The Retirement Income Review has delivered far more than expected when it was commissioned. The fact that it does not include any firm recommendations is almost irrelevant. The Henry Tax Review contained 138 recommendations and most of them are still gathering dust. This time, former Treasury official Michael Callaghan's group can expect more policy consequences despite originally being asked only to:

“establish a fact base of the current retirement income system that will improve understanding of its operation and the outcomes”

That sounded like collecting statistics with a rather dry outcome, but it commendably confronts many of the arguments taking place in the superannuation industry. There’s a fine line between some of its statements and a policy recommendation.

For example, it makes arguments such as:

“Changes to superannuation earnings tax concessions would improve equity.”

“Extending earnings tax to the retirement phase could also simplify the system by enabling people to have a single superannuation account for life and would improve the sustainability of the system.”

“The weight of evidence suggests the majority of increases in the SG come at the expense of growth in take-home wages.”

“Replacement rates are the most appropriate metric for assessing whether the retirement income system maintains living standards in retirement.”

“Using superannuation assets more efficiently and accessing equity in the home can significantly boost retirement incomes without the need for additional contributions.”

It provides the Government with a blueprint for policies previously hinted at and subject to strong opposition, placing firmly on the agenda that:

- Retirees must learn to live off their savings and the equity in their home, not only the earnings on their investments, and

- Too much of the benefits of superannuation go to wealthier people.

Five highlights from the Review

1. Increases in super result in lower wages growth

Treasurer Josh Frydenberg would have enjoyed the line in the Review saying: “increases in the SG rate result in lower wages growth, and would affect living standards in working life.”

In the Media Conference releasing the Review, Frydenberg looked mightily pleased with the results, saying:

"It points out that people's early access to superannuation during the COVID crisis has been justified in that it sometimes is appropriate for people to access superannuation early and that this hasn't had a significant impact on people's retirement incomes ... I'll quote it (the Report), 'Maintaining the superannuation guarantee rate at 9.5% would allow for higher living standards in working life. Working life income for most people would be around 2% higher in the long run.' So the Report goes into some detail about the trade off between a working life income and people's wages and that with an increase in the superannuation guarantee, it points out that the most effective way for people to secure themselves in retirement is not necessarily an increase in the superannuation guarantee, but by more efficiently using the savings that they do have."

This is a major point of difference between the Liberals and the unions and industry funds, most vocally represented by Greg Combet, Chairman of Industry Super Australia and a former federal Labor minister. The Government now has the ammunition to ditch the legislated increase in the SG from 9.5% to 10% on 1 July 2021, and subsequent increases to 12%, claiming the money is better in workers' hands now. Combet argues that real wages have stagnated at a time when super has not increased. It is highly unlikely that if the SG is not increased by 0.5%, there will be a 0.5% increase in wages instead. Combet wrote in The Sydney Morning Herald of 26 November 2020:

"Analysis of more than 8,000 workplace agreements made following the last freeze in the super guarantee in 2013 found no evidence of compensating wage rises."

The Review finds many people are forced to reduce consumption in their working years, and often end up with more in retirement than they need. There should be a better balance between pre- and post-retirement needs:

“Saving for retirement involves forgoing consumption in working years. With voluntary saving, people decide on this trade-off. When there is compulsory superannuation, the rate should be set at a level that balances pre- and post-retirement living standards for middle-income earners. It is challenging to set a single SG rate that suits all Australians given the variety of people’s circumstances and experiences.

A rate of compulsory superannuation that would result in people having an increase in their living standards in retirement may involve an unacceptable reduction in living standards prior to retirement, particularly for lower-income earners.”

2. Retirees must learn to spend their capital not only live on their income

The Review makes many references to the capital in a superannuation fund financing retirement, not only the income. Superannuation should smooth income over work and retirement, not build a nest egg to leave to the next generation. It says:

“A major misunderstanding is the view that ‘retirement income’ involves the return from investing superannuation balances rather than drawing down those balances to fund living standards in retirement.”

The vital piece of research supporting this opinion is this:

“Data provided by a large superannuation fund found members who died left 90% of the balance they had at retirement. When retirees die, most leave the majority of the wealth they had at retirement as a bequest.”

In fact, so strong is the view that super should be run down, it is also used to justify leaving SG at 9.5%. Here, the Review argues if savings were more efficiently used (that is, run down), the 9.5% is sufficient to deliver a 65% to 75% replacement rate (of income prior to retiring) which is entirely adequate.

“More efficient use of savings in retirement can have a bigger impact on improving retirement income than increasing the SG. If the SG remained at 9.5 per cent, and retirement savings were used more efficiently, most people would achieve 65-75 per cent replacement rates. Most would also achieve higher replacement rates than with the SG at 12 per cent and drawing down balances at the legislated minimum rate.”

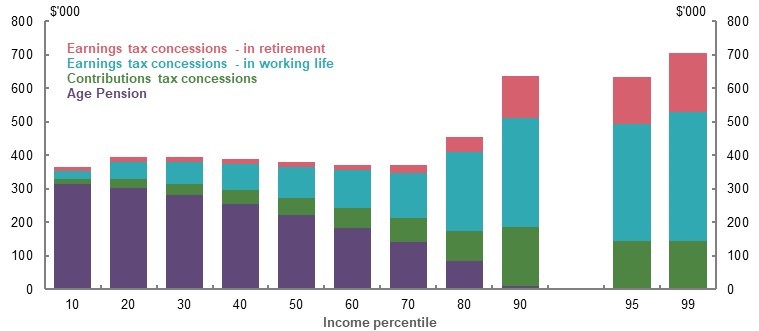

3. People with large super balances receive too much in tax concessions

In noting 11,000 people have over $5 million in superannuation, the Review states:

“While the age pension helps offset inequities in retirement outcomes, the design of superannuation tax concessions increases inequality in the system. Tax concessions provide greater benefit to people on higher incomes.”

The Review includes this chart which shows people with incomes in the 99th percentile receive more tax concessions both during their working lives and in retirement than any other grouping. The age pension makes up most of the government support for all groups up to the 50th income percentile, and it’s a material contribution even up to the 80th percentile.

Figure 1: Projected lifetime Government support from the retirement income system

Note: Values are in 2019-20 dollars, deflated using the review’s GDP deflator and uses review assumptions (see Appendix 6A. Detailed modelling methods and assumptions). Income percentiles are based on the incomes of individuals (whether they are single or in a couple). Source: Cameo modelling undertaken for the review.

Showing the ongoing role played by the age pension, as at June 2019, 71% of people aged 65 and over received some form of pension payment, and over 60% of these were on the maximum age pension rate.

4. The family home is a vital part of retirement planning

The Review makes the case for accessing home equity:

“One of this report’s themes is that a more optimal retirement income system would involve retirees more effectively drawing on all their assets, including the equity in their home, to fund their standard of living in retirement.”

It has little sympathy for the view that retirees need to preserve the equity in their home to pay for aged care. It describes the following statement as a common misunderstanding: “I need to preserve my assets in case I get sick or need aged care.”

Josh Frydenberg also embraced the finding that home ownership is key to an adequate retirement income. He said:

“Importantly, the Review provides confirmation of the policy direction being pursued by the Morrison Government with respect to the importance of increasing the efficiency of the superannuation system and lifting home ownership rates – both identified as key drivers of an adequate retirement income ... Additionally, given the importance of home ownership to the financial security and wellbeing of Australians in retirement, the Government will continue to support measures to allow more Australians to buy their first home sooner, including through our First Home Loan Deposit Scheme, First Home Super Saver Scheme and HomeBuilder.”

The Review clearly sees people who rent in retirement as vulnerable and the ones the social security system needs to protect. It says:

“The retirement income system does not appear to be delivering an appropriate standard of living for many retiree renters. Owning a home has a positive influence on a person’s standard of living in retirement. Whereas, in retirement, renters have higher levels of financial stress. A significant proportion of retiree households that rent are in income poverty, which is even higher for single retiree renters.”

The consequence of this retirement funding via home equity is profound. Instead of the heavy focus on superannuation in retirement, the family home will increasingly come into play, including how super money can be used to buy a home. As the chart below shows, the poverty rates in retirement are highest for single renters, couple renters and people forced into retirement early who have been unable to build their wealth. Home owners are least likely to live in poverty.

Figure 2: Income poverty rates of retirees

Note: Data relates to 2017-18 financial year. Elevated poverty rate defined as 5 percentage points above retiree average. Retirees are where household reference person is aged 65 and over. There is overlap between some categories, for example, early retired and renter categories. Early retired means aged 55-64 and not in the labour force. Housing costs includes the value of both principal and interest components of mortgage repayments. Source: Analysis of ABS Survey of Income and Housing Confidentialised Unit Record File, 2017-18.

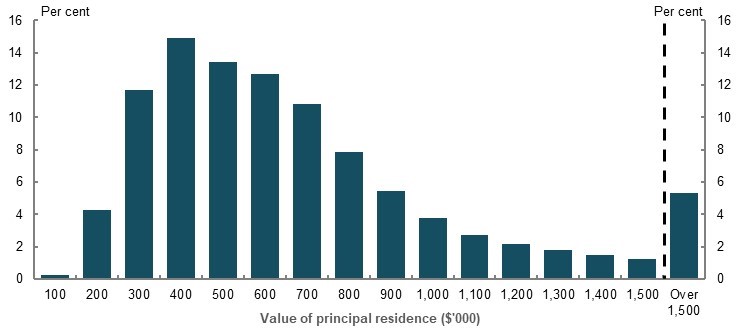

5. The case to means test the family home

While the Review leans heavily towards policy suggestions in many other areas, it dare only hint at that most sacred of cows, the exemption of the family home from social security tests. However, the subject is not ignored:

“A key aspect of the retirement income system favouring home owners is that the principal residence is excluded from the assets test for the age pension. Regardless of the value of the house, a home owner can receive the same age pension as a renter, all other things being equal.

This suggests that wealthier retirees (in terms of the value of their homes), can receive the same Government assistance as those less wealthy (either retirees who rent or home owners with houses of lesser value).”

Renters who hold assets in a form other than their house will receive less in an age pension than a home owner with the same level of wealth. The worry is that a declining trend in home ownership will increase the number of retirees renting in future.

On this sensitive subject, the opinions are of ‘some stakeholders’ rather than the review team, although it's clear that home owners and renters are not treated equally in the retirement income system:

“Some stakeholders suggested that if a retiree’s principal residence was part of the age pension assets test, this would help equate the treatment of home owners and renters. If the home were included in the assets test, some home owners would no longer be eligible for the age pension. Others would receive less age pension. In response, home owners may be more inclined to access the equity in their home to fund their retirement.”

To illustrate how home owners benefit from this system, this chart shows many age pensioners own homes with a value above the pension cut off level (which for a single home owner is $578,250).

Figure 3: Distribution of home values among age pensioners who own their home

Note: Horizontal axis labels indicate home values up to that amount (e.g. $200,000 includes homes over $100,000 up to $200,000). Source: Department of Social Services analysis of payment data, June 2018.

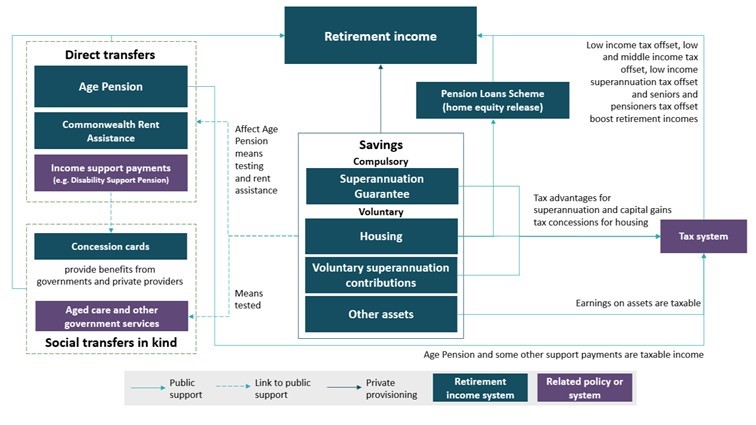

Bringing it all together in an interactive system

The 650-page final report contains a wealth of information that will inform the superannuation debate for years to come. It highlights the major interactions of the welfare and government concession systems, such that certain people benefit from multiple benefits. The figure below is a useful summary bringing together these interactions.

Figure 4: Key retirement income system interactions

The Retirement Income Review goes much further than an innocent-sounding 'fact base'. If we thought the fight over franking credits at the last election was heated, we are likely to see even fiercer battlelines at the next election between unions (and industry funds) and the Coalition Government.

Graham Hand is Managing Editor of Firstlinks. The full Retirement Income Review is linked here.