The Weekend Edition includes a market update plus Morningstar adds links to two of its most popular stock pick articles from the week.

Weekend market update

From AAP Netdesk: A first week of gains in the past five on the ASX had investors feeling better although there's wariness of China's highly-leveraged economy. An ASX rally on Friday was spurred by expectations of an economic rebound as eastern states gradually reopen from coronavirus lockdown. The benchmark S&P/ASX200 index closed higher by 63 points, or 0.9%. The market improved 1.9% over the five days.

Iron ore miners thrived after the price of the steel-making commodity nudged higher. Rio Tinto climbed 4%, BHP gained 3%, Fortescue was up 2.4%.

Woolworths has now paid $370 million for staff underpayments from 2013 to 2019 but shares were up 0.6% to $39.95. In banking, the big four were mostly higher. NAB was best on Friday and rose 1.4%.

From Shane Oliver, AMP Capital: Despite a messy US jobs report on Friday, global shares mostly rose over the last week as the US debt ceiling was pushed out to December and there was some easing in concerns regarding the European energy crunch. For the week US shares rose 0.8%, Eurozone shares rose 0.7% and Chinese shares rose 1.3%, but Japanese shares fell -2.5%. On Friday, the S&P500 fell 0.2% and NASDAQ was down 0.5%.

The Biden Administration’s $550 billion infrastructure spending and $3.5 trillion Build Back Better spending packages have been delayed a month or so but it still looks likely that to get moderate Democrat support with some cut backs.

The energy crisis in Europe and China is adding to supply bottlenecks and stagflationary pressures. The good news is that Russian President Putin has offered to increase gas supply to Europe (where prices have risen six-fold since earlier this year) although it may come with some strings attached (eg speeding up the certification of the Nord Stream 2 gas pipeline). Likewise, there are some signs China is easing restrictions on coal and electricity supply.

***

Cognitive dissonance is the mental discomfort caused by holding two conflicting beliefs or values. We might rush into buying a house although we believe prices will fall but the fear of missing out is even worse. We don't like the pain inflicted by excessive gambling but we invest in casinos. Alcohol destroys families but a beer company sponsors our local football club. We believe sugar is detrimental to health but we work for a soft drink maker. A short-term share trade makes a loss and becomes a long-term investment.

F. Scott Fitzgerald even justified dissonance when he said:

"The test of a first-rate intelligence is the ability to hold two opposing ideas in mind at the same time and still retain the ability to function."

Insiders say Steve Jobs could hold completely disparate ideas and values in his mind at the same time and still act on them.

For many people, an inconsistency between a long-held value and a recent action can be troubling, and tension is relieved in different ways. We rationalise, reject, justify and explain. "Yes, more jobs means higher economic growth but it will lead to interest rate rises and lower economic growth."

Financial markets are full of conflicting beliefs. Central banks pump trillions into the economy with no apparent downside, where once we believed inflation would be inevitable. Now, as inflation is rising, we call it transitory and interest rates do not need to respond. We know nobody can accurately forecast the next market downturn but we listen to expert predictions every day. The majority of active managers cannot outperform their benchmarks but there is more money under active management than passive.

Consider this paragraph from the weekly newsletter of the highly-respected global financial analyst, John Mauldin, typical of much market commentary.

"The latest volatility may or may not turn into something more extended. Some of the most respected market analysts are turning bearish. Still, others expect the bull market to continue. Timing is hard. Yet nothing has happened to make bear markets impossible. Stocks are overextended by many different measurements, so at some point, the bears will take control. More than a few investors aren’t ready for that possibility."

Say, what? Some bears, some bulls, markets are extended or maybe not. It's enough to dissonant your cognition.

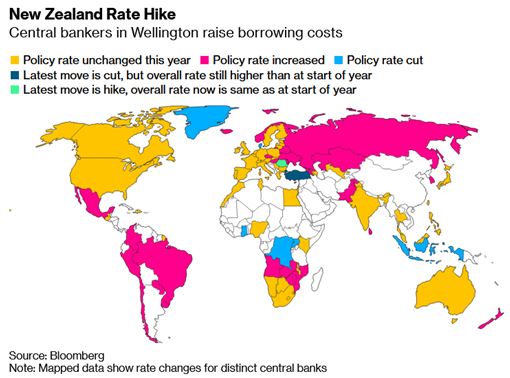

The Governor of our Reserve Bank, Philip Lowe, said Australian interest rates will not rise until 2024 while the Reserve Bank of New Zealand last week moved up 0.25% to 0.5% with another increase expected in November. Australian rates may need to rise if inflation takes hold as New Zealand is not the first to move up.

Cognitive dissonance is worse in politics, because the number one aim of any political party is to win elections. There is no point being a politician in opposition, so policy is not good if it is too unpopular. The Labor Party recently abandoned the negative gearing, capital gains tax and franking credit policies previously argued for. And at his 'back in black' budget in 2019, Treasurer Josh Frydenberg said:

“The country is now living within its means. We have got there by being restrained and disciplined."

Within two years, the FY21 budget deficit was $134 billion due to COVID costs. Fair enough in a pandemic, but Josh Frydenberg presided over a JobKeeper programme worth $89 billion where an estimated 31% of recipients were not eligible, with no ability or desire to clawback claims by employers who exaggerated their losses. Australia faces a submarine project costing an unknown amount above $100 billion for equipment not delivered until 2040 at best. At a state level, there are billions for new stadiums that replace good stadiums, light rail that is slower than buses and an unlimited money for favourite local projects. What happened to 'restrained and disciplined'?

A Federal election is due by 21 May 2022. While most of us have taken our medicine to ward off the virus, we will be less inclined to accept a cure for budget deficits. As befits spending in a crisis, the budget deficit in FY21 was the largest dollar amount in history and the largest as a share of GDP since WWII at 28.6%. Yet the Parliamentary Budget Office has estimated that net debt could be reduced by $276 billion by 2030 if we do not proceed with planned personal tax cuts for wealthier people. The Treasurer insists they will proceed.

And there is a cognitive dissonance. The Treasurer says tax cuts are in his Government's DNA but as recently as December 2019, he was proud of the restraint delivering a budget surplus for 2020/21. As the next six months roll into an election campaign, voters will buy the promises of largesse. In 2020 and 2021, it seems central banks can print money and pay for almost anything with no adverse consequences.

Much like the conflict in our minds of our largest trading partner also being our biggest national security threat, that's a cognitive dissonance.

Meanwhile ... signs of inflation are everywhere, such as rising global energy costs, shortages of supplies, increasing house prices and global shipping costs, as shown below.

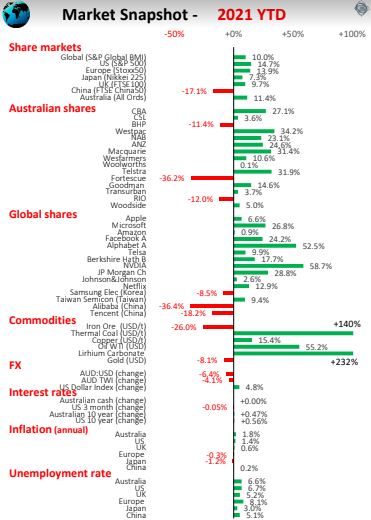

Amid all this turmoil, the market has experienced a few wobbles but hangs on to its gains. Courtesy of Ashley Owen, here are the major markets and other data points for 2021 to the end of September. Stay away from China and it's nearly all green, and there's a cognitive dissonance between rises in coal prices at a time when the world is supposed to be turning away.

As we emerge from lockdowns, with freedom to move and billions to inject into the economy, it will be a volatile time for economic growth and prices. Good luck finding a builder for a renovation in the next year. APRA has announced the first of the prudential controls on housing that we called for last week. In itself, it will have little impact as the 3% 'buffer' now required by banks on loan repayments is close to the 'floor' many banks are already using, but there is more to come.

So it's a good time to take a quick stocktake with five charts on who pays the taxes, who owns the assets and who earns the income. What do an average 100 Aussies look like?

Ashley Owen then takes us through the recent history of Australian house prices, when and why they rise and fall, and he justifies his price views for the coming year or two. Nobody has better charts than Ashley.

The world is experiencing another disconnect between the timing of renewables and batteries coming online and the cutback in investment on fossil fuels. Roy Chen explains the consequences drawing on Europe's chilling experiences. In the short term, it's great for Australian gas exports but it will feed into inflation.

Amy Arnott summarises Morningstar research in the US which shows the poor investment results for many investors compared to the funds they invest in due to the timing of cash flows (the dollar-weighted returns). Combined with taxes and fees, it's a major impediment to investment success.

Drawing on a speech that David Gonski AC gave to the UNSW Graduate School, he delivers nine pearls of wisdom from his vast business experience and leadership. Mr Gonski is considered the best-connected of businessmen and has chaired many companies, and he knows what works and what doesn't.

Still on lessons into how to run a business, Delian Entchev dives into the success of the prestige goods company Louis Vuitton Moet Hennessy (LVMH). Its amazing collection of 75 brands in cosmetics, wines, spirits, watches, travel goods and fashion are at the top of their game and will benefit from spending coming out of lockdowns.

And Michael Collins gives a fascinating update on ransomware, which is not only hitting homes and businesses but national security, and he offers a radical solution to stop the payments feeding to problem. I personally faced a ransomware attack some years ago which did not end well, and I've been wary of clicking on unrecognised email links since.

Two bonus articles from Morningstar for the weekend as selected by Editorial Manager Emma Rapaport.

Soaring natural gas prices are set to boost short-term profits at Woodside Petroleum as gas shortages in the northern hemisphere highlight the fuel's importance to the clean energy transition, writes Lewis Jackson. And Seth Goldstein highlights four stocks to watch in the electric vehicle supply chain as the adoption of EVs expands rapidly.

The Comment of the Week comes from C, among many excellent thoughts on Saul Eslake's housing article:

"Do you know who are those people priced out these days? It's not just the waitresses and childcare workers but also those well educated and qualified professionals in their 40s with family income 200k-300k. The problem is they don't have rich parents. Are those families expecting too much for wanting to live in a 3 bedroom house in a reasonably good school catchment?

In all honesty, how many of you have helped your children with house deposits? I know a couple with $150k family income bought $3m and several couples with approx. $250k family income bought $4m houses. All with parents' help. Their parents' houses are now worth $7m, $8m.

The way things are going, I will have to help my kids in the future too. My kids have no interest in money professions. They want to be engineers and build things, or scientists who cure cancers. With their intelligence and maths skills, frankly speaking, I think it would be a waste of talent if they end up working for banks and financial engineering products. I have nothing against bankers. Just thought it would be a tragic loss to society if all intelligent people need work in banking just so they can afford a house in north shore."

Graham Hand, Managing Editor

A full PDF version of this week’s newsletter articles will be loaded into this editorial on our website by midday.

Latest updates

PDF version of Firstlinks Newsletter

IAM Capital Markets' Weekly Market Insight

ASX Listed Bond and Hybrid rate sheet from NAB/nabtrade

Monthly market update on listed bonds and hybrids from ASX

Indicative Listed Investment Company (LIC) NTA Report from Bell Potter

LIC (LMI) Monthly Review from Independent Investment Research

Plus updates and announcements on the Sponsor Noticeboard on our website