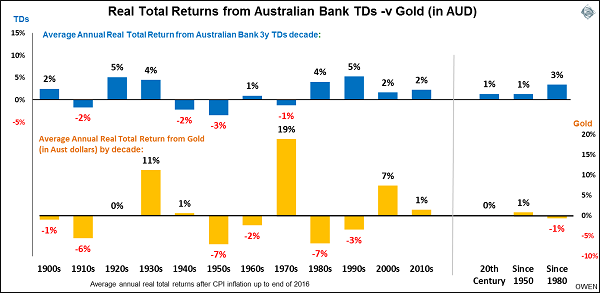

Last week we looked at Australian shares and bonds as safe havens. This chart shows returns from two other so-called safe havens: bank deposits and gold (in Australian dollars).

Click to enlarge

The good news is that gold has indeed provided a hedge against inflation and against the long-term decline of the Australian dollar (which is essentially the same thing) over the very long term. It has generated zero real returns after inflation (i.e. a hedge but no actual positive returns), but that’s before storage and insurance costs which eat into returns.

The bad news is that the gold price shoots up once in about every 30 years and then takes the next 30 years to recover its real value (more on this later). That’s a long time to wait. But if bought cheap (it is not cheap now) gold can provide an effective hedge (but with zero returns) if you are prepared to wait.

In the meantime, gold has suffered negative real returns for six decades out of the 12 decades since 1900, including seriously bad decade-long losses in the 1910s, 1950s and 1980s. Hardly a ‘safe haven’.

Bank deposits have generated very low returns overall, which should be expected since they are virtually risk-free. The last time an Australian bank failed to repay bank depositors was in 1932. The problem is that bank deposits generated negative real returns after inflation for four whole decades – the 1910s, 1940s, 1950s and 1970s. That means steady declines in living standards for several decade-long periods at a time. Hardly a ‘safe haven’ or ‘store of wealth’ or a protector of living standards.

With the possibility of war in the headlines lately, the charts show that during both the First and Second World Wars, the so-called safe havens of gold and bank deposits provided no safe havens from decade-long losses.

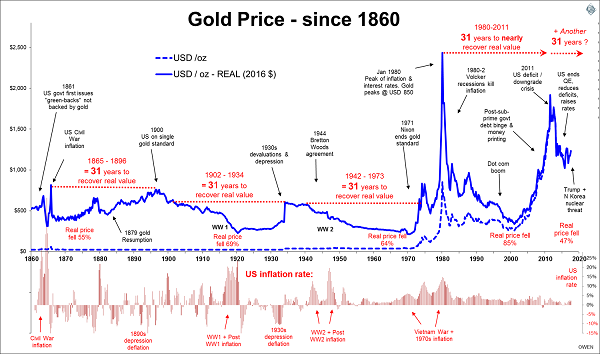

Gold: another 31 years?

The gold price shot up to US$1,900 per ounce at the height of the US downgrade crisis in late 2011. The usual shrill 'end of the world' panic merchants were excited about buying gold as it was going to go up to US$3000 or even higher.

Then the gold price collapsed 44% from US$1,900 to US$1,050 by December 2015, forced down by panic selling at the bottom of the oil/gas/steel collapse and the regular ‘China slowdown’ panic. But the recent mini-recovery to US$1,300 this year with the global ‘reflation’ scare and the North Korea nuclear threat has people starting to panic-buy gold again.

Panic buying and panic selling is not investing, it is speculating. Gold is a legitimate asset with a place in long-term portfolios from time to time (personally I like gold but I have not owned gold ETFs since selling in 2011).

Here is a chart on the medium-term history of gold prices.

Click to enlarge

Long term holding of gold makes sense as an inflation hedge only if bought when it is cheap, at or below the long-term value around which it has oscillated for thousands of years. It is well above that now and has been since 2010.

The gold price shoots up rapidly about once in every generation, due mostly to money printing by governments or inflation spikes. It then takes a generation to recover its real value. It has been a neat 31-year cycle from one peak to the next, so people who panic bought in each bubble need to wait another 30+ years for another one.

Ashley Owen is Chief Investment Officer at advisory firm Stanford Brown and The Lunar Group. He is also a Director of Third Link Investment Managers, a fund that supports Australian charities. This article is general information that does not consider the circumstances of any individual.