There is a remarkable concentration similarity between the Australian and US stock markets that has delivered poor results for Australians and great results for Americans (and global investors). As the share prices of five Australian banks have tanked, the prices of five US tech companies have surged. Each group now represents 20% of their respective indexes, but the journey has been a disaster for many Australians.

Despite the rapid fall in market value of the Big Five Australian banks, they still comprise 20% of the S&P/ASX200 Index as at 13 May 2020, down from about 30% a few years ago.

| Bank |

Weighting in ASX200 |

Price fall in last 12 months |

| CBA |

7.4% |

-18% |

| Westpac |

4.0% |

-44% |

| National Bank |

3.4% |

-37% |

| ANZ Bank |

3.3% |

-41% |

| Macquarie Bank |

2.0% |

-11% |

| TOTAL |

20.1% |

|

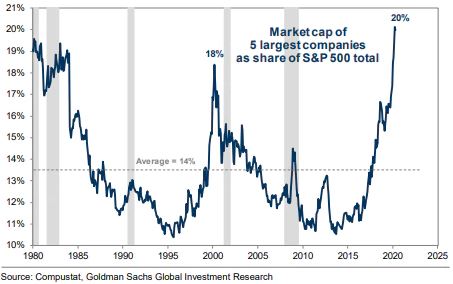

In contrast, the amazing success of Microsoft, Apple, Amazon, Alphabet and Facebook to become the largest five companies in the US now means they also comprise 20% of the S&P500. Where traditionally the US market was admired for its diversity, an index investment now has a solid exposure to only five companies (chart below is as at 23 April 2020).

The 12-month price changes to 12 May are Microsoft +44%, Apple +58%, Amazon +25%, Alphabet +18% and Facebook +12%. Australian retail investors who have held our banks for their high yields are now suffering as dividends are savaged. In investing, what matters is the future, but can anyone make a convincing case that the prospects of our banks are better than the five US companies? Boosted by these tech giants, the S&P500 has fallen half as much as the S&P/ASX200 in calendar 2020. Thank goodness for CSL.

We start with Howard Marks and his latest update on uncertainty and forecasting during a crisis. For those of you struggling with whether we are in a bear or bull market, he explains why nobody really knows meaningful information about the crisis.

David Walsh shows most of the return from local stocks has traditionally come from dividends, and companies preserving capital will have major ramifications for our market. Then Rudi Filapek-Vandyck says this dividend income focus and reliance was always a poor strategy, as investors should have looked more to share price growth for reliable income.

In his half-yearly Bank Scorecard Report, Hugh Dive summarises the dramatic changes hitting banks, especially loan provisions, and he sees much in their financial accounts which is guesswork at this stage.

Garry Laurence explains how varying performance comes from different sector exposure, and how he is finding global opportunities after the recent sell offs.

It's not all bad news for retail investors. Gemma Dale goes inside the client dealing of nabtrade and suggests many investors had held cash waiting for better buying opportunities. Gemma is also joined by Kate Howitt in a video discussing dividends and capital raisings.

While we are all hearing the latest catch phrase, 'the market is not the economy', Angus Coote says this as a poor explanation for the failure of risk markets (equities and credit) to realise how bad the coming corporate results will be. Crucially, liquidity cannot fix insolvency. Last night's stock falls in the US are a warning.

While also concerned with lesser-quality credits, Brad Dunn is more optimistic that there is a role for investment grade paper in a defensive asset allocation.

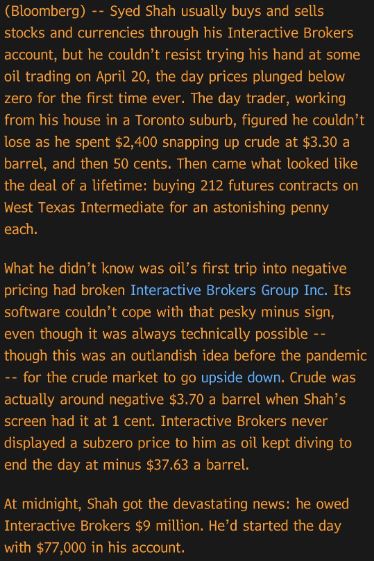

The remarkable events in the oil market are explored by Alistair Mills who shows how oil ETFs are managed and how investors can take a view on energy assets. It's better for most people to invest in commodities using funds (with the possible exception of physical gold) rather than futures, as this extraordinary (unrelated) Bloomberg story shows.

Two new articles added over the weekend.

Mike Murray finds a healthcare stock which is well-positioned to benefit from ongoing treatment of COVID-19, while Donald Hellyer provides data on how women are faring on company boards and uncovers an important difference not often discussed.

This week's White Paper from Fidelity International looks at the new economic order likely after Covid-19, and the opportunities that will come from the dislocation.

Graham Hand, Managing Editor

Latest updates

PDF version of Firstlinks Newsletter

Global ETF Review Q1 2020 from BetaShares

ASX Listed Bond and Hybrid rate sheet from NAB/nabtrade

Monthly market update on listed bonds and hybrids from ASX

Indicative Listed Investment Company (LIC) NTA Report from Bell Potter

Monthly Investment Products update from ASX

Plus updates and announcements on the Sponsor Noticeboard on our website