian Government Bond Yields (%)

Source: Bloomberg, Mar 2026.

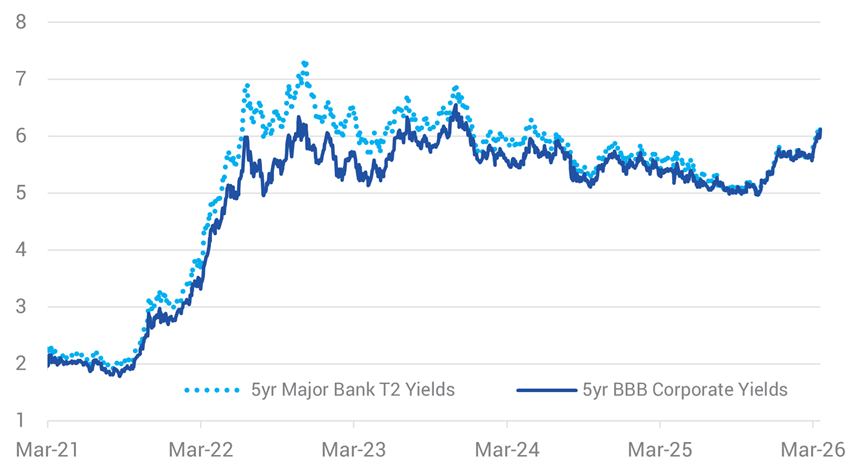

This higher rebasing of interest rates has a commensurate impact on corporate bond yields, with 5-year major bank T2 and triple B corporate yields now both back above 6% for the first time since late 2023 (refer Chart 2).

Chart 2: 5-year T2 and BBB Corporate Yields (%)

Source: NAB, Yarra Capital Management Mar 2026.

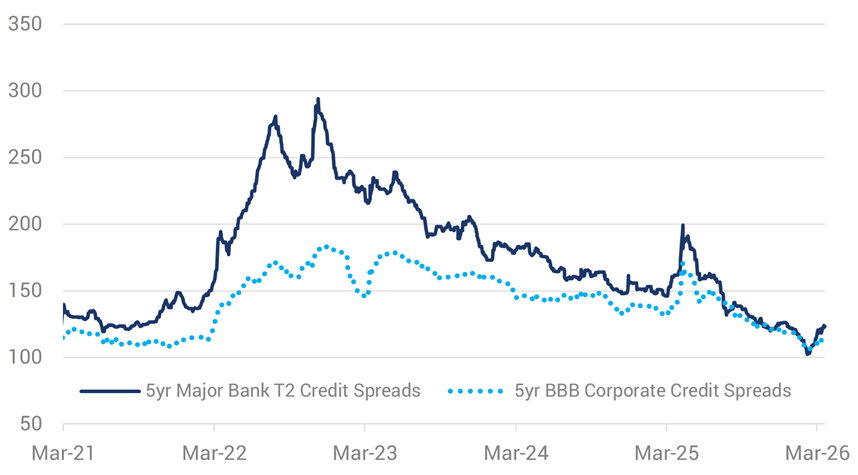

By contrast, the movement wider in investment grade (IG) credit spreads of ~20bps only takes us back to late 2025 levels (refer Chart 3). The orderly behaviour of IG credit thus far is testimony to the power of higher risk-free rates and outright yields (i.e. lessening the pressure on credit spreads to achieve investor return targets). Moreover, for the most part risk markets are still pricing in a speedier return to normalcy, enabling central banks such as the RBA to raise rates despite the heightened uncertainty.

Chart 3: 5-year T2 and BBB Corporate Bond Spreads (bps)

Source: NAB, Yarra Capital Management Mar 2026.

When uncertainty in markets is elevated, playing the averages over the medium term typically remains the best course of action. In many ways, what we’ve experienced in recent months, turbocharged by the Iran war, is a mini 2022 period with one important caveat. After the normalisation of bond yields in 2022, travel time to higher bond yields in 2026 was shorter and much less painful for interest rate duration positions.

From our perspective, while holding some duration has been reflected in performance in recent months, our focus has remained on taking advantage of higher outright yields and locking in attractive income. Portfolio running yields for the IG quality Yarra Enhanced and Higher Income funds are now well above 6% and approaching 7%, levels we last generated in 2023/24. Maintaining duration in portfolios at these elevated levels is advantageous for sustaining performance throughout the remainder of 2026.

In addition to higher bond yields, the rebuilding of more rate hikes in market pricing has significantly flattened the yield curve. The difference between the 3 and 10-year bonds is now under 30bps, down from a peak of ~120bps during the liberation day selloff in April 2025 (refer Chart 4). In this environment and if sustained, a flatter yield curve should result in a steeper credit curve with investors at the very least demanding increased term premiums in the current environment (i.e. higher credit spread compensation for longer dated securities).

Chart 4: Yield Curve – 3s10s (bps)

Source: Bloomberg, Mar 2026.

While credit spreads remain well behaved, if the current interest rate pricing is even half realised – i.e. reflective of some RBA future hikes – then a significant deflationary impulse for the Australian economy is likely. This is especially the case when combined with an appreciating $A, much higher petrol prices, greater application of AI tools across the economy and a retreating public sector following a more austere May Federal budget. Resultant higher unemployment and much weaker economic growth is likely to reverse current interest rate settings through the course of 2026/27. Therefore, despite a small impact in recent months, maintaining interest rate duration in portfolios continues to make sense at current levels.

In an environment of much weaker growth and higher unemployment, rallying bond yields is likely to result in credit spreads moving wider, with the current calm in credit giving way to a further rebasing of spreads. Our focus remains on locking in favourable income and using duration and curve to protect the portfolio and strongly position us to take advantage of the transition in return composition, with credit spreads likely to comprise a greater proportion of future outright yields following a significant decline in risk free rates.

Phil Strano is Head of Australian Credit Research at Yarra Capital Management, a sponsor of Firstlinks. This article contains general financial information only. It has been prepared without taking into account your personal objectives, financial situation or particular needs. Both the Yarra Enhanced Income and Higher Income Funds are zero leverage funds, providing attractive yields.

For more articles and papers from Yarra Capital, please click here.