There has always been considerable misinformation surrounding the asset allocation of SMSFs. The main reason is the inadequate categorisation and long-time lags in the ‘official’ Australian Taxation Office (ATO) statistics. Cuffelinks has discussed this directly with the ATO, as reported in previous articles here and here.

The main shortcoming is that the category ‘Overseas shares’ only includes direct share investments, and excludes the billions invested through listed and unlisted trusts and other managed investments. When I confronted the ATO on overseas share asset allocation, their response was:

“It’s fair to say a substantial amount is in international equities, much larger than the number quoted under the ‘Overseas shares’ category.”

According to the official statistic, less than 1% of SMSF assets resides in ‘Overseas shares’. Considering that SMSFs hold one-third of our $2 trillion in superannuation assets, this inaccuracy is a major shortcoming. In fact, people marketing global funds often take advantage of this low number, imploring trustees to correct their ridiculous asset allocation mistake and invest in their global fund. The truth is, trustees are already using hundreds of other available global channels.

A more accurate SMSF asset allocation number

SuperConcepts has released its 2016 Financial Year Analysis based on the actual investments of about 3,300 SMSFs administered by its subsidiary Multiport. Due to its relationship with AMP, this group has more financial adviser input than the average SMSF, giving a greater allocation to managed funds and global equities, but it is instructive of SMSF trends nonetheless.

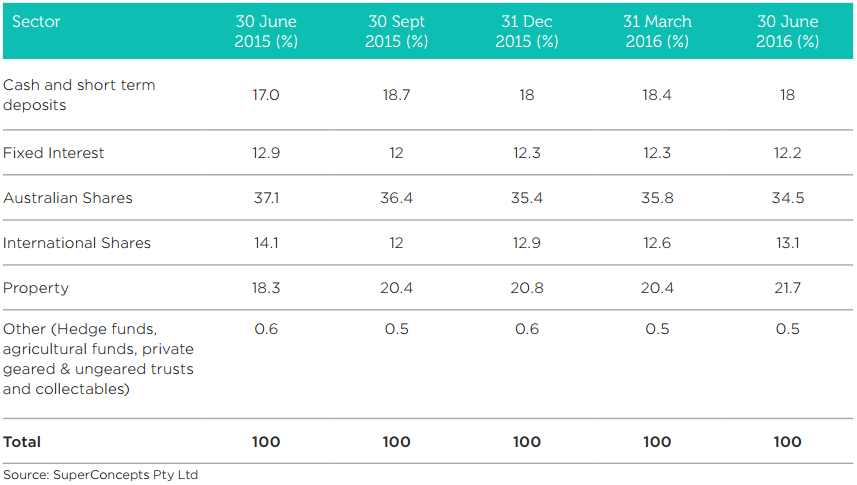

Asset allocation of sample SMSFs as at 30 June 2016

The interesting and sometimes unexpected changes in the last year include:

- A fall in equity investments, with domestic down from 37.1% to 34.5%, and international down from 14.1% to 13.1%, refuting the claims about the TINA (There Is No Alternative to equities) mentality in the sector. SuperConcepts attributes this fall to trustees reducing their exposure during periods of higher volatility, and less appeal of the local large cap stocks. Among the most commonly held investments, two pooled structures, Magellan and Platinum, are favourites with this group for global exposure.

Over the course of 2015/2016, the amount held in the top 10 listed securities fell from 16.5% of all investments to 14%. The Top 10 shares by market cap still represent about 38% of Australian equities held by SMSFs, but the reduction recognises that investors are more concerned about the capital growth of the banks, BHP, Newcrest, and Telstra. Increasingly, SMSFs are looking for opportunities outside of the large caps.

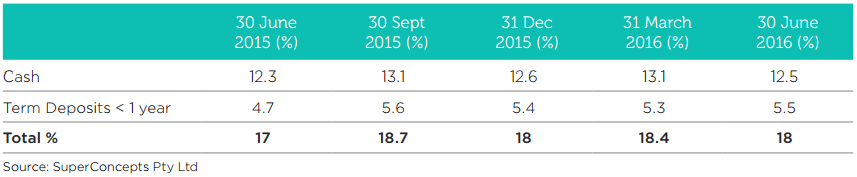

- Cash holdings have increased from 17% to 18% despite low interest rates. Within this segment, term deposits rose more strongly than at-call cash, which took a hit in the last quarter in the face of falling cash rates. It’s surprising to see the large allocation in this segment.

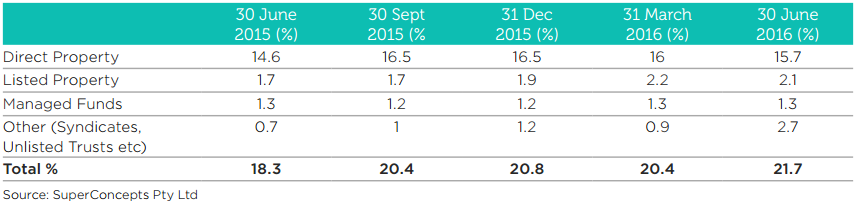

- Property has been the big winner, up from 18.3% to 21.7%, including both listed and unlisted segments. Direct property (often business premises held by the SMSF and rented to one of the trustees, rather than residential property) rose steadily, but the major increase came in the ‘other’ category of syndicates and unlisted trusts. With listed A-REITS trading at a hefty premium to NTA, unlisted trusts have benefitted from the search for yield at better prices.

- Fixed interest allocations fell overall, but hybrids and direct holdings rose. Managed funds in this segment comprise only 4.4% of assets, losing out badly to cash.

(The full report also looks at market movements versus funds flow and makes the same conclusions regarding increases in cash and property and reductions in fixed interest and equities).

Trustees take cash flow decisions in the final quarter

Both inflows and outflows from SMSFs are always at their highest in the June quarter as trustees take action before the end of the financial year. However, with uncertainty surrounding the May 2016 budget, average inflows to SMSFs in the June 2016 quarter of $10,700 were the lowest since 2012. June withdrawals are also heavy, at $17,800, as trustees ensure they meet minimum pension requirements. Withdrawals are always heavier than contributions in any quarter, showing how much the continuing growth of SMSF balances relies on market performance.

Checking from another source

We checked these numbers against the Vanguard/Investment Trends March 2016 SMSF Investor Report, based on a survey of 3,531 SMSF trustees. Its major findings are consistent in direction and include:

- Direct shares (outside of managed funds and ETFs): 38% of total SMSF assets in 2016, down from 41% in 2015

- Cash and other cash products: 25%, up slightly from 24% in 2015

- ETFs: now at 3%, up from 2% in 2015

- Managed funds: 10%, up from 9%

- Direct property (residential & commercial): 11%, up from 10%

- Other investments: 13%, steady

Investment Trends believes the allocation to direct shares (outside of managed funds and ETFs) has declined over the past three years as a result of market performance and poor investor sentiment towards individual shares.

Marketing opportunities

These SMSF investment patterns suggest there are good opportunities for bond funds and other cash alternatives, ex-20 Australian equity funds and other global equity funds. Property is popular but managed funds miss out to direct property, unlisted and syndicates.

Graham Hand is Editor of Cuffelinks. See the full Investment Patterns Survey here. SuperConcepts is a Cuffelinks sponsor.