The August 2022 corporate results season in Australia is upon us and genuinely builds after mid-month, but July and the opening week have already generated some valuable insights for investors.

We explore miners, property trusts (A-REITs) and asset managers.

Miners and resources

All too often forgotten, producers of copper, gold, oil and gas, and other commodities are themselves heavy consumers of diesel, steel, water, power, and other commodities.

That reality has started to show up in quarterly production updates from miners and energy producers. One sector on the ASX that has been heavily hit are the local gold producers, if only because gold has largely traded sideways this year, apart from a temporary spike as Putin's army crossed the border with the Ukraine.

Rising costs when the price of your main revenue source refuses to spike higher can only mean one thing: margin pressure, and lower profits.

And so it was, when sector analysts at Canaccord Genuity updated their modeling and forecasts at the end of July. Higher costs translate into higher investments for those companies looking to expand and into higher operational expenses when running daily operations.

Consider the following incomplete list of price increases the industry is dealing with:

- Diesel costs up 60% on average in Western Australia

- Steel prices are up 60% from one year ago

- Freight costs can be up to 400% higher

- Costs for drilling have increased by 15-20% in recent months.

No surprise thus, running higher operational costs and capex estimates through its modeling, Canaccord Genuity's valuations reduced by -24% on average for explorers and developers and by -26% for producers.

With no sustainable uptrend predicted for the price of bullion anytime soon, the underlying conclusion at UBS is pretty much the same:

"...tempered growth ambitions, continued operating and inflation headwinds combined with our reduced price deck means stocks are not as cheap as they look."

Share price falls do not mean 'buy'

Not every share price that has fallen represents a great opportunity for mid- to longer-term investing. The challenge for investors is to identify the real gems and the real quality in a basket that is full of pretenders.

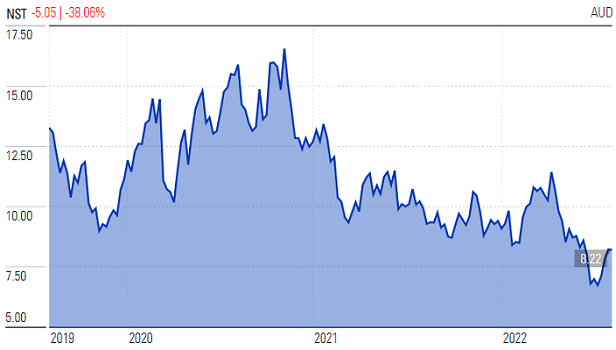

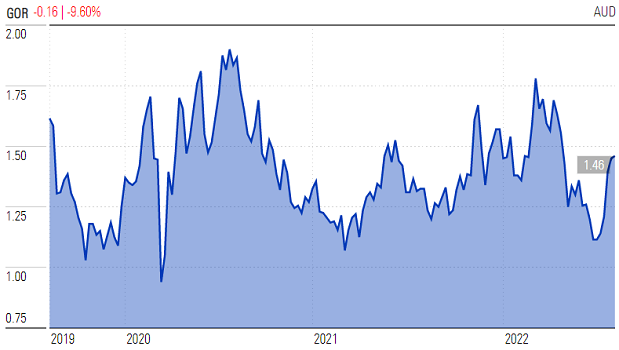

For what it's worth, UBS's favourites are Northern Star Resources (NST) among the large caps, because of the company's strong organic growth pipeline, and Gold Road Resources (GOR) among small caps. UBS analysts advise investors should focus on strong balance sheets, low risk growth and newer mines with a good runway and optionality still ahead.

(All charts in this article are sourced from Morningstar).

Northern Star Resources

Gold Road Resources

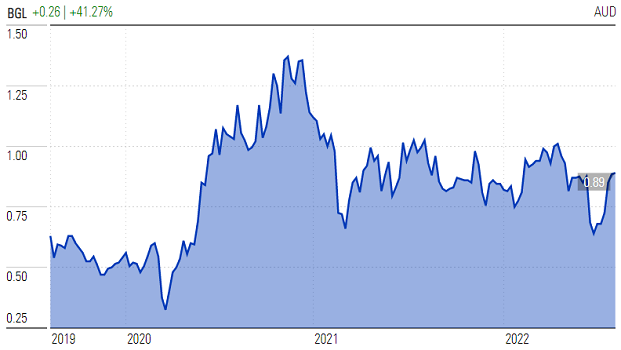

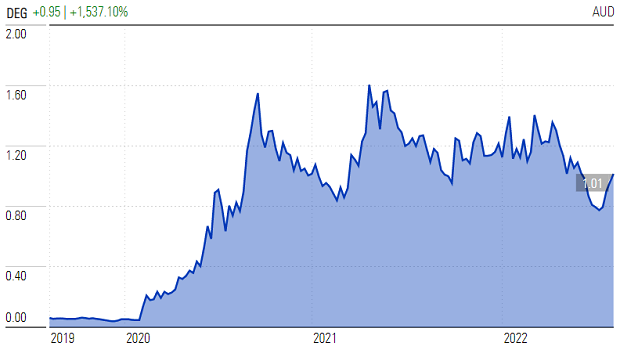

Canaccord Genuity's sector favourites are Bellevue Gold (BGL), De Grey Mining (DEG) and Predictive Discovery (PDI). All three have rallied off their June-July low.

Macquarie's favourites are Northern Star, Silverlake Resources (SLR) and Gold Road Resources among producers, as well as Bellevue Gold and De Grey Mining among juniors in the sector.

Bellevue Gold

De Grey Mining

Predictive Discovery

Silverlake Resources

The cost-inflationary pressures that have dogged the gold sector this year equally apply for commodity producers elsewhere, as also shown by June-quarter trading updates released by sector heavyweights BHP Group (BHP) and Rio Tinto (RIO), as well as by the half-year report already released by the latter.

Canadian iron ore producer Champion Iron (CIA) also disappointed and higher-than-anticipated costs proved one important contributor.

OZ Minerals (OZL) is more a copper stock than gold but it equally disappointed with its quarterly update in July, but the share price recovered ahead of BHP Group launching an unsolicited, 'opportunistic' takeover bid for the company on Monday 8 August.

Combine all the above and the take-away message for investors might be that sharply weaker share prices may have already discounted a lot of the bad news, at least in the short term, but cost inflation remains a problem and is creating wide divergences inside sectors.

BHP's takeover attempt shows August this year won't just be about bottom line-financials and forward-looking guidance. Analysts are expecting at least some commentary about a bonus dividend from Woodside Energy (WDS), while Origin Energy (ORG) should continue its share buyback.

Woodside is also still looking to sell down its Scarborough project, while Santos (STO) might soon announce new ownership for its non-core asset in Alaska, and potentially for its equity in PNG LNG too.

Note to us all: the threat of economic recession has not dissipated. The odds are shortening that Europe and the USA will join the UK in falling GDP in the months ahead.

Australian Real Estate Investment Trusts (A-REITs)

Another sector that has equally landed under close scrutiny is local real estate investment trusts, A-REITs, many of which have recently experienced significant price falls.

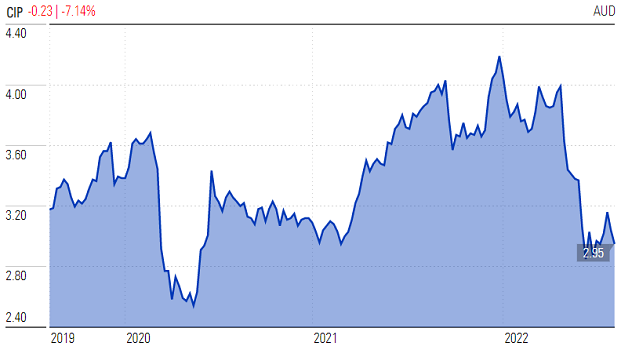

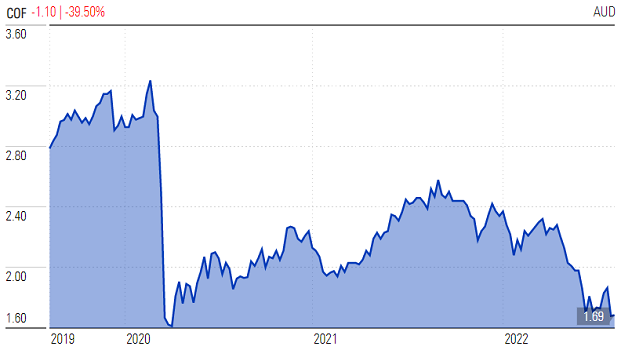

The early part of the earnings season saw both Centuria Industrial REIT (CIP) and Centuria Offce REIT (COF) releasing FY22 financials and while the former met forecasts and offers optimism now the share price has weakened significantly year-to-date, the latter disappointed and sees investors and sector analysts continuing to adopt a more cautious approach.

Centuria Industrial REIT

Centuria Offce REIT

What both REITs have in common is management at each trust has adopted a cautious approach regarding the rising cost of debt, which could become somewhat of a Sword of Damocles hanging over this sector for the year(s) ahead.

In simple terms, the market has taken what seems a rather dire view as to how high the weighted average cost of debt (WACD) can rise over the coming three years. While more optimistic sector analysts can thus see 'value' in the sector, others think the market's pricing seems but a realistic scenario.

The real estate analyst at Barrenjoey, Ben Brayshaw, is among the least enthusiastic. He thinks REITs will meet FY22 forecasts in August, but the outlook is for reduced growth, reduced profits, and reduced payouts for the sector on average. Issues range from rising costs, to deflating property markets, to the threat of less consumer spending, to still struggling office assets, to less opportunities for acquisitions, to higher headwinds from servicing debt.

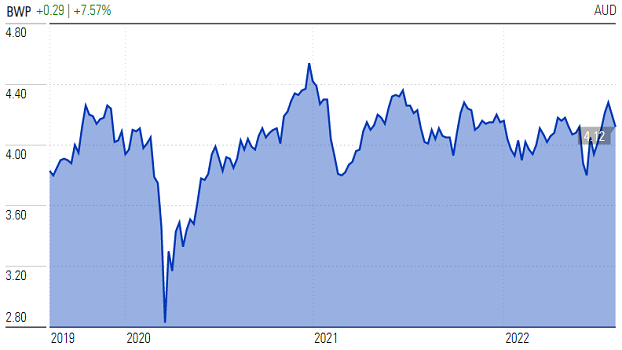

REITs were firmly in focus throughout week one, with Bunnings landlord BWP Trust (BWP) mid-week reporting "strong fundamental performance" and "prudent positioning", but given BWP just about always trades at a sizeable premium versus the rest of the sector, analysts simply cannot get excited, and this includes the perceived risk profile for the Trust.

BWP Trust

The sector as a whole is often described as a beneficiary of higher inflation (as leases are often tied to CPI), but the first three financial results this season have proved this narrative is too simplistic for general purpose.

Asset managers

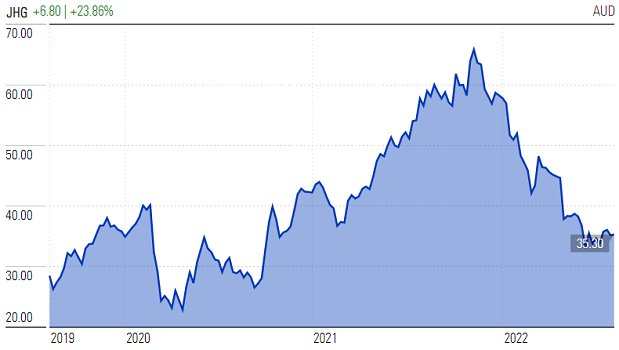

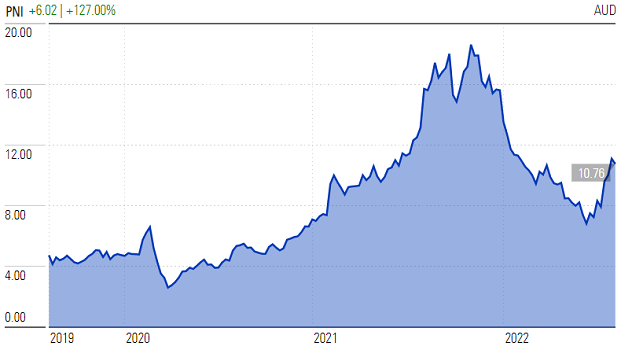

The first week also saw two asset managers releasing FY22 results and the outcome could hardly have been more different.

In one corner we find Janus Henderson (JHG) struggling to keep investor funds from departing while share markets in general are likely to face ongoing subdued momentum as the threat of economic recession continues to loom large.

Janus Henderson

In the other corner sits Pinnacle Investment Management (PNI), the umbrella group that includes affiliates such as Firetrail Investments, Hyperion Asset Management, Metrics, Plato Investment Management and Solaris.

Pinnacle Investment Management

Pinnacle is enjoying more popularity than its peers this year, making the impact from sector-wide selling on its share price pre-FY22 release looking extremely silly. But as the price chart shows, the market is addressing that situation recently.

Maybe the take-away message at the start of a busy reporting season is that individual strength can overcome general sector malaise.

Rudi Filapek-Vandyck is Editor at the FNArena newsletter, see www.fnarena.com. This article has been prepared for educational purposes and is not meant to be a substitute for tailored financial advice.