The primary focus of the Financial Services Royal Commission to date has been consumer lending, financial advice and small-medium enterprises, but the investment management industry may also be lacking in public trust.

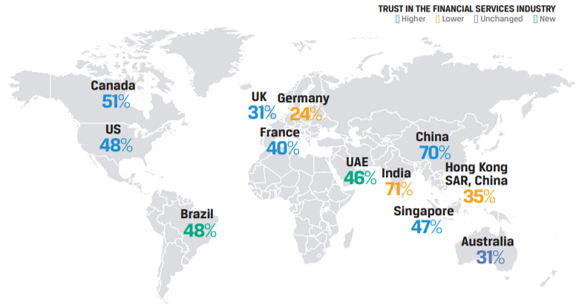

A survey in November 2017 by the CFA Institute called “The Next Generation of Trust – A Global Survey on the State of Investor Trust” highlighted some alarming signs that resonate here in Australia. The survey highlighted that trust in financial institutions is very low and the reputation of the finance industry compared to other industries remains poor. It also showed a widening gap between investor expectations and outcomes delivered. The map below shows the level of trust in the financial services globally. It is alarming to see that Australia has the equal second lowest level of trust after Germany at 31%. I suspect this outcome for Australia may be even lower today.

Trust in the Financial Services Industry: Reputation versus Realities

The survey asked retail respondents to rate seven actions that investment firms could take to build trust, ranked in terms of importance and personal level of satisfaction. The areas with the biggest difference between expectations and outcomes included disclosure regarding fees and conflicts of interest.

The CFA survey relates to the broader, and global, investment community. However, in the recent increase in Listed Investment Companies (LICs) in Australia, a key area of focus has been appropriate and consistent disclosure on the reporting of performance and fees.

Internally managed vs externally managed LICs

The traditional, internally managed LICs offer a low cost, transparent and stable but growing dividend for shareholders. In addition, management works for the company so there are no fees paid to an external manager nor any conflict of interest between the shareholder and manager. These LICs generally have a lower turnover and are considered an investor on ‘Capital Account’ for tax purposes as opposed to ‘Revenue Account’ firms which are considered traders.

Externally managed LICs offer a number of different strategies backed by some strong recent performance. However, the industry sometimes falls short in the reporting of consistent and relevant information for shareholders. Often what is disclosed are performance figures highlighting only a pre-tax portfolio performance, which can differ from the end-result to investors due to management fees, performance fees, dilution and taxes. Another often poorly disclosed factor is whether external fees are calculated pre-tax or post-tax. This makes accurate comparison between different LIC strategies difficult for retail investors.

This is an area where the ASX should assume leadership and create standard disclosure requirements for the LIC sector to ensure investors are fully and fairly informed.

Internalising IPO costs on new LICs

The recent trend for new LICs to internalise IPO listing costs (paid by the manager) is positive, as shareholders in the IPO have an NTA on listing equal to the issue price. However, the external managers are not doing investors a huge favour. Shareholders need to read the PDS/prospectus carefully, as the manager could be seeking to claw back these costs from shareholders over time through management fees and performance fees.

In addition, there are often onerous costs to break an investment management agreement, ensuring the manager will recover the listing costs with little risk. The primary attractiveness of LICs for external investment managers is the ‘captive money’ such an arrangement brings. While this guarantees the funds for future fee streams, it also removes the implications of money entering and redeeming from the fund, often at the worst times. Certainty of funding should allow for better investment decisions over the longer term. The importance of long-term captive money is intensified by fee pressure in the institutional funds management space and the internalisation trend being pursued by industry super funds.

What can Australia learn from the UK?

LICs have exploded in number and market cap over the last few years in Australia. However, they do go through cycles in terms of investor appetite and tend to trade on yield as much as NTA. The majority of recent LICs conduct financial reporting on ‘Revenue Account’ and many pay dividends from capital, usually realised gains. These gains may come under pressure in a market downturn, so investors need to be aware of the risk regarding the sustainability of dividends. Investors need to analyse where their dividend is coming from, and how much retained earnings the company has to support future dividends.

An interesting trend in UK investment companies has been the use of ‘continuation votes’, where a company’s articles of association provide for shareholders to vote on whether the company should continue to exist under certain circumstances. They give shareholders the opportunity to vote on a company being wound up. Some continuation votes are conditional on measurement metrics – say, when the discount to asset backing is trading wider than a pre-determined level for a period. Other continuation vote opportunities are offered on a periodic basis. Perhaps this is something that in time LICs in Australia could consider.

Survey recommendations

The CFA Institute survey also offered recommendations for the industry to increase investor trust through a ‘trust equation’ which is a combination of credibility and professionalism. Credibility addresses factors such as track record, brand, well credentialed people and the use of a code of conduct. Professionalism focuses on areas such as transparency and clarity regarding fees, competency, and values. Like any highly regarded service industry, trust and quality service should be the bedrock of a firm’s foundation.

Financial institutions are facing a challenging time with ethics and culture, as greed, dishonesty, and fraud appear to be occurring too often. The investment management industry is competitive. It is critical to provide appropriate products and transparent disclosure, and to ensure investors interests are put first.

About the survey

The Next Generation of Trust data collection was conducted by research firm Greenwich Associates and consisted of a 15-minute online survey conducted in November and December 2017. The survey sampled 3,127 retail investors (25+ years old) with investable assets of at least US$100,000 in the United States, Canada, Brazil, United Kingdom, France, Germany, the United Arab Emirates, Australia, India, Singapore, China, and Hong Kong. It also sampled 829 institutional investors with assets of US$50 million or more in these markets. The survey and related data is available at nextgentrust.cfainstitute.org.

Andy Forster is a Senior Investment Officer at Argo Investments Limited. This article has been prepared for educational purposes and is not a substitute for tailored financial advice.

Charts are Copyright 2018, CFA Institute. Reproduced and republished from “The Next Generation of Trust: A Global Survey on the State of Investor Trust” with permission from CFA Institute. All rights reserved.