“We always overestimate the change that will occur in the next two years and underestimate the change that will occur in the next 10. Don’t let yourself be lulled into inaction.” Bill Gates

Part 1 was a focus on short term disruption and the potential for a new entrant to gain a significant slice of the wealth market, and concluded:

I don’t see how any company can make wealth management sufficiently exciting for enough people to grow a market share of 5 to 10% in the next few years. To use Google’s test, what problem will the disruptor solve in such a novel way that hundreds of billions will divert from incumbents? I hope I’m wrong because it would be fun to watch.

Part 2 takes a longer time frame over the next decade to 2025, and predicts the likely winners and losers, especially for superannuation.

The power of incumbents

The three main (but not only) parts of the wealth management value chain are financial planning, administration services and asset management.

While each is a distinct service, the market is dominated by businesses that perform all three roles, although clients may not realise their adviser is aligned with one of the big players. The four major banks plus AMP 'control' about 70% of financial planner business. Many clients of the Commonwealth Bank who meet a planner in their local bank branch will be set up on a Colonial First State administration platform invested in a fund managed by a group subsidiary. Such ‘vertical integration’ is the subject of much angst from consumers, regulators and governments but it received relatively little attention from the recent Financial System Inquiry. A recommendation to review Stronger Super in 2020 is at least two Federal elections away.

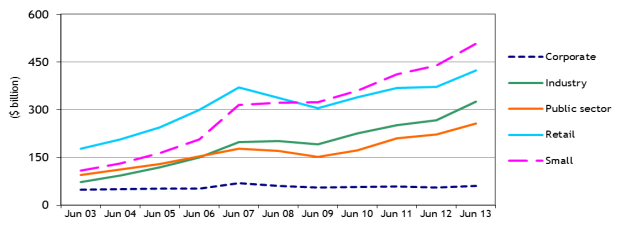

However, despite their vast distribution networks, these retail fund businesses are far from winning the superannuation race they dominated until around the GFC. Between 2007 and 2008, retail super funds, heavily invested in equities, fell significantly, while SMSFs (labelled ‘Small’ in Chart 1 below) attracted new members and held a more conservative asset mix with 30% in cash and term deposits. SMSFs overtook retail funds in 2009 and now hold about one-third of the $2 trillion in super. And whereas a decade ago, the industry funds were less than half retail funds, they are now around three quarters and catching up fast.

Chart 1: $ billion held by various superannuation industry sectors

Source: APRA Annual Superannuation Bulletin, revised February 2014

Of course, other providers specialise in only one part of the wealth value chain. There are thousands of non-aligned financial advisers who argue they are more independent and better able to act in a client's best interests. Similarly, there are dozens of sophisticated administration platforms, especially (but not only) for assisting in the management of SMSFs, which allow investors to hold almost anything. And there are hundreds of asset managers holding billions of dollars (super and non-super), all claiming special talents which shout ‘choose me’.

Industry funds in the context of market disruption

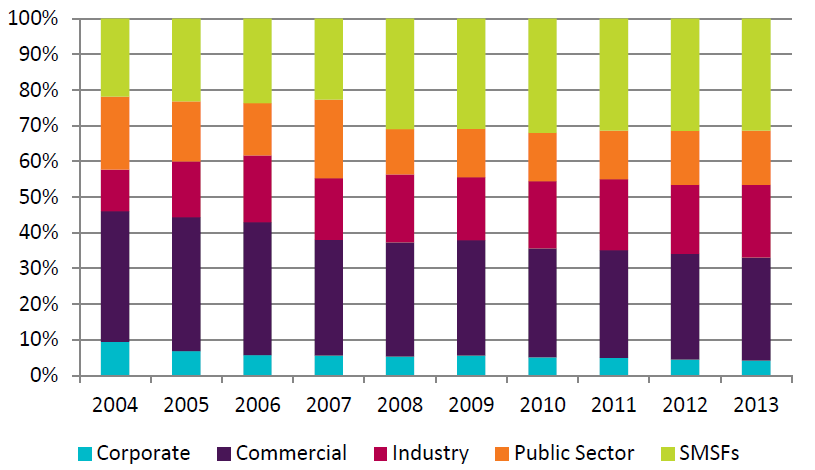

Two of the major competitive forces, SMSFs and industry funds, are almost unique in the world in their structure, making the likely future outcome for wealth management in Australia different from other countries. Chart 2 shows market shares of superannuation assets and these two segments are the big winners in the last decade. According to Rice Warner, while corporate funds, retail (‘Commercial’ in the chart) funds and public sector funds have all fallen significantly, industry funds have doubled their share of the large superannuation fund market (excluding SMSFs) from 15% to 30% since 2004.

Chart 2: Market share of the superannuation industry, 2004-2013.

Source: Rice Warner submission to the Financial System Inquiry, page 14.

What are the strengths and competitive advantages of industry funds that will enable them to thrive in the face of new sources of competition?

- Client acquisition. Most people who start their first job on the checkout at a supermarket at the age of 15 are given a ‘starter pack’, and it includes an application form for the Retail Employees Superannuation Trust (REST). It’s not only low income earners, as Unisuper’s position in universities shows. The largest, AustralianSuper, manages almost $90 billion. While industry funds have experienced some leakage to SMSFs, the majority of clients stay for life.

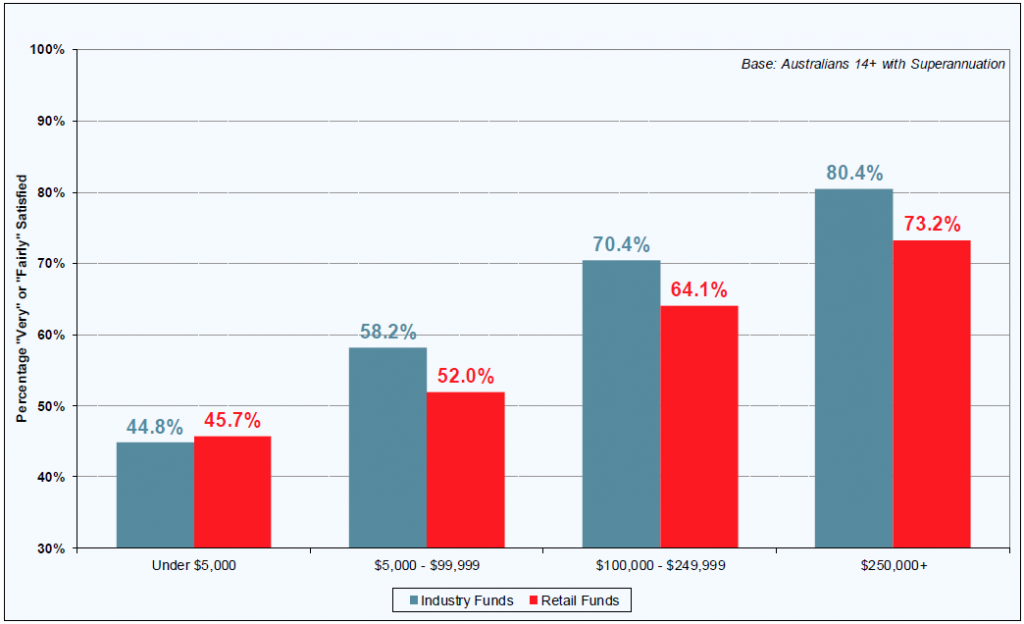

- Higher satisfaction ratings. Without entering the debate about whether it is perception or reality, industry funds are considered to deliver performance at least as good as retail funds at a lower price. Industry funds have led retail funds in overall satisfaction ratings for over a decade. As shown in Chart 3, what is most surprising is the satisfaction gap is much greater with larger balances, where investors are likely to be better informed and engaged. Satisfaction is similar for under $5,000 but wide for over $250,000, which accounts for only 10% of customers but a whopping 43% of balances. It’s not an encouraging sign for retail funds gaining large clients from industry funds.

Chart 3: Satisfaction with financial performance of superannuation by balance held

Source: Roy Morgan Research, six months to December 2014, sample n=15,932.

- Not for profit structure. Industry funds have only one type of stakeholder, their members. This clarifies decision-making and should lead to singularity of purpose, of improving member returns and services at the least cost. Retail funds must satisfy shareholders demanding an economic return on capital, requiring a profit margin built into fees.

This final point is the most important for long term expectations. As industry funds grow, the largest bring more of their funds management in-house. The economics of paying competitive salaries for top fund managers are compelling for a fund with say $50 billion in total and $20 billion in equities, paying 0.40% to an external manager. That’s $80 million in fees, which covers a lot of salaries and bonuses. Even if asset management is not brought in-house, an ever-expanding range of sector index funds plus smart beta funds are available at a fraction of the fees of active managers. With the guaranteed SG inflow from a largely disengaged client base choosing default funds, they have the potential to lower fees significantly over time.

Within 10 years, as funds grow with a largely fixed cost base spread over more assets, industry funds will commonly deliver their main default balanced fund options for 50bp or less all in. That will cover asset management, administration and even some financial advice. All the large funds will further develop their advice capability at subsidised costs with salary-based staff, removing many of the arguments about conflicts that come from commissions. While advice will not be free, it will be attractively priced, again with no profit margin driving the fees.

The main risk facing industry funds is that the government may remove the privileged position as the nominated funds under employee awards. This may be matched by increasing the number of independent directors, a change which may assist public perception. Either way, industry funds will remain a major force in the market, probably stronger than their current market share of super. Retail funds have their MySuper products around 1%, but they will not deliver better fund performance to make up for the higher fees. Even where industry funds outsource their asset management, they use the same managers as retail funds and can negotiate rates which are at least as competitive.

The rise and rise of SMSFs

The improvement in technology and developments in ‘fintech’ and ‘roboadvice’ make it easier than ever to manage an SMSF. An administrator can sign up a new SMSF, including opening a bank account, broker links, access to a term deposit aggregator, full trustee identification and comprehensive reporting, all online in less than 30 minutes. Without entering the debate about the minimum amount required for an SMSF, it is certainly cost competitive at amounts above say $500,000 (and many argue much less), where even a low 0.5% is $2,500. This will cover tax returns, audit and reporting for a simple fund, which can then choose inexpensive investment options such as ETFs or direct ASX investments to keep management costs down.

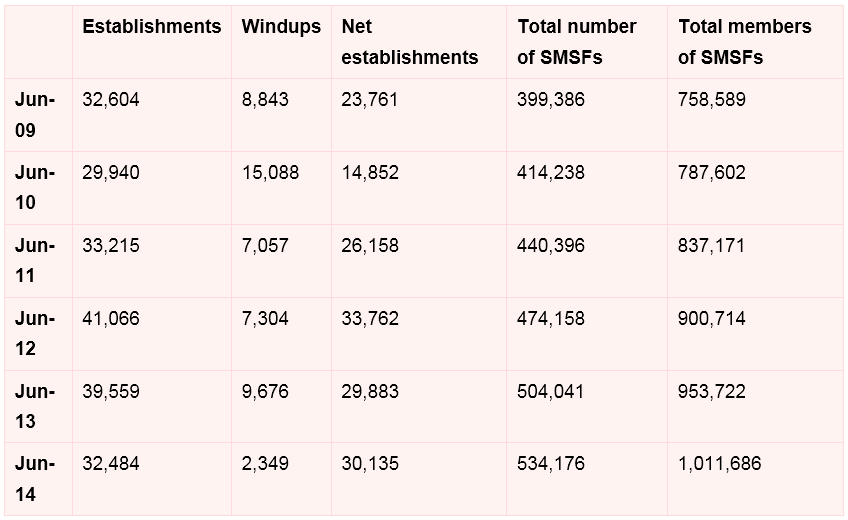

Retail funds have obviously done well in the rising stockmarket of the last few years, and they are far from struggling. Staff have still received their handsome bonuses. But there’s little sign of a drop off in the establishment of SMSFs, now well over half a million.

Chart 4: Membership and number of SMSFs

Source: Australian Taxation Office, SMSF Statistical Report, June 2014

With around 30,000 new SMSFs established each year, that’s about 100 a day, with an average of two trustees. Over one million Australians have signed a 90 page Trust Deed taking legal responsibility for their own superannuation.

A recent report entitled ‘The 2015 Automated Investment Advisers Global Market Review’ by FinDigital and Ignition Wealth reviewed 45 roboadvice offers, and found they were often targeting self-directed investors including SMSFs. Technology is not only for younger generations as the roboadvice offers appeal to older investors due to the better customer experience and lower fees. These developments are likely to encourage more SMSFs, as the simple advice models suggest planning decisions relating to risk assessment and asset allocation can be done without an adviser.

Where does that leave the retail funds?

Retail funds will continue to grow in absolute terms, even while they lose market share to industry funds and SMSFs. Their distribution networks and provision of most of the ‘face to face’ financial advice will ensure they remain strong businesses. They have billions invested in technology, and they have the marketing resources to attract corporate super, where 80% of people do not actively select their own fund but default to that selected by the employer.

On the platform side, it's an industry truism that managed funds are sold and not bought. Financial planners have their favourite platforms or funds around which they build their administration and model portfolios, and it’s not easy to change. The retail providers will continue to service their networks well.

But it is increasingly easy to create the same asset allocation possibilities using the ASX and a collection of ETFs, LICs, listed bonds, alternatives and shares. There are dozens of simple administration platforms of varying sophistication which might cost as little as a few hundred dollars a year. A copy of the contract note for the trade on the ASX is automatically sent to the administrator for a portfolio to be updated real time. They may not have the tax sophistication of a full retail platform but the information automatically generated at the end of the year makes the financial return straightforward for a competent accountant. The ASX's mFund service delivers managed funds previously available only via a platform or long form PDS.

What about fintech, roboadvice and other new providers?

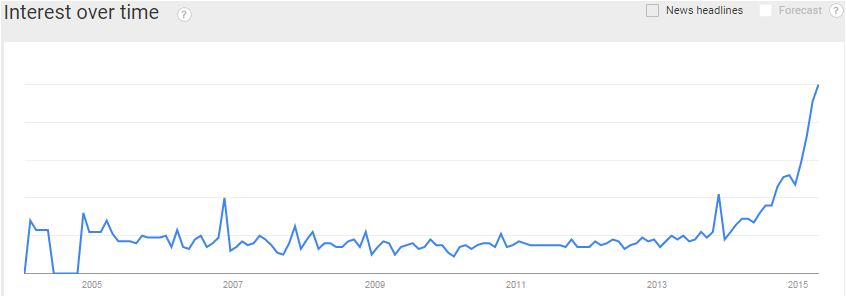

Fintech and roboadvice are starting to make an impact in wealth management services. The basic approach requires a client to answer a series of questions to assess their risk capacity, income, assets and long term goals, and an algorithm generates a suggested portfolio. There may be online or video conversations with an adviser. It is clearly no substitute for a bespoke, personal consultation with a skilled financial planner, but a minority of people have a planner. And while most people nearing retirement are no doubt missing out on good planning ideas, such as making the most of superannuation, estate planning, insurance and portfolio construction (to name a few of the things a good financial planner will cover), for many the roboadvice is a major step forward in the diversity and sophistication of their retirement planning. Chart 5 shows how much the word ‘fintech’ has entered our search conversations (acknowledging ‘fintech’ has a much broader definition than only wealth management).

Chart 5: Google Trends based on search term ‘fintech’ with April 2015 the ‘base’ of 100

While many criticise the simplicity of roboadvice, it offers better opportunities than keeping money in the familiar places of cash, term deposits, bank shares and residential property (not that such a portfolio has done poorly in recent years, but it does lack the diversity that international equities and other asset classes bring).

Such online advice and implementation is usually cheap, based on ETFs with an all-in cost of say 0.25% per annum. Although Vanguard moved into online advice based on index funds, it recently added active funds for clients who want to complement indices with active stock and bond pickers. Active management remains a massive market and roboadvisers will not necessarily ignore it.

We are only at the beginning of an exciting new development: the market leader in the United States, Wealthfront, has only about USD2 billion under management, a tiny (read insignificant) share of the market despite its high profile and slick technology.

In Australia, some early movers are Decimal, Stockspot, SelfWealth, AdviceConnect and BigFuture. In the United States, more advanced are Betterment, Wealthfront and PersonalCapital, plus more established names like Charles Schwab and Vanguard.

As we discussed in Part 1, many of the new entrants in roboadvice will do well, as they have relatively low costs and capital needs, and a couple of billion under management can be an excellent business. But with $2 trillion in super, a 1% market share is $20 billion. While 1% is hardly market disruption on the scale of Amazon’s effect on Borders, are there any trusted names which have the capacity to raise this much over say the next decade?

If the technology (ETFs, roboadvice, cheap administration) had been available 10 years ago, then a name like Virgin may have made a bigger splash. Its brand was moving into everything, but its impact has been largely confined to credit cards rather than superannuation. Virgin is one of the most recognised brands in the market, yet it struggles as a wealth management name.

The best technology companies and retail brands in the world, such as Google, Apple, Facebook, Twitter, Microsoft, Ebay and Amazon, clearly have the deep pockets and distribution to design solutions that can gain a big following. It’s reasonable to expect them to see the opportunities in wealth and consider it an extension of their existing businesses.

And of course there are points of intersection where incumbents use new technology to improve their own offers. Regardless of developments, face to face advisers will always have a role in coaching and guiding their clients, especially where needs are complex such as estate planning, tax, aged care and retirement. These advisers can use roboadviser tools to help with risk assessment, portfolio selection and investment reporting. This will be complementary to moving the financial advice industry into the more professional status so keenly sought by the industry.

Conclusion on the future of wealth management

Technology can change industries almost overnight, and in hundreds of ‘tech hubs’ around the world, some of the smartest brains of any generation are working day and night to develop an online investing and advice solution that will change the world. The former executives from Kodak, Blockbuster and Borders know that even experts in a business do not see the freight train coming until it runs over them. The new generations of investors are far less loyal to existing relationships and open to innovative forms of technology.

Recognising the warnings by Bill Gates not to underestimate long term change, my expectations are (defined for simplicity in terms of superannuation): SMSFs to continue to increase market share but with some natural cap due to most people remaining disengaged with investing; industry funds to gradually lower fees and expand more into advice and to take over retail funds as the second largest segment; retail funds to remain strong based on broad distribution but to lose market share due to higher fees without better performance; and new entrants using elegant online solutions to have some great successes and great failures but no single new party will have greater than 10% of the market by 2025.

(A six-minute video to go with this article is linked here).

Graham Hand has worked in funds management, investment banking and retail banking since 1979 and is Managing Editor of Cuffelinks.