The ‘index versus active’ investing debate is one of the oldest arguments in the industry. On one side, researchers point to the legends of the market (think Buffett, Templeton, Lynch, Gross) who have outperformed a market index over long time periods. On the other side, as many brilliant minds point to statistics which show the majority of active managers underperform the index after fees over long time periods, and of course there will be some above average in a sample of thousands - that’s how probabilities work in any game of chance.

The professors can't agree, what hope for mere mortals?

The debate had another run this week when the Nobel Prize for Economics was shared by world-renowned professors with opposite views. In one corner is Professor Eugene Fama, who gave us the modern efficient markets theory that share prices incorporate all available information and there are no mispricings to exploit to consistently deliver outperformance. Fama’s conclusion in his paper (with Kenneth French), Luck versus skill in mutual fund performance, was:

“Going forward, we expect that a portfolio of low cost index funds will perform about as well as a portfolio of the top three percentiles of past active winners, and better than the rest of the active fund universe.”

The other Nobel winner, Professor Robert Shiller, says of efficient markets, “the theory makes little sense, except in fairly trivial ways”, and he draws on behavioural science to show the human errors involved in market pricing. He emphasises the extent to which individual investors misperceive and overreact to information.

Outperformance comes in many guises. Rosalind Hewsenian, CIO of a major US charitable trust and an investment consultant from 1985 to 2006, in this excellent article called ‘Beating the market has become nearly impossible’ (Institutional Investor, 18 September 2013), says:

“Most of my career was dominated by the twin rallies of the stock and bond markets. Alpha was generated by simply tilting risk a little higher than the markets generally and you could outperform.” (Note: alpha is a measure of excess returns).

Most asset manages do not accept such a humble and self-deprecating explanation.

About 80% of securities listed on the ASX are owned by institutional funds, domestic and foreign, each managed by highly qualified and skilled experts. There are thousands of stock pickers and analysts, all educated at the best universities in the world and most with decades of experience. They are the market and they own the index, and some will underperform and some will outperform. A few will look really good, and they will win awards and attract money. But how do we separate skill from chance? For example, the probability of making 60 correct guesses out of 100 coin tosses is about 2.8%. So if we have, say, 100 participants who guess a coin toss every month for 10 years, about three of them will correctly guess 60 out of 100. Are these the celebrated fund managers who have outperformed all the others? Surely, a decade of excellence in coin-tossing proves their added skill. But then what happens next year, on the next set of tosses?

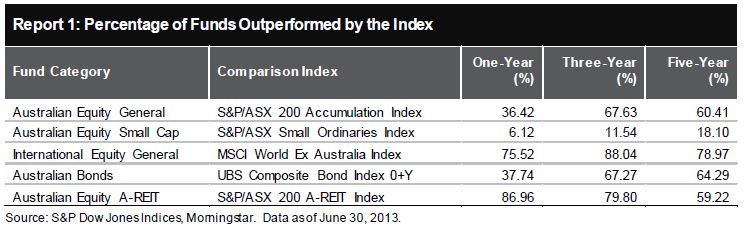

The latest ‘Index Versus Active’ scorecard

So it is opportune that in the same week as the Nobel Prize announcement, the updated SPIVA scorecard was released. This is a tortured abbreviation for the Standard & Poors’ (SP) Index Versus Active (IVA) scorecard. The report is issued semi-annually, the latest for mid-year 2013, and it tracks the performance of actively-managed Australian funds versus their benchmarks, corrected for survivorship bias.

The comparisons of active versus index over only 12 months are not much value. For example, in the year to 30 June 2013, 60% of active Australian equity funds outperformed the S&P/ASX200 Accumulation Index, but in the previous year, 70% underperformed over one year. Longer time periods must be studied.

The results over five years, summarised in the table below, are:

- the index outperformed over 60% of active Australian equity funds, and over three years, 68% of managers lagged their benchmarks

- 82% of small cap Australian equity managers actually outperformed their index. This occurs over all periods studied in the report. There are two reasons usually given why small cap managers consistently outperform their index. First, the index includes many speculative small resources companies with a dream but no decent cash flows, which eventually collapse, and managers often avoid these disasters. Second, small caps are less analysed than ASX100 companies, and it is possible to identify undervalued gems with excellent prospects

- 79% of active international equities underperformed their index, and 88% over three years

- 64% of active Australian bond funds failed to beat their index

- 60% of active Australian A-REIT funds failed to beat their index (and 87% in the last year)

- Only 81% of the asset managers from five years ago still exist.

It’s not much of a scorecard for the millions of hours of number-crunching and company visits by talented active managers. Or are they all so talented that they cannot beat each other?

Ironically, S&P believes active management provides a useful role, since the massive amount of research undertaken keeps prices close to fair values and allows index investors to take a free ride without paying the costs. They call this a ‘fragile equilibrium’, and quoting William F Sharpe:

“Should you index at least some of your portfolio? This is up to you. I only suggest that you consider the option. In the long run, this boring approach can give you more time for more interesting activities such as music, art, literature, sports and so on. And it very well may leave you with more money as well.”

It’s your call, depending on who and what you know. If you think you can identify the few managers who outperform the index consistently over time, either by research or based on advice, go for it. At least you’ll have more fun watching him (it’s always a man) explain the variability to the index and why his style did not work last year. If you don’t have an opinion, or don’t have the time, stick to an index. If there’s one thing you can control, it’s the cost, and the range of index funds now available allows wide choice to implement most asset allocation strategies.