“I used to rule the world

Seas would rise when I gave the word

Now in the morning I sleep alone

Sweep the streets I used to own

I used to roll the dice

Feel the fear in my enemy's eyes

Listen as the crowd would sing

"Now the old king is dead! Long live the king!"

One minute I held the key

Next the walls were closed on me

And I discovered that my castles stand

Upon pillars of salt and pillars of sand …”

Extract from Viva la Vida by Coldplay

Selecting an active fund manager who can outperform the market over time is even more difficult than picking stocks. A talented and skilful team may utilise a style which goes out of favour for many years, making the fund managers look below average. Investors may become frustrated with the poor performance and leave at the worst time, attracted to last year's successes.

Similarly, previous winners can go through rough patches. Many of Australia’s best-known fund managers, such as Hamish Douglass at Magellan, Andrew Clifford at Platinum, Roger Montgomery at Montgomery and Anton Tagliaferro at Investors Mutual, have struggled to match their benchmarks after fees in recent years.

Zero to hero

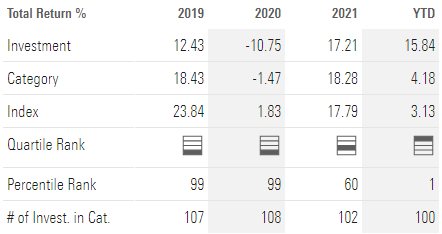

Consider the performance of the Lazard Select Australian Equity Fund since 2019, shown below. Its highly-regarded and experienced investment team carries a strong Silver rating from Morningstar, yet in both 2019 and 2020, it was in the bottom percentile of its category of Australian Equity Large Value (and Value also underperformed Growth). Almost last among over 100 managers surely tested the resolve of investors and analysts alike. It recovered somewhat over 2021, and in 2022 YTD, the fund is in first place, as well as in the top few over 12 months. Going from last to first in a year or two says a lot about the fortunes of fund managers.

Source: Morningstar Direct

Source: Morningstar Direct

A study of the 2021 Fund Manager of the Year

It works both ways.

In February 2021, Morningstar announced its 2021 Fund Manager of the Year awards, and Hyperion Asset Management was not only selected as the Overall winner, but also topped the separate categories of Domestic Equities – Large Cap and Domestic Equities – Small Cap. Morningstar said:

“Our 2021 winners have proven themselves to be excellent stewards of fund shareholders’ capital. Australian investors are well served by a solid lineup of quality managers, but Hyperion Asset Management wins our Overall Fund Manager of the Year award for a strong performance across all their stable of funds.”

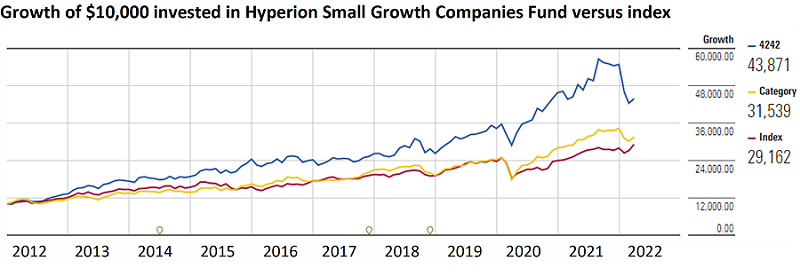

A check on the long-term performance of the Hyperion Small Growth Companies, which scores a rare Gold fund rating from Morningstar, shows why the investment team is held in high regard. Over the 10 years to 31 March 2022, the fund returned 14.6% per annum against its index (Morningstar Australia TME GR AUD) of 10.5%. Over five years, the comparison is 13.1% versus 9.6%. In the chart below, the blue line shows the Hyperion fund versus the red line of the index.

However, in the first quarter of 2022, the fund was down 20% versus the index up 4.2%. Investors have given back a quarter of their capital relative to the index in only three months.

What lessons do the recent results versus its history give investors about selecting active managers?

Warnings in the Morningstar analysis

Writing in September 2021, Michael Malseed, Associate Director at Morningstar explained the Gold rating:

“Hyperion Small Growth Companies continues to earn our highest conviction among growth-focused small-cap managers given its deep and differentiated research, genuine long-term time horizon, and highly experienced portfolio managers.”

Then in explaining the investment process, the reasons for recent underperformance appear:

“Hyperion pays little heed to benchmark weights when constructing a concentrated portfolio of high-growth small-cap stocks. Importantly, portfolio outcomes are a function of bottom-up research and forecast long-term internal rates of return, rather than any top-down or macro thematic. Nevertheless, this approach leads to large sector skews relative to the index and peers. Technology names have traditionally dominated, accounting for more than 34% of the portfolio as of 31 July 2021 compared with the benchmark's 8% and category average of 13%. Top holdings as at that date included software-as-a-service providers Xero and Wisetech Global. Consumer cyclical is the second-largest sector exposure at just over 30%, comprising names such as Dominos Pizza, Temple & Webster, and Kogan. Healthcare stocks also prominent through exposures such as Fisher & Paykel Healthcare, Nanosonics, and Pro-Medicus. Hyperion typically holds no allocation to materials and energy stocks, reflecting its lack of confidence in the sectors’ earnings predictability and pricing power.” (my bolding).

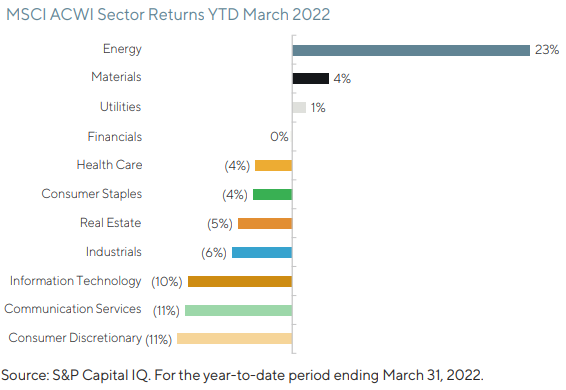

The technology and growth stock exposure which served Hyperion well in 2020 and the first half of 2021 reversed as the market became increasingly focussed on rising interest rates. Investors turned more towards resources and energy stocks, supercharged by the Ukraine war and a shortage of commodities.

The table below of sector returns in the MSCI All Country World Index for the first quarter of 2022 shows it was almost impossible for a fund without exposure to energy and materials (resources) to match its index.

Any fund manager measured against an index with significantly different stock weightings will produce outsized volatility when the market changes.

Therein lies the challenge for investors. Morningstar considers the Hyperion team one of the best but a first-time investor on 1 January 2022 has seen a 25% underperformance. The results from selecting an active fund manager often require patience. In some cases, managers can spend years underperforming with no change in their process or the people making the decisions that once placed them top of the league tables.

Hyperion’s global fund in the listed market

For investors who prefer to invest via the listed markets, Hyperion’s Global Growth Companies ETF (ASX:HYGG) has been on the ASX since 22 March 2021. Its March 2022 fund update shows unfortunate timing, delivering a nil return versus the benchmark of up 12.2% over 12 months. The same portfolio in managed fund form has an inception date of 1 June 2014 and has returned 19.4% per annum versus the benchmark of 13.2%.

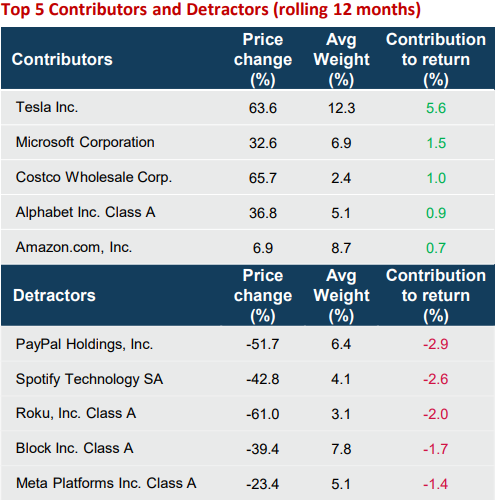

The major winners and losers over the 12 months are shown below. Some initial COVID beneficiaries such as PayPal, Spotify and Facebook (Meta Platforms) have given back much of the prior gains.

In an updated review of this fund written on 22 April 2022, Morningstar's Malseed reported under the heading ‘Backing long-term winners but patience is required’:

“... a strong growth-style bias will likely see short-term bouts of underperformance during cyclical or value-led rotations. Investors should be prepared for higher-than-average volatility.”

Here is the price performance of HYGG since listing, and with a 12-month price range of $3.32 to $4.98, the investor experience depends on the entry point. Over April 2022, the price has fallen from $3.92 to $3.38 at the time of writing (27 April).

What do Lazard and Hyperion tell us about active managers?

Hyperion’s first Australian equity funds were launched in 2002, giving it a 20-year track record. An investment of $100,000 in its Australian Growth Companies Fund in September 2002 would have increased to $918,547 by 31 March 2022 (net of fees with distributions reinvested) versus the S&P/ASX300 at $577,076.

It’s well established that most active fund managers do not beat their benchmarks after fees over time. It is common to see strong periods of outperformance when a style works well, but markets rarely reward a particular style forever. The 20 years is an impressive test period which shows evidence of skill rather than luck.

I am not a fund or stock analyst, and I have no intention of second-guessing my colleagues at Morningstar who spend their careers judging manager performance, but here are my takeaways:

1. Allocating to an active fund manager is a long-term decision

As Warren Buffett said, “The stock market is a device for transferring money from the impatient to the patient.”

There is no point paying active fees for a fund manager who hugs the index, and so investors should pay for skilled managers who back their views and run large tracking errors. These stock views may take years to pay off. Investors who jump out after a bad few years are likely to be leaving at the wrong time. A decision to place confidence in an active manager should come with at least a five-year horizon, and better, eight to 10 years.

2. Investors must have realistic expectations

Consistent outperformance will not occur over all time periods. Markets always face surprises and geopolitical events are difficult to forecast. Few people expected Russia to invade Ukraine and send commodity prices surging. A fund manager such as Hyperion who is unimpressed by the lack of certainty of earnings in the resources sector will suffer in current markets, at least over the short term. Lazard's traditional value approach struggled for years. Investing can face a long disappointment before a thesis pays off.

3. Funds may be vulnerable after a hot streak

A manager that has done well for many years and continues to hold the same stocks probably manages a portfolio that has become more expensive over time, absent evidence its companies are increasing earnings. This so-called ‘Price/Earnings expansion’ occurs when investors become more confident about long-term prospects and are willing to pay more for each dollar of earnings. Prior to the current monetary tightening phase, the fall in interest rates also encouraged this expansion. But markets change, rates are rising, and there is likely to be some reversion to the mean after a hot streak.

4. Watch for style changes

Fund managers who experience a period of underperformance may feel pressure to change their stock selection process. Many a value manager who suffered through a decade of growth stocks winning and a move to tech felt the challenge and criticism of sticking to traditional, boring industrial companies.

It’s an obvious reaction to judge the quality of an investment by its success, or what is known as ‘outcome bias’. A good outcome always looks like a good investment, but an unfavourable outcome may be due to bad luck in a rapidly-changing world, rather than a fund manager’s investment process being fundamentally weak.

5. There should be a uniform and consistent message

Hyperion advises on its website:

"Our funds are designed for investors with a long-term investment outlook, so we recommend looking at 10-year performance where available to appropriately assess growth prospects.

Convention has Hyperion’s portfolios benchmarked against the relevant equities indices. This is something we acknowledge for the sake of reporting but studiously ignore when it comes to making investment decisions."

Exactly right. It was a lapse to highlight the short term when on 29 July 2020, Hyperion issued a media release headed “Hyperion Asset Management top performer over two decades”. Fair enough. Every fund manager on earth would be proud of this achievement and use it to promote their funds.

But then Managing Director and Chief Investment Officer, Mark Arnold said,

“Our performance demonstrates that it is possible to take a long-term view and deliver short-term results with the same fund, growing our investors’ money through lean times and bountiful. We design our portfolios in a way that allows us to consistently profit from market highs as well as to protect capital during periods of market volatility. Our results prove that you do not need to use complex hedging strategies and derivative products to protect your capital during downside movements.” (my bolding)

While the time frames assumed in this comment are relevant, losing 20% to 25% in a quarter does not meet the test of 'protecting capital'. Hyperion went on to quote data compiled by S&P in its SPIVA report on Australia that:

“ ... over the 10- and 15-year periods, 83.9% and 85.30% of Australian equity general funds underperformed the S&P/ASX 200 on an absolute basis respectively. The findings demonstrate that Hyperion is one of a very small group of managers able to consistently outperform over the short and long term.”

Perhaps Hyperion does not consider one year to be short term, but many investors would. Here are the one-year and three-year results sourced from their website as at 31 March 2022.

Hyperion funds net performance versus index

|

Fund

|

1 year

|

3 years

|

|

Global Growth Companies Fund

|

-12.2%

|

+4.8%

|

|

Australian Growth Companies Fund

|

-10.9%

|

+5.9%

|

|

Small Growth Companies Fund

|

-11.9%

|

+2.5%

|

Mark Arnold went further, describing a “strict proprietary investment process which allows the team to separate the winners from the losers.”

Does 'separated' mean the losers are avoided? Roku (down 61%) or PayPal (down 52%) suggest otherwise, and a stock that falls 50% needs to rise 100% to recover the loss.

Hyperion should be well satisfied with the results delivered over two decades but they should temper their claims to reflect a style which will inevitably deliver periods of underperformance that may last at least a year, and probably longer.

Take it away, Coldplay

The final verse of Viva la Vida is a warning that the market can bring every investor down to earth. Even when the investment process is not built "upon pillars of salt and pillars of sand", those who want to be king need to prepare for a period when the monarchy is unfashionable.

"Revolutionaries wait

For my head on a silver plate

Just a puppet on a lonely string

Oh who would ever want to be king?”

Graham Hand is Editor-at-Large for Firstlinks. This article is general information and does not consider the circumstances of any investor. Disclosure: Graham owns a small investment in the listed HYGG.

Extracts from Viva la Vida by Coldplay. Copyright, Universal Music. The concert recorded live in Sao Paulo, Brazil, is extraordinary. The song reached Number One on the Billboard 100 and UK Singles Chart and won Song of the Year at the Grammy Awards in 2009.

Access data and research on over 40,000 securities through Morningstar Investor, as well as a portfolio manager integrated with Australia’s leading portfolio tracking service, Sharesight. Sign up to a free, four week trial below:

Try Morningstar Investor for free